When:

Friday 22nd May

Friday 22nd May

What to expect ?

To say its been a turbulent year for the luxury retailer would be an understatement. With the US – Sino trade war, Hong Kong protests and now covid-19 to deal with, we can expect the results to reflect this.That said, Burberry’s behaviour through lockdown paints a picture of a company with financial resilience. Burberry has donated 100,000 PPE items to NHS, provided a base line salary for all UK workers who can’t work from home without government support, whilst senior staff have taken a 20% pay cut.

Retail sales slump

Retailers doors remain firmly shut in Europe and US owing to the coronavirus outbreak. Demand for luxury goods has also evaporated. The fact that Burberry has retooled a factory for PPE suggests that they don’t expect demand to pick up anytime soon.

According to the Office of National Statistics retail sales slumped by 5.1% in March, in the biggest decline in sales in the series 23-year history. Expectations are that retail sales in April will be even weaker as lockdown measures caused demand to vanish.

In late March Burberry released an update warning that it expected a 70% - 80% fall in sales in the final two weeks of March owing to coronavirus temporary store closures. Burberry also said that it expected this deep decline to result in a 30% fall in overall Q4 sales. After the firm quantified the expected hit to sales, the share price started to rise. There is nothing traders hate more than the unknown

Asia - China

Its impossible to look at Burberry without looking at China. China’s sales account for around 40% of total sales for Burberry. Hong Kong protests feel like an eternity ago, but they will have had an impact on sales as will the coronavirus lockdown in China at the start of the year.

Store in Asia are starting to reopen. Investors will be keen to hear how the reopening has been going in an attempt to gauge what can be expected from Europe and the US as lockdown measures are eased and stores reopen. According to China Luxury Advisors an independent consultancy, luxury consumer confidence is still down.

Its impossible to look at Burberry without looking at China. China’s sales account for around 40% of total sales for Burberry. Hong Kong protests feel like an eternity ago, but they will have had an impact on sales as will the coronavirus lockdown in China at the start of the year.

Store in Asia are starting to reopen. Investors will be keen to hear how the reopening has been going in an attempt to gauge what can be expected from Europe and the US as lockdown measures are eased and stores reopen. According to China Luxury Advisors an independent consultancy, luxury consumer confidence is still down.

Online Sales

Internet sales will also be closely eyed. These will give an idea as to whether customers shopping habits shifted to the internet during the lockdown or whether consumer decided to hold off from luxury purchases altogether.

Internet sales will also be closely eyed. These will give an idea as to whether customers shopping habits shifted to the internet during the lockdown or whether consumer decided to hold off from luxury purchases altogether.

Recession

It is also worth considering that the UK, Europe and the US are all heading towards a recession of historic proportions. Luxury items are unlikely to be top of many people’s shopping lists until there is more clarity over the economic outlook and until they have more job security. A quick rebound appears to be off the cards.

It is also worth considering that the UK, Europe and the US are all heading towards a recession of historic proportions. Luxury items are unlikely to be top of many people’s shopping lists until there is more clarity over the economic outlook and until they have more job security. A quick rebound appears to be off the cards.

Strong brands the other side

Research has indicted that those firms with a strong brand tend to recover more quickly from economic downturn. This is because in times of turmoil, those competitors with weaker brand cut advertising spend, reducing brand awareness There is no denying that Burberry has a very strong recognisable brand and given the challenging outlook, Burberry’s brand should work in its favour versus competitors.

Research has indicted that those firms with a strong brand tend to recover more quickly from economic downturn. This is because in times of turmoil, those competitors with weaker brand cut advertising spend, reducing brand awareness There is no denying that Burberry has a very strong recognisable brand and given the challenging outlook, Burberry’s brand should work in its favour versus competitors.

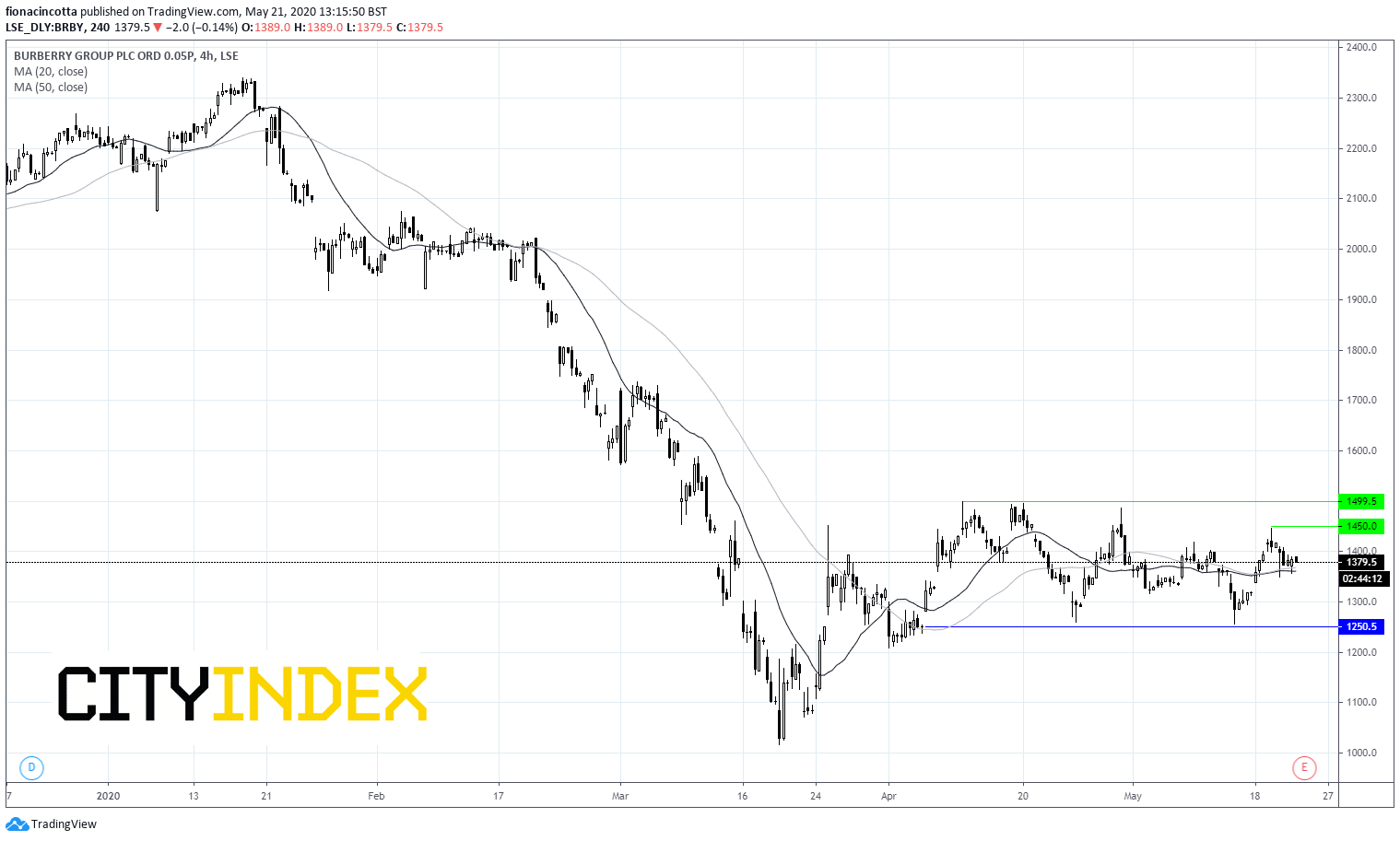

Chart thoughts

After picking up from the March low, Burberry’s recover stalled in early April. The stock has been trading within a familiar range of 1250p – 1500p for the past 6 weeks. It trades just marginally above its 20 & 50 sma on the 4 hour charts.

Even if results do disappoint, a break below 1250p would be need for a more convincing move southwards.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM