HSBC dividend cheer may be followed by chill

HSBC paints a dour picture for its U.K.-based business which it expects to face Brexit flak, but investors are focusing on dividend hopes.

HSBC paints a dour picture for its U.K.-based business which it expects to face Brexit flak, but investors are focusing on dividend hopes.

Unlike the British press, it seems, investors are clear that the bulk of HSBC’s future revenues, profits and growth, on the near horizon hinge more on businesses overseas.

Ironically though, it was a change in how Britain’s Prudential Regulation Authority treats HSBC’s investment in China’s Bank of Communications that enabled the group to report another rise in core capital to 13.9% from 12.1% at the end of June.

The perception that the group’s regulatory ‘cushion’ is strengthening —albeit in the third-quarter it was only a paper accounting treatment—plays directly to HSBC’s ability to maintain dividend pay-outs at the current level, hence shares rose as much as 5% on Monday.

The group’s abandonment of a 10% return on equity (ROE) target earlier this year tells investors all they need to know about when the bank expects to offer shareholder income around that level.

True, core profit would have been more optically pleasing in Q3 without such impairments as a £1.7bn loss from the sale of HSBC’s Brazilian business, falling trade finance revenues, and negative currency effects.

Its Risk Weighted Asset sell-off is also as good as done, with assets equivalent to just a fifth of the $250bn-$300bn total remaining to be sold by the end of 2017.

But HSBC’s cost of equity is widely thought to have churned around 9% for most of 2016.

That’s great given the economic climate for global banks, but still way above returns which, likewise, have floundered around 2%, and are expected to continue to do so for years.

The U.K. does offer opportunities given the group’s roots here and 13% current account base—less than half of the group’s retail deposit base has a mortgage with the lender.

Strong returns in Asia also promise a smoother post-RWA ride for HSBC than for rivals.

For the immediate term though, investors may yet face the banking sector’s continuing ‘winter chill’ before the thaw, because the group has not categorically ruled out dipping into reserves, or even borrowings to fund the dividend.

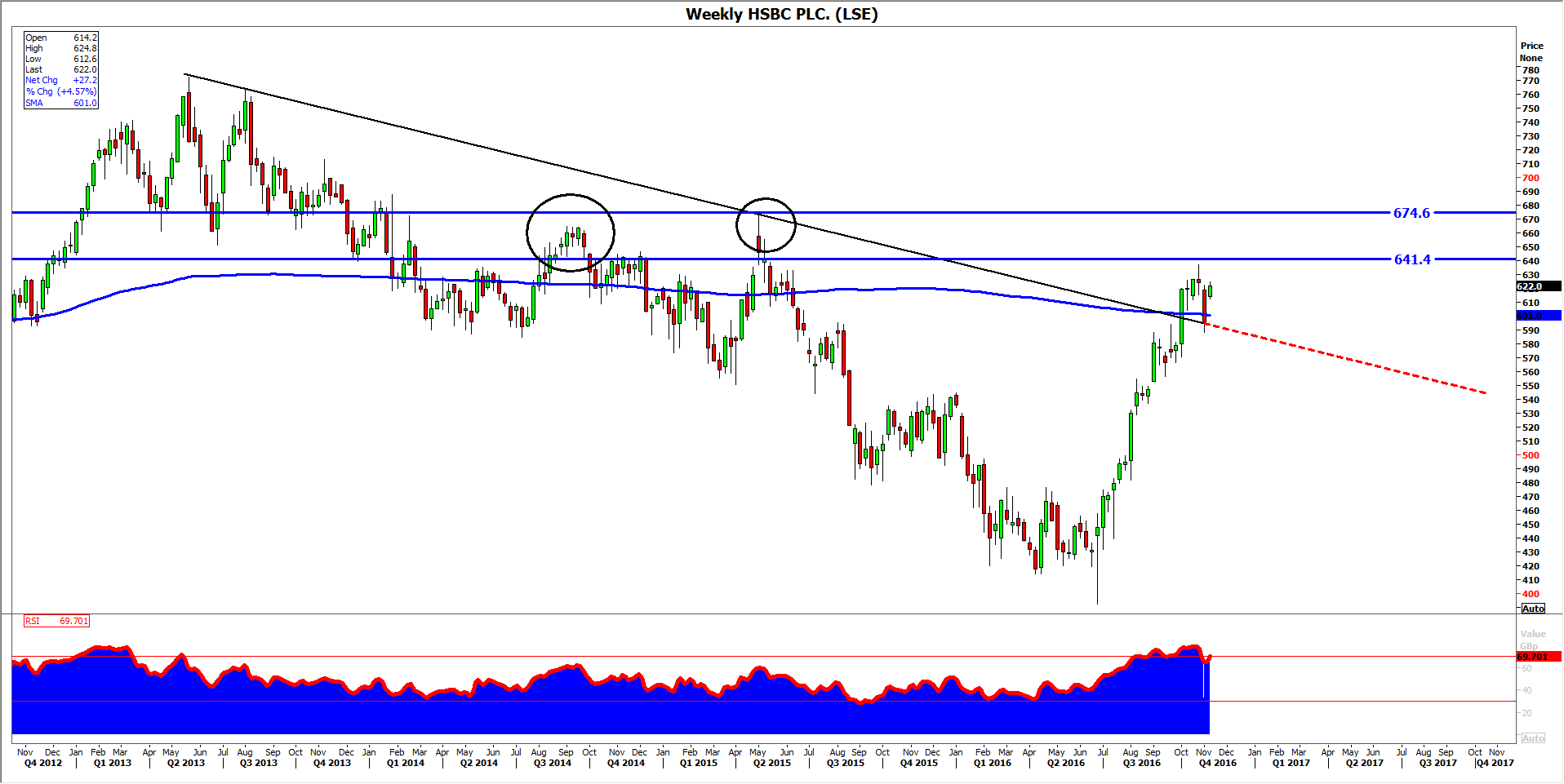

Please click image to enlarge