August 12, 2019 6:14 PM

Hong Kong Protests Help to Push NZD to Session Lows

Thousands of protesters poured into Hong Kong’s airport to hold demonstrations against the police, who protesters claim acted violently over their peaceful protests held over the weekend. Hong Kong airport authorities canceled all flights on Monday as protests continued. Authorities are still unsure as to if the airport will reopen on Tuesday. In addition, fears continued that tensions over the China-US trade war will continue to escalate. What does this mean for the Kiwi?

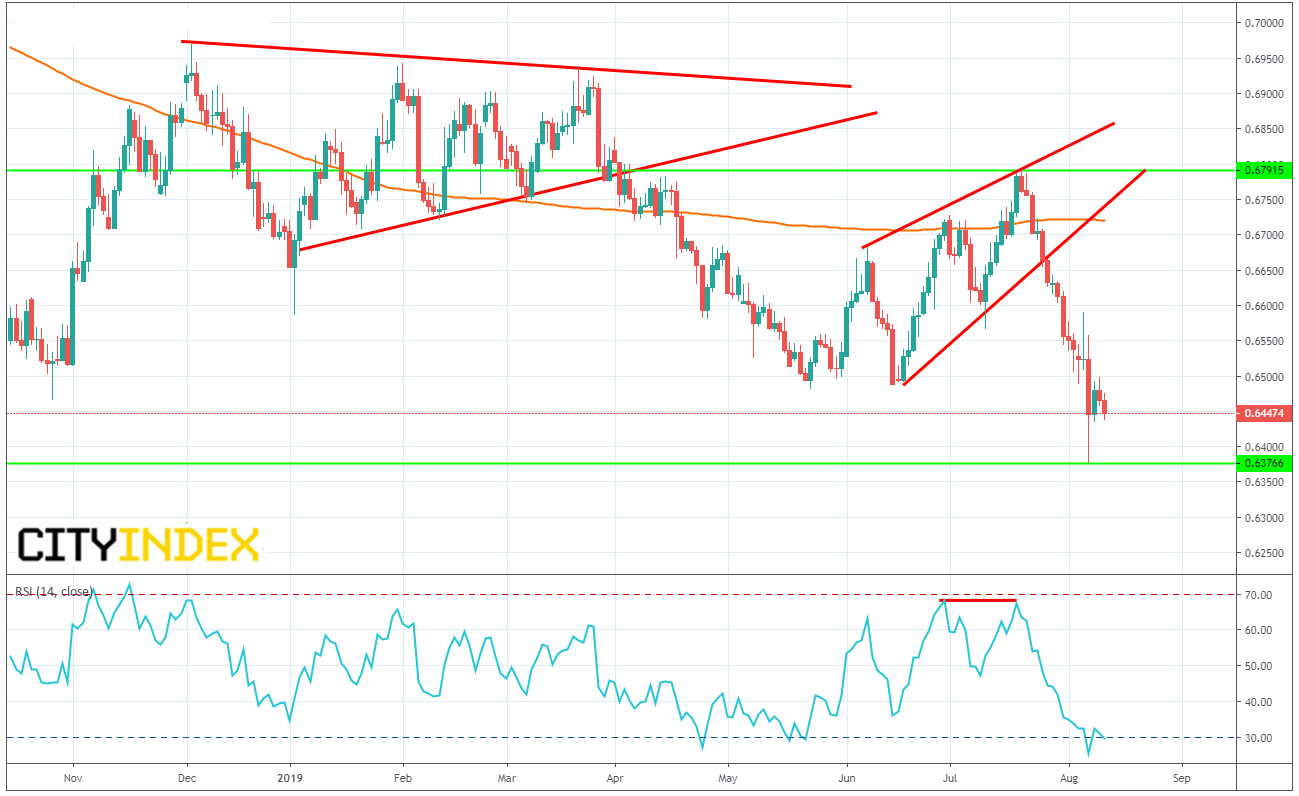

The latest problems pushed NZD/USD past the completion point of the rising wedge and now looks poised to test last week’s lows after only a minor bounce on Thursday….not to mention the surprise 50bps rate cut from the RBNZ last week (consensus was 25bps). Bearish kiwi traders may look to sell bounces towards 0 .6480.

Source: TradingView, City Index

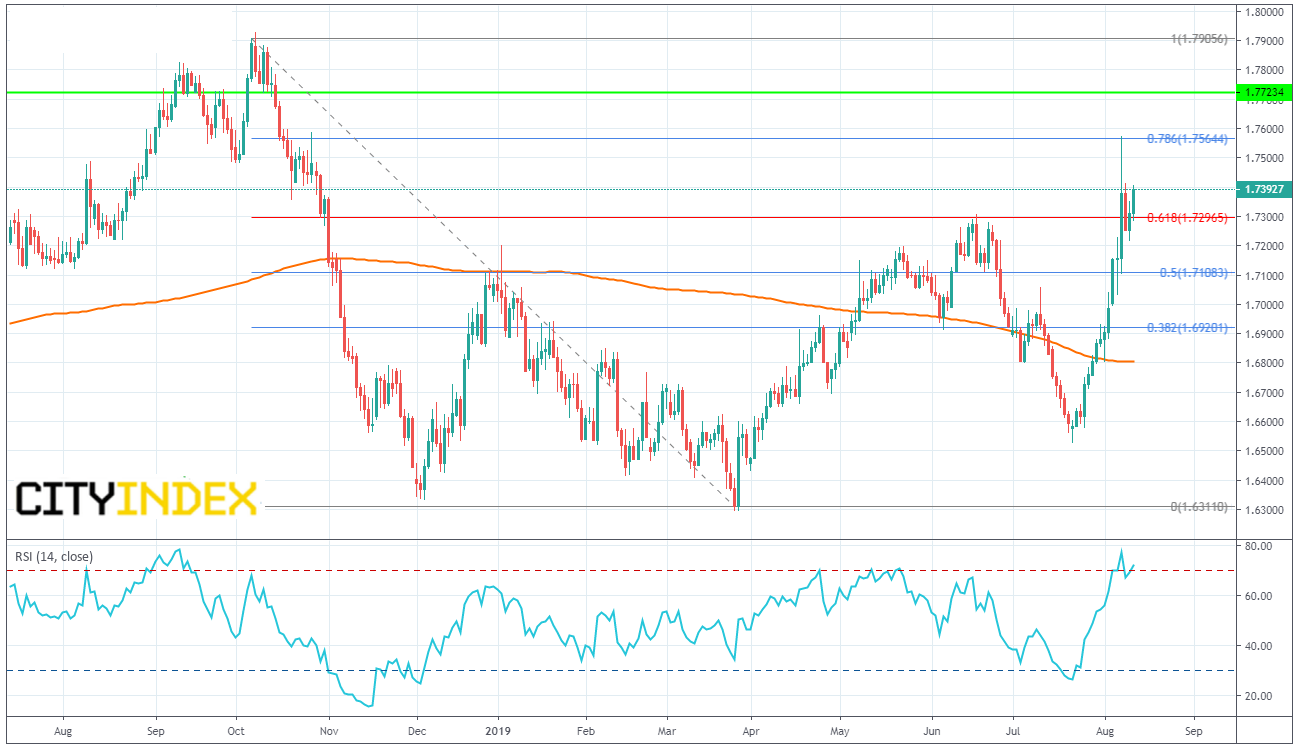

The same can be said for EUR/NZD, as we look to test last week’s breakout from Thursday at 1.7574. This level is also the 78.6% retracement level from the highs in October of 2018 to the lows of March 2019. Again, bearish kiwi traders may look to buy dips towards 1.7300.

Source: TradingView, City Index

If the protests in Hong Kong continue to worsen, watch for a continued selloff of NZD!

Latest market news

Today 08:15 AM

Latest Forex articles

Yesterday 11:09 PM

Yesterday 04:00 PM