Interest Rates vs Equities amp Overblown Reactions to FOMC Rhetoric

It’s not the end of the world when the Federal Reserve pauses from easing, or even starting to raise rates. Often times, the opposite happens. […]

It’s not the end of the world when the Federal Reserve pauses from easing, or even starting to raise rates. Often times, the opposite happens. […]

It’s not the end of the world when the Federal Reserve pauses from easing, or even starting to raise rates. Often times, the opposite happens. The release of the minutes from the December FOMC meeting earlier this month indicated “several” FOMC members favoured stopping or slowing asset purchases well before end of 2013 caused it share of jitters in bond and equities.

Some observers viewed this as an indication of unwinding QE, which would be a negative for equities, gold and a boost for the greenback as well as yields.

We disagree with such conclusions for many reasons, one of which being that slowing the pace of purchases is largely different from tightening policy. In addition, the Fed could always indicate (via minutes rather than Bernanke himself) a leaning away from the continuous $85 bn in monthly purchases to say $70 bn or $60 bn, before reverting to higher purchases or loosening policy in another shape or form—such as extending the guidance for zero rates.

Another factor is the data itself. If the declining trend of unemployment sustains a brief pause, or a slight blip, then markets could transition into “cheering bad news” on the basis of maintaining ultra-loose monetary policy as long as inflation is largely contained.

Last but not least, the Fed’s shift towards an implicit targeting of 6.5% unemployment rate leaves out the case for any tightening—especially as the rate currently stands at 7.8%. In fact, a decline of such magnitude in unemployment has historically taken at least two years.

And so even if the dovishly-slanted FOMC of 2013 takes the improbable decision of voting for slower asset purchases, such a shift would be considered as mere “cooling” in the pace of easing, rather than tightening. There is a vast gulf of market movements and expectations between easing, neutral and tightening.

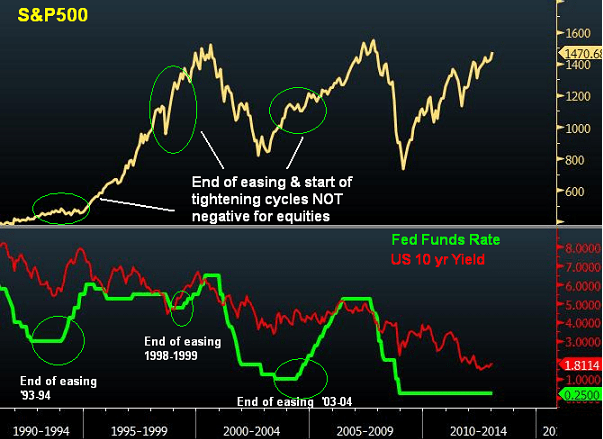

Finally, once the Fed reaches a neutral stance (sign of economic strengthening), equities have rallied during such a phase.

S&P500 during periods of neutral policy following rate cuts

Sep ‘92 to Jan ‘94: S&P500 +15%

Nov ‘98 to May ’99: S&P500 +16%

June ‘03 to May ‘04: S&P500 +18%