Historical analysis shows the FTSE traditionally rallies from September to year end

The traditional ’sell in May and go away, come back again on Labor Day‘, holds true when taking historical price trends into account and may […]

The traditional ’sell in May and go away, come back again on Labor Day‘, holds true when taking historical price trends into account and may […]

The traditional ’sell in May and go away, come back again on Labor Day‘, holds true when taking historical price trends into account and may help to inspire a bit of confidence as the final quarter of the year approaches.

Labor Day falls on the first Monday of September each year, which for 2012, is today. The idea behind the traditional tagline is that equity markets typically find pressure between May and the end of August, but rally from September until the end of the year.

So let’s look at the data.

This year, the FTSE 100 fell 0.45% from May until August, thanks in part to resurgence in optimism towards additional stimulus measures which many investors believe will be announced by the ECB and, to a lesser extent, the People’s Bank of China and the US Federal Reserve.

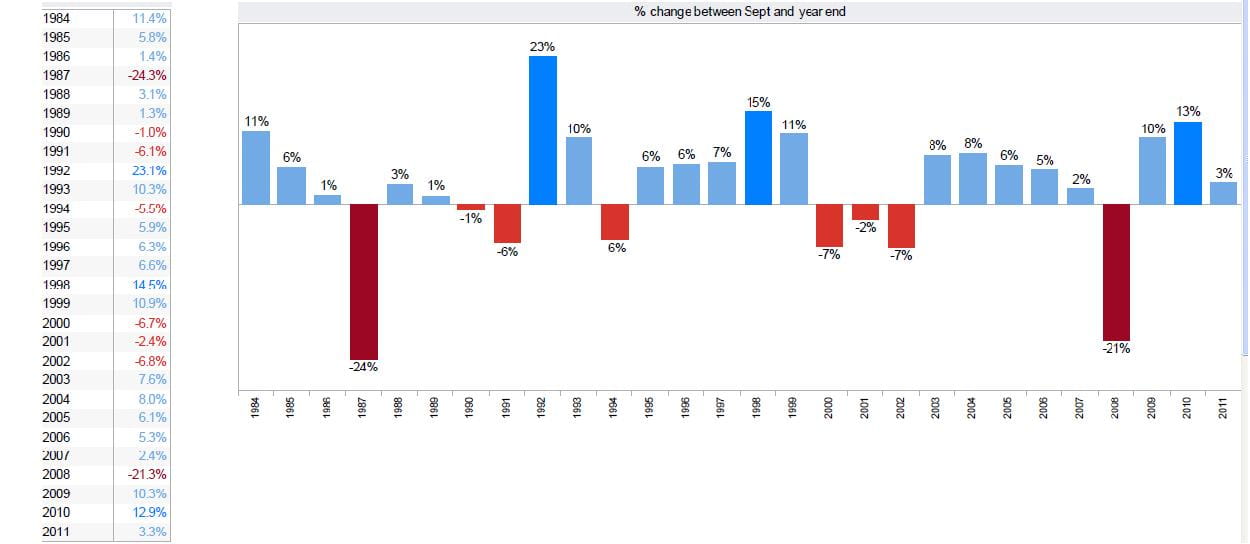

So how does September to year end equity performance typically fare? The answer is fairly bullish. On the FTSE 100, of the last nine years between September and the year end, the FTSE has rallied eight times, netting average gains of 7%. When looking even longer into history, the FTSE has rallied 20 times (or 71% of the time) in the last 28 years. For each year the FTSE 100 has rallied, the average gains have been 7.8%, with the best yearly performance being in 1992, when the FTSE rallied 23.1%. However, when the FTSE has actually bucked the historical trend and fallen between September and year end, the Index has fallen an average 9.3%, with the worst performances being in 1987, when the FTSE lost 24.3% and in 2008, when the FTSE fell 21.3%, albeit on both of those occasions the markets were suffering from severe shocks.

So what may lie in store for this year end?

There are some important variables to consider for this year, including the European debt crisis, the US presidential election, the Troika ruling on Greece and perhaps even more importantly for near term sentiment, central bank stimulus plans.

Much of the market is awash with speculation as to whether central banks will seek to ignite the markets with further stimulus.

Flagging Chinese growth and manufacturing data has continued to apply pressure on the People’s Bank of China (PBOC) to stimulate activity going into the year end. Indeed, just this week China’s Premier Wen Jiabao stated that they could use the 100bn yuan ($16bn) left in the fiscal stability fund to curtail against slowing growth. China still maintains that they expect growth of 7.5% this year, a marked slowdown from 9.2% a year earlier. China has moved to stimulate the markets on two fronts previously; interest rate cuts and infrastructure spending. Whilst it appears the door remains open for both of these elements, stronger than expected Chinese inflation in August at 0.6% remains an area of doubt as to whether China will continue to cut interest rates.

Given the fact that the Chinese economy has an important influence on the prospects of the FTSE 100, given that the industrial nation plays a major role in metal demand. Further, as many miners such as Rio Tinto, BHP Billiton and Xstrata bear a heavyweight influence on the FTSE 100 Index, a bullish mining sector can also be fruitful for the performance of the UK benchmark Index. As such, it is Chinese policy that is likely to have a big impact on how the FTSE trades to the year end.

See Peter Esho’s article on ‘is the Chinese growth story over‘ for a more in depth view of the Chinese economy.

The recent announcement of Outright Monetary Tranactions (OMT) by the European Central Bank to buy stressed bonds of up to 3yr maturities at the specific request for aid by countries is a much needed form of stimulus in the euro area. The smooth passing through the German constitutional courts of the ESM has helped to remove an air of doubt as to whether the ESM can start to be used. Yet there will likely be some political manoeuvring to be done before countries will likely tap the ECB to buy their bonds, as the ECB would require formal requests before doing so, and the acceptance of those requests will come with conditions that governments may find difficult to accept. Spain remains a key area to watch in this regard.

Add to this the fact that the Bank of England is likely to increase asset purchases before the year is out and that the Fed may announce a third phase of quantitative easing as early as tomorrow, it’s easy to see how expectations of global stimulus are likely to play a major role in how equities perform into the year end. If the Federal Reserve does announce an aggressive form of stimulus, that could be a real game changer.

Yet it is also important to consider the implications of the US Presidential election in November, and the likely consequences of manifesto pledges on equities, specifically defence spending, financial stocks and pharmaceuticals. A key element to the election will be spending and budgetary controls, as well as taxation, which could leave broader implications to the US’s credit rating by ratings agencies.

So as we progress to the end of the year, keep an eye on these elements which are all likely to play a key role in whether the historical trend of a stronger FTSE 100 between September and the year end continues.