HSBC shares still weighed by uncertainty

HSBC has wasted no time since announcing a strategic refocus just over a month ago. The world’s second-largest bank in terms of assets said it […]

HSBC has wasted no time since announcing a strategic refocus just over a month ago. The world’s second-largest bank in terms of assets said it […]

HSBC has wasted no time since announcing a strategic refocus just over a month ago.

The world’s second-largest bank in terms of assets said it wanted to shed billions of dollars of those assets, and it’s started by inking a $5.2bn deal in Brazil.

However, HSBC’s far-reaching targets and a likely decision to leave Britain have placed a weight on its shares that could last for months.

Banco Bradesco, Brazil’s largest lender, agreed to buy HSBC Bank Brasil, Banco Múltiplo and a number of other units.

The price HSBC will get for the assets is complicated by the adjustments required to reflect net asset value, but it’s expected to be the equivalent of 1.8 times their book value, currently standing at $5.2bn.

That’s far better than the below-tangible book-value offers HSBC reportedly received earlier.

The disposal of the Brazilian business will help HSBC reduce risk-weighted assets (RWA) by about $37bn.

HSBC’s CEO, Tim Gulliver had set a target of $290bn in planned asset reductions to take advantage of potential growth opportunities elsewhere.

The sale of assets in Brazil and also the likely completion of deals to sell HSBC’s loss-making Turkish unit can be expected to rake in about $110bn.

Even without confirmation that it has trimmed the fat in Turkey, HSBC has still managed 10.6% annualised return on equity (ROE) in its first half, well within its target calling for ROE above 10%.

A dividend yield above 5.5% also looks assured, judging by management comments.

Additionally, the bank noted that profits in the first six months its financial year were driven by the upswing of volatile markets in China, when markets there were soaring earlier in the year.

The bank’s Hong Kong broking business was a beneficiary of inflows unleashed by the Stock Connect trading link established with Shanghai, fortuitously timed when markets were rocketing.

However this tailwind from the Far East may turn into a headwind in the second half of 2015.

[CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0) or GFDL (http://www.gnu.org/copyleft/fdl.html)], via Wikimedia Commons")

HSBC Building, 8 Canada Square, Canary Wharf, London, UK, by Danesman1

Initially news of HSBC’s significant progress in H1, particularly the asset disposal news, propelled its stock more than 1% higher on Monday.

However this gain was pared back within an hour of trading.

Whilst HSBC’s first-half pre-tax profit beat expectations with a 10.5% rise to $13.63bn, compared with $12.34bn expected, first-quarter net profit was actually 4% lower to $4.4bn.

And given that stock markets in China have since gone on to burn more than third of the 150% gains built over a year or so, some of the shine is likely to come off HSBC’s earnings performance in the second half.

RWA reduction so far not withstanding, HSBC’s target to cut risk-weighted assets in its global banking and markets division to less than a third of group total will also take more than one fiscal half to achieve. As will HSBC’s goal to reduce costs by up to $5bn by 2017.

This, combined with the uncertain situation in China, and, the risk that HSBC’s global HQ may depart UK shores for Hong Kong by the end of the year, may be why its UK shares continue to trade below book value, despite the rapid progress made on its recovery plan.

London Stock Exchange rules state that when a company’s headquarters are in a country in which it is listed, it will be delisted from all UK indices.

If that happened to HSBC, as the situation currently stands, index-tracking funds would have no option but to liquidate all their holdings.

At last count, just 629 investing institutions held 43.83% of the London-listed stock.

Whilst a potential one-off agreement between the LSE and HSBC could ameliorate the possible impact of the exchange’s requirements, uncertainty will continue to damp the stock for months.

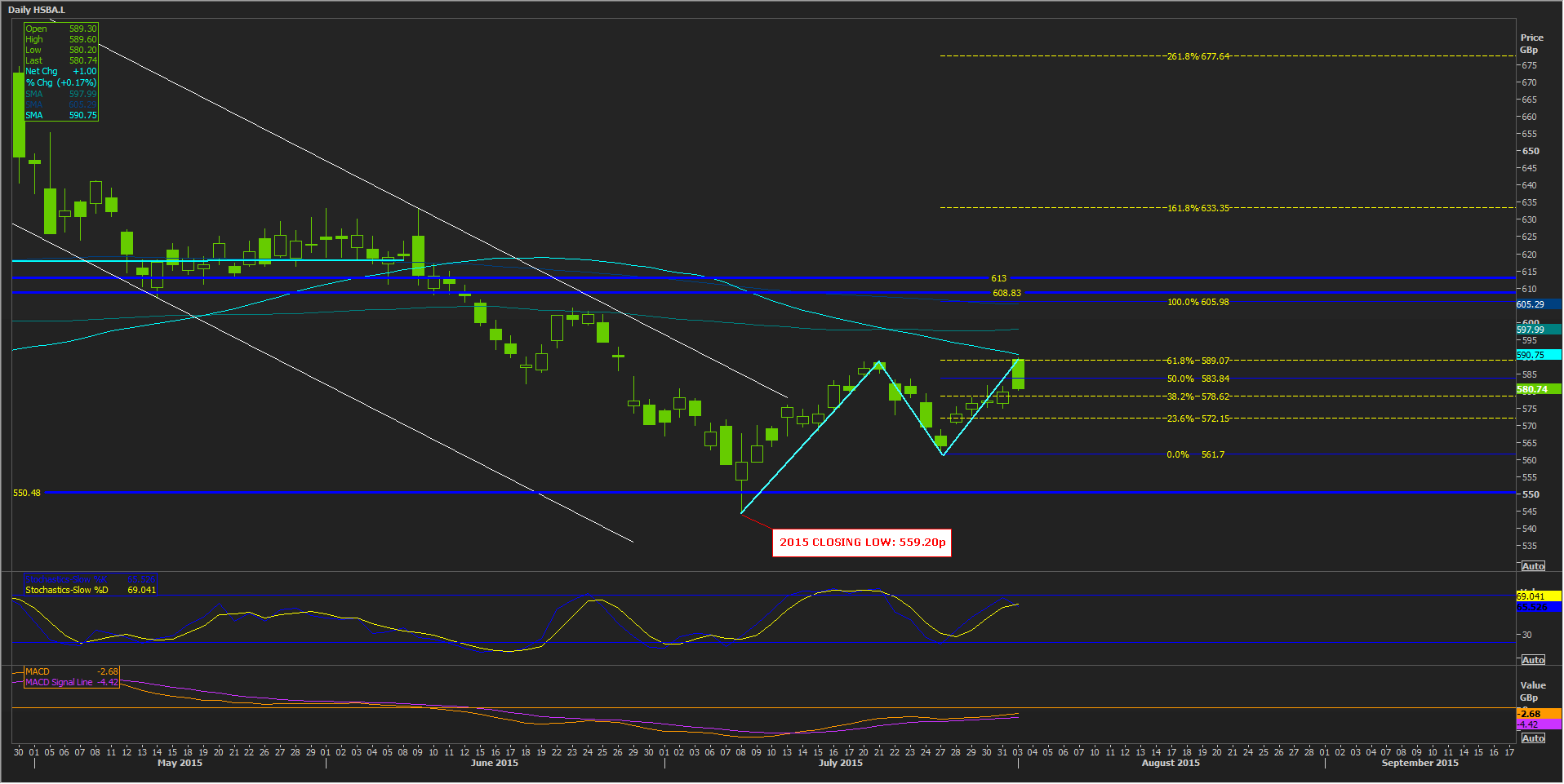

Last month, the shares escaped the falling channel they entered in the spring. (At the time, its senior management had faced embarrassing public scrutiny and the bank also felt widespread opprobrium for its alleged client advice on taxation.)

Since hitting a 2015 low in early in July, the stock has risen more than 8%.

It is now a matter of 8p away from its 50-day moving average (having fallen below it in June).

The recovery has now extended some 61.8% and that important Fibonacci marker has given the shares further reason to pause.

A drift back to the base of the recent up leg seems likely, implying 561p in the medium term.

Please click image to enlarge