How the Carry Trade Could Explain EURUSD s Counterintuitive Moves and Why it Matters

Traders the world over have been surprised by the relative resilience of the euro over the last few weeks, despite growing concerns that Greece may […]

Traders the world over have been surprised by the relative resilience of the euro over the last few weeks, despite growing concerns that Greece may […]

Traders the world over have been surprised by the relative resilience of the euro over the last few weeks, despite growing concerns that Greece may default on its debt and be forced to exit the Eurozone (the feared “Grexit”). Analysts have proffered various explanations for the EURUSD’s durability: that the European financial system has had plenty of time to “ring fence” Greece and prevent contagion to other countries, that a last-second deal is imminent, or even that traders are just blithely underestimating the risk and damage of a Grexit.

One alternative explanation that we find particularly compelling is “Euro as a Funding Currency Theory.” As a reminder, the carry trade is when a trader borrows in (sells) a low-yielding currency and invests in (buys) a higher-yielding currency in an attempt to profit from the difference in interest rates. With the European Central Bank driving its main refinancing rate down to 0.05%, pushing its deposit rate all the way down to -0.2%, and engaging in large-scale quantitative easing, the euro represents the perfect funding currency for carry traders looking to borrow cheaply. Carry traders can then use these funds to invest in higher yielding currencies such as the New Zealand dollar, Turkish lira, or even the Russian ruble.

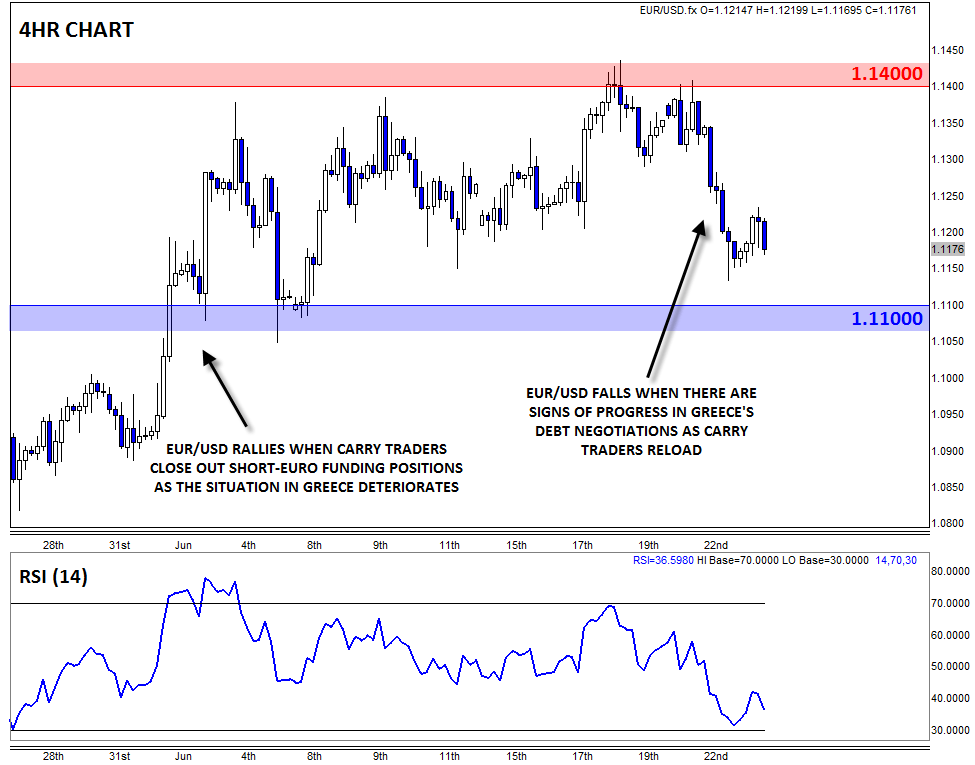

However, as all experienced traders know, every strategy comes with risks and the carry trade is no exception. As a general rule, carry traders prefer low volatility and predictable risks, lest adverse movements in the spot market overwhelm any gains from interest rate differentials. Unfortunately, the Greece’s debt drama has neither of those features, and the increasing concerns about Greece have prompted carry traders to reverse their trades by selling higher-yielding currencies and buying back the euro, even though the source of risk (Greece) emanates from the Eurozone itself.

The “Euro as a Funding Currency Theory” hypothesis succinctly explains the counterintuitive moves we’ve seen in EURUSD over the last few weeks. When it looks like Greece and its creditors are making progress on a deal, carry traders pile back in to sell the euro (as we saw yesterday), and conversely, when the negotiations suffer a setback (as we’ve seen repeatedly over the last few weeks, including earlier today), the euro sees a seemingly implausible rally. This theory also has empirical data to support it: though there’s no precise statistics on the prevalence of the carry trade at any given time, we have seen a dramatic reduction in euro short positions in the CFTC’s Commitment of Trader data over the last few weeks, confirming that many traders have reversed previous short positions in the single currency.

…So What Does This Mean for EURUSD?

Of course, this thought process only matters insomuch as it helps traders capitalize on market moves. In that vein, traders who anticipate an agreement between Greece and her creditors by the end of the month, even if it’s another last-second, kick-the-can-down-the-road type deal, may want to position for a possible fall in the value of the euro as carry traders resume selling. The key support level to watch near-term is 1.1100, which has put a floor under EURUSD month-to-date. Conversely, readers who think “this time is different” for the small Mediterranean country should be wary of a possible rally through 1.1400 resistance in EURUSD.