HSBC share slide little to do with Brexit warning

HSBC is ‘the biggest bank in Europe’, but perhaps the least exposed to recent peculiarly European capital concerns. Yet it has still seen double-digit percentages […]

HSBC is ‘the biggest bank in Europe’, but perhaps the least exposed to recent peculiarly European capital concerns. Yet it has still seen double-digit percentages […]

HSBC is ‘the biggest bank in Europe’, but perhaps the least exposed to recent peculiarly European capital concerns.

Yet it has still seen double-digit percentages lopped off its shares this year.

Final earnings out on Monday demonstrate why.

The Asia-focused, corporate-leaning lender, which has been forced to fend off regulatory troubles closer to the region it has (re)chosen to call home, booked another stagnant set of results for the year ending 31st December 2015.

The main weight on the bottom line was an unexpected $858m Q4 loss due to impairment charges on derivatives, legal costs and the bank’s wholesale retreat from Brazil.

Revamp costs on the way to cost savings (the bank hopes to trim up to $5bn) were also in the frame.

The main theme was, in short, rather too reminiscent of the same one which has been playing on global banks for the last decade: high regulation/low growth, raising concerns among investors about just what circumstances would be enough to facilitate reasonable banking returns.

Added to HSBC’s barely filtered exposure to China and other EM regions, there appears to be ample scope for continued uncertainty.

Dividends were among the better points—the total ticked 1 cent higher to $0.51.

But there was concern here too.

Investors noted that at 8%, the yield was creeping higher vs. market average and might be flashing a classic signal of a forthcoming cut.

The bank also guided its investors towards a couple of other issues they might like to worry about.

It said it was ensnared in one of the near-innumerable regulatory investigations that are most certainly non-legacy.

This one was an SEC probe into recruitment practices ‘in Asia’ (though so far that usually means China).

It’s the “Princelings” phenomena, in which it’s alleged the offspring of powerful families are hired for mutual benefit.

JPMorgan was among the first to be slammed for this in 2013.

It remains under investigation and faces multi-million dollar penalties.

HSBC offered no timeline for resolution in its case, but warned the impact “could be significant”.

It also joined the Brexit Bandwagon.

“A disorderly (EU) exit could force changes to HSBC’s operating model, affect our ability to access the European Central Bank and high-value euro payments, and affect our transaction volumes due to possible disruption to global trade flows”.

Actual or feared Brexit should probably be the least of its investors’ worries in our view.

It is unlikely that quantification of the impact of the UK’s departure from the EU has been completed by most large businesses, even if guesstimates end up in the right ballpark.

No, HSBC shares were down 19% for the year to date at online time due to the impact of its global regions and global clients, which in turn tend to have exposure to oil and commodities and emerging markets.

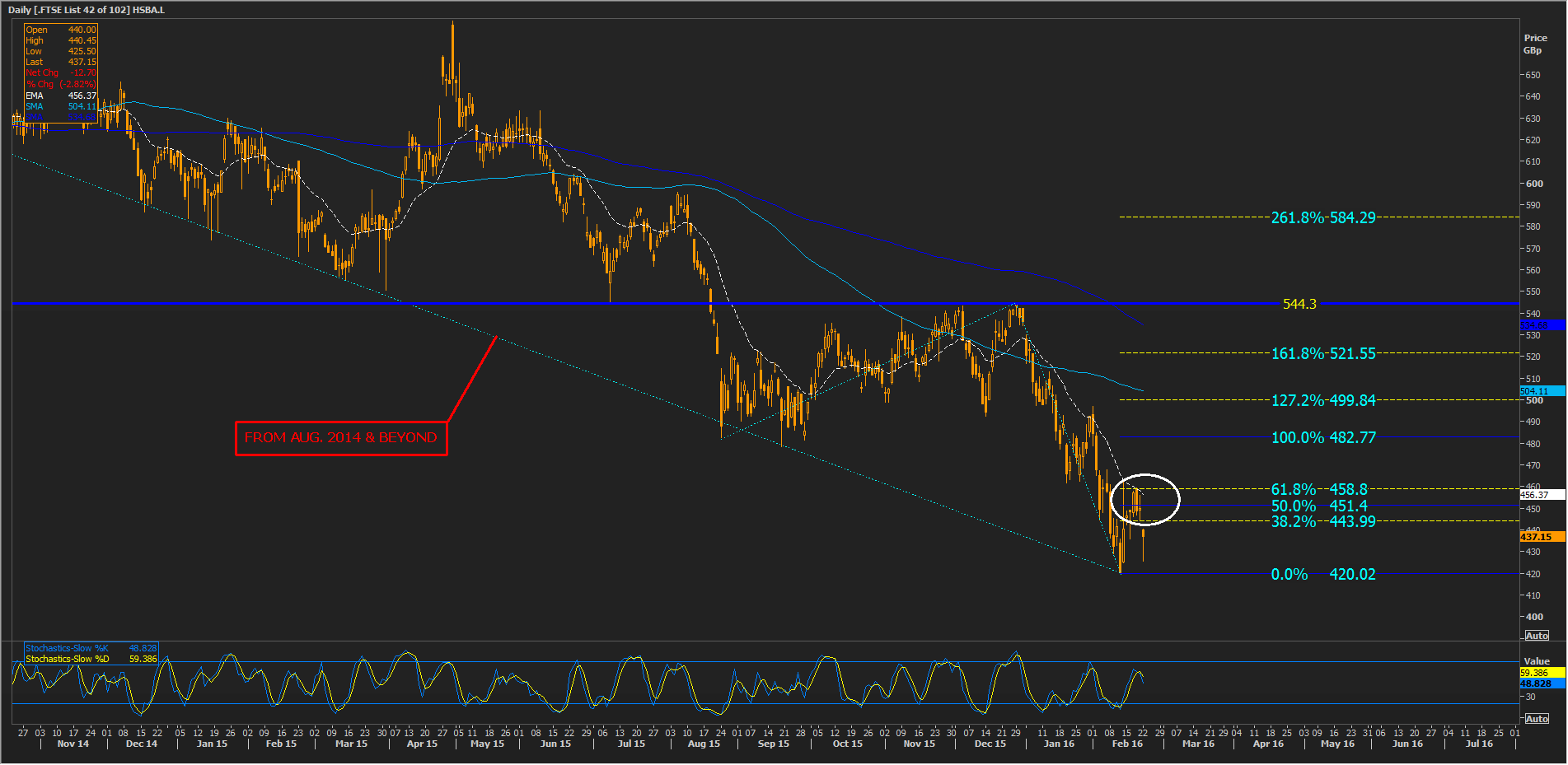

From a technical basis, HSBC stock has displayed similar patterns to assets in the above categories for at least 18 months.

Chiefly it has clung to a long-term downtrend.

HSBA’s most recent failure to break the pattern got as far as 544p.

Fibonacci intervals in extension from the commencement of that leg show the share’s most recent reversal was at a 61.8% marker equating to 458.8p.

Weak momentum (sub-chart) tends to confirm the outlook for continued weakness, though investor unease with current prices which trade below intrinsic value (close to ‘credit-crunch’ lows) suggests a game of squash for the near term.

The ceiling mentioned above won’t break very easily.

Please click image to enlarge