Home Retail shares dragged by Argos as it squares up to Amazon

Home Retail Group’s first-quarter sales show that Argos continues to be a drag. Poor-selling electrical categories pushed sales at stores open more than a year […]

Home Retail Group’s first-quarter sales show that Argos continues to be a drag. Poor-selling electrical categories pushed sales at stores open more than a year […]

Home Retail Group’s first-quarter sales show that Argos continues to be a drag.

Poor-selling electrical categories pushed sales at stores open more than a year 3.9% lower than in Q1 2014, 20 basis points lower than market expectations.

The Homebase DIY business performed much better with a 5.4% jump in same-store sales compared with just0.8% expected.

Homebase’s gross margin was an impressive 175 basis points better during Q1, which covered the 13 weeks that ended on 30th May.

Argos’s gross margin fell 50 points.

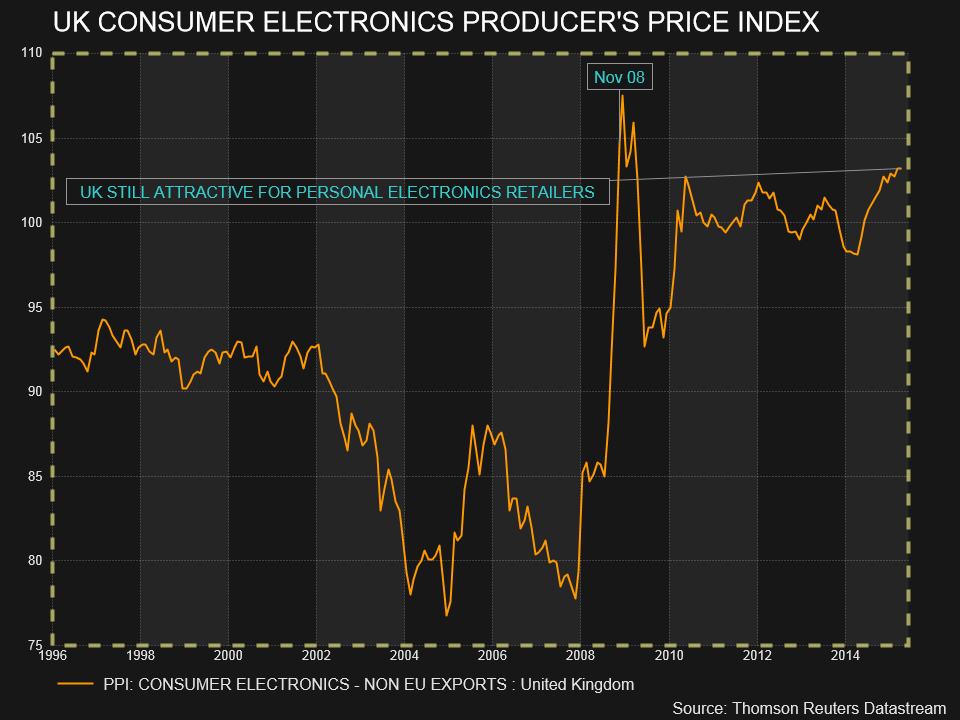

Argos’s persisting weakness looks at least partly like a continuation of the squeeze from rival retailers of consumer electronics retailers, perhaps especially Carphone Warehouse, which we know has almost certainly grabbed market share from the entire sector over the last several months.

Home Retail blamed falling demand for TVs and tablet computers.

It had already warned in April that first-half sales at the in-store catalogue-style retailer would probably decline this year as it shakes-up its format, and from the effect of flighty consumer demand.

It wants to pivot Argos deeper into digital retailing, looking for an expanded focus on higher-margin mobiles and tablet PCs whilst speeding up collections.

Obviously, Home is very much aware of actual and future potential incursions into its major segments from a rapidly (and fiercely) expanding eCommerce sector, namely Amazon.

click for larger image

It is the e-tailing conglomerate giant that may represent the biggest threat to Argos and that is why Home Retail is sacrificing large chunks of margin each quarter (-50 basis points at Argos versus +175 basis points at Homebase in Q1) to achieve its aim of a leaner, more Internet-based consumer electronics business.

Ironically, during this drive, HRG’s erstwhile slower growing DIY arm starts to look a lot more solid and dependable, though it’s worth remembering Homebase still represents little more than 20% of HRG’s revenues compared to Argos at 76%.

Therefore, whilst management has this morning reassured that it “does not expect (a) change to analysts’ FY consensus forecast for pre-tax profit”, that does not rule out a slight downgrade to those expectations.

The market broadly sees the pre-tax profit for the year ending in February 2016 at £131.52m after £132.1m in the year that ended in February. I wouldn’t be surprised to see the net effect of the struggles at Argos take as much as 5% off the consensus for the current financial year.

And, given that HRG’s transformation strategy centred on Argos was a five-year plan that kicked-off in 2012, margin contraction on the high street and at HQ looks to be on the cards for at least two more years, assuming perfect execution.

Under these circumstances it appears unlikely Home Retail shares can progress much higher than the descending channel the price entered in least late November last year.

If I’m correct, the advance off lows close to 150p which started a few days ago might well stall between 168.7p to 174p at best, though the stock does currently have a moderate tailwind, judging by the tone of the stochastic chart.

Home Retail Group stock had a lead of as much as 3.4% earlier on Thursday, but that slipped to below 1% above Wednesday’s close at the time of writing.

click for larger image