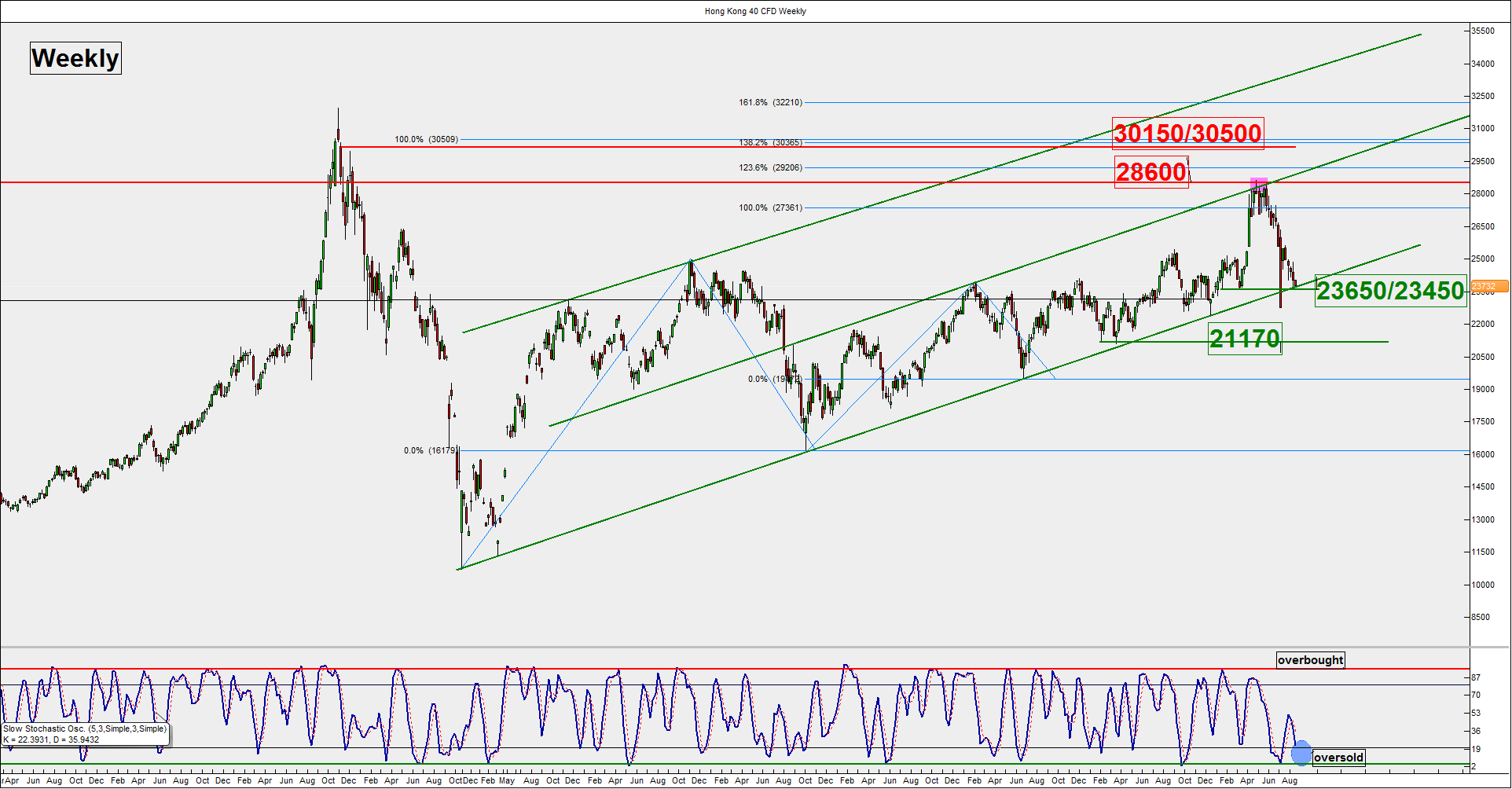

Hang Seng Index Weekly Outlook for 17 Aug to 21 Aug Hovering above the 23450 long term key support

(Click to enlarge charts) What happened earlier The Hong Kong 40 Index (proxy for the Hang Seng Index) has continued to drift sideways below the […]

(Click to enlarge charts) What happened earlier The Hong Kong 40 Index (proxy for the Hang Seng Index) has continued to drift sideways below the […]

(Click to enlarge charts)

(Click to enlarge charts)

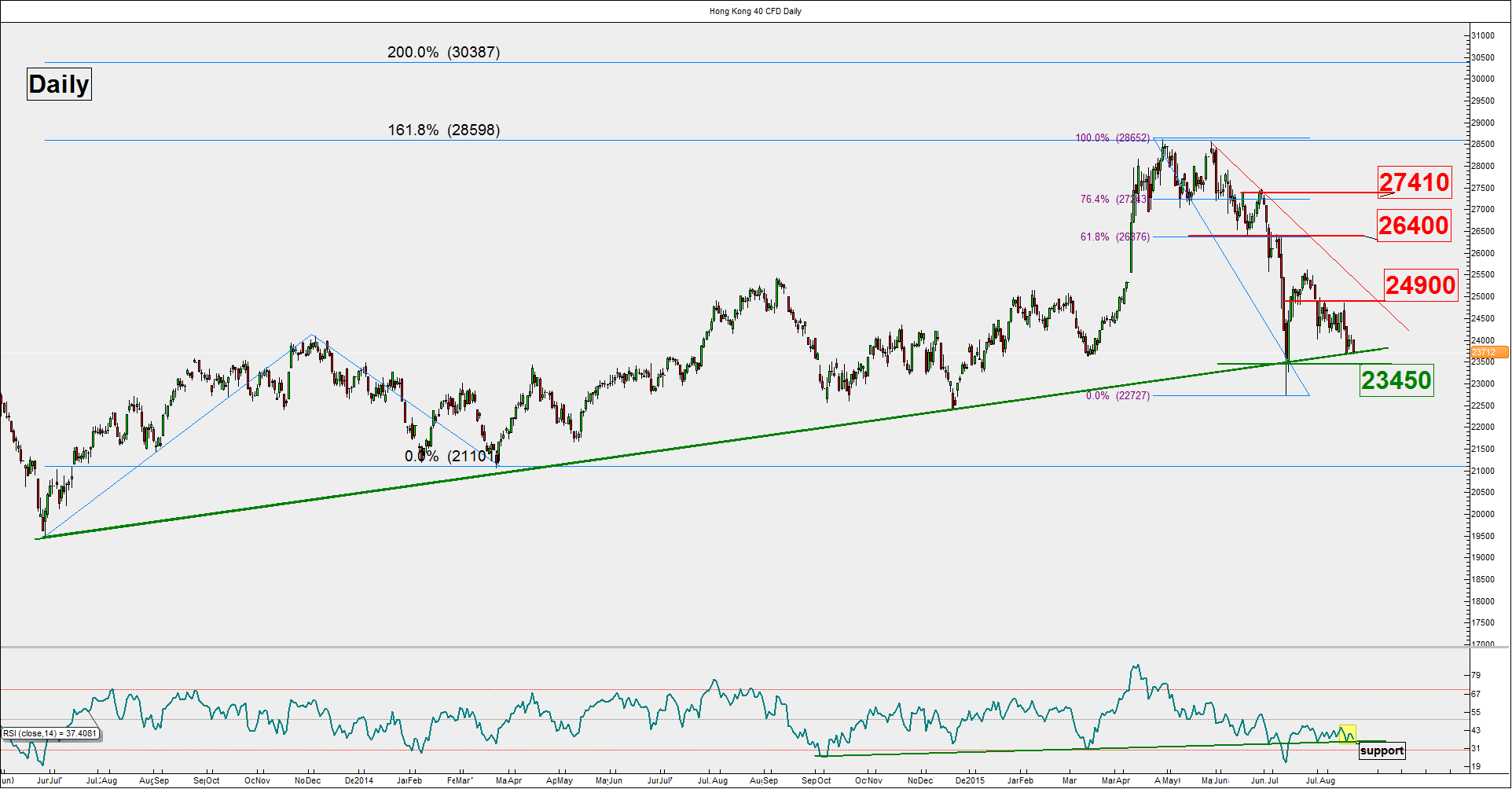

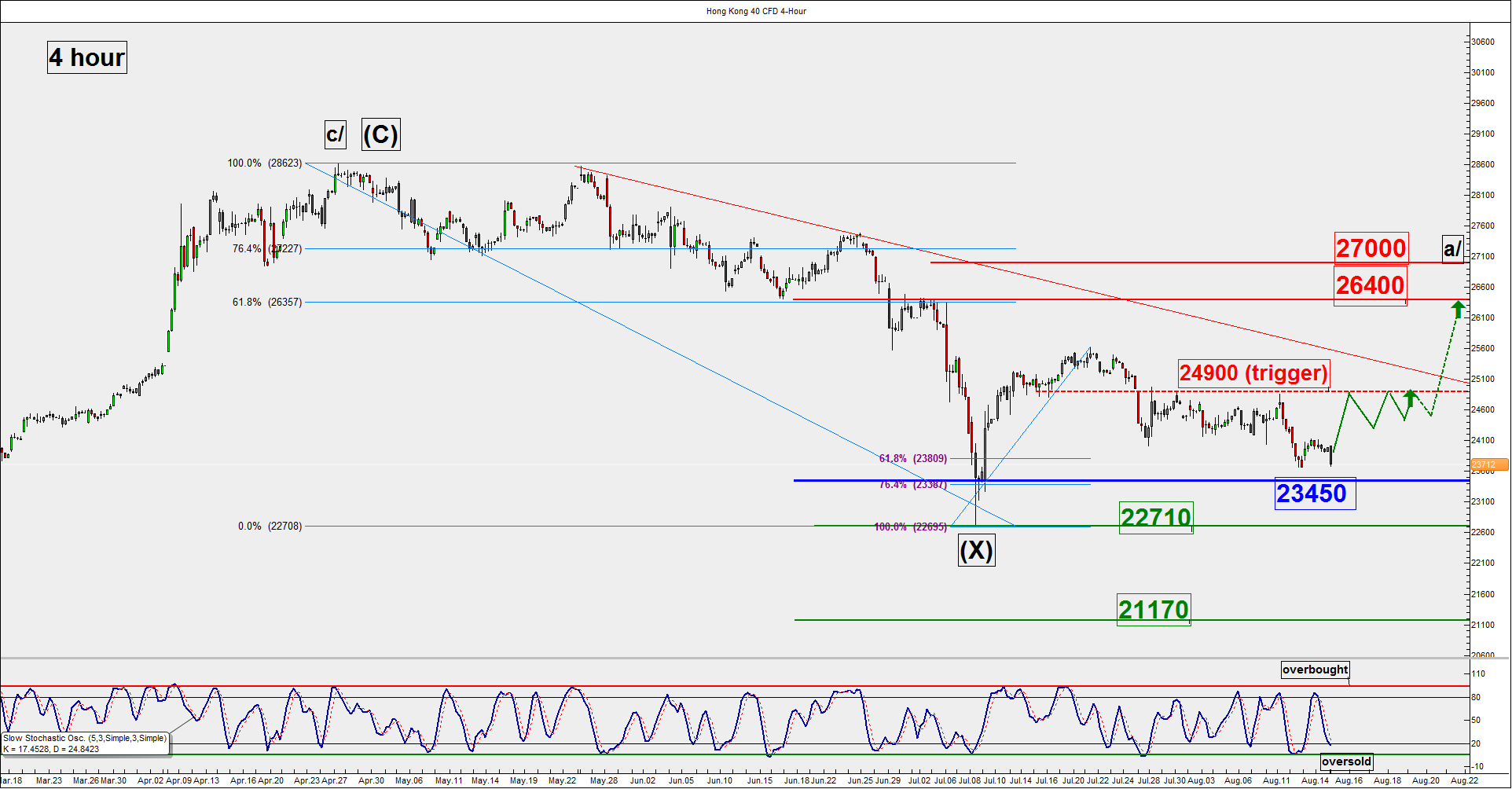

The Hong Kong 40 Index (proxy for the Hang Seng Index) has continued to drift sideways below the 24900 potential medium-term upside trigger level.

Please click on this link for more details on our previous weekly outlook.

*Please note that the weekly candlestick for 06 July to 10 July 2015 is erroneous as it did not have a weekly close below the 23450 support. This error will be rectified as soon as possible.

Pivot (key support): 23450

Resistance: 24900, 26400 & 27000

Next support: 22710 & 21170

The Index is now back at its key inflection level of 23450 (the long-term key support as aforementioned) but lack of upside momentum to push up and form a new swing high.

Thus, the 24900 range top remains the key intermediate resistance that the Index needs to breakout in order to gain inertia for a potential upside movement to target 26400.

On the other hand, failure to hold above the 23450 weekly pivotal support is likely to damage the long-term bullish trend and see the start of severe correction towards 22710 before 21170 in the first instance.

Disclaimer

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this email, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs. All queries regarding the contents of this material are to be directed to City Index, a trading name of GAIN Capital Singapore Pte Ltd.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit cityindex.com.sg for the complete Risk Disclosure Statement.