Goldman JPM Citi earnings rise despite 8216 new normal 8217 banking era

Globally reaching US banks will draw into sharp focus this week as a raft of them report first-quarter earnings. JPMorgan Chase, and Bank of America […]

Globally reaching US banks will draw into sharp focus this week as a raft of them report first-quarter earnings. JPMorgan Chase, and Bank of America […]

Globally reaching US banks will draw into sharp focus this week as a raft of them report first-quarter earnings.

JPMorgan Chase, and Bank of America will unveil results on 14th and 15th April respectively, and Goldman Sachs and Citigroup will follow on 16th.

Whilst the years of financial sector slump garnished by ratcheted-up regulatory heat are not quite over yet, revived trading results and a rise in M&A advisory deals are expected to have boosted the bottom line of household-name US investment banks.

The banks with most currency trading exposure, JPMorgan and Goldman, may, in theory, be among the largest beneficiaries of significant volatility in currencies precipitated by the Swiss National Bank’s unexpected abandonment of its currency peg against the euro, in January.

However, the extent to which any gains were offset by unforeseen losses related to the SNB event is unclear in most cases.

For instance, even though Citigroup is less geared to trading than macroeconomic business, it is known to have suffered losses of about $300 million from the Swiss franc fiasco.

This uncertainty over trading gains is another signifier of the ‘new normal’ in investment banking.

Big currency swings of the kind seen over the last few months would ordinarily have been expected to provide a more or less outright boost to earnings for global banks.

But now, significant spikes in volatility no longer guarantee an uptick in bank profits, as was traditionally the case, with many of the larger investment banks having scaled back riskier businesses.

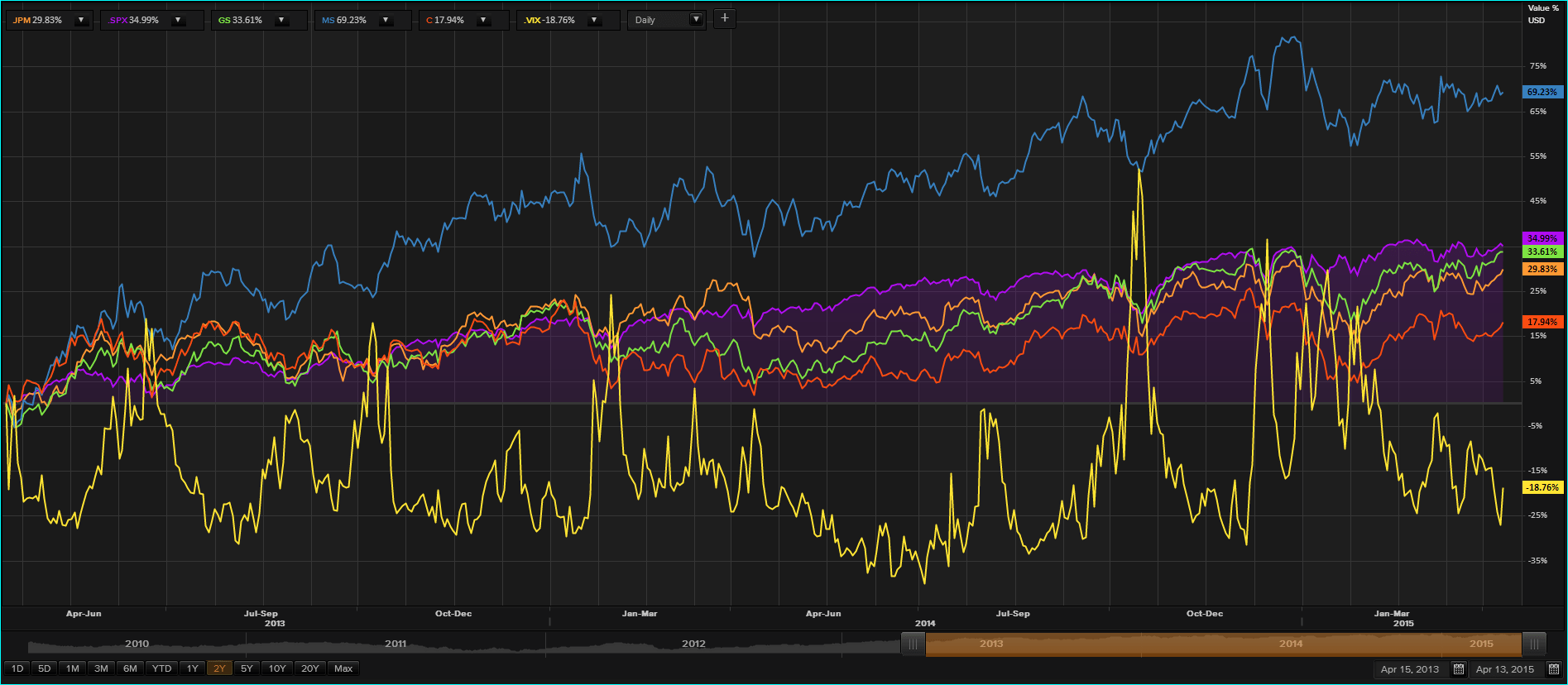

In my chart below, I rebase the stock prices of the banks mentioned in this article to zero, revealing relative performance over two years.

I’ve included the Chicago Board Options Exchange VIX index of volatility (bright yellow).

As can be seen, not only did the sharpest upticks in volatility not result in strong jumps in any of the stock prices, in fact, something moderately inverse seems to have happened.

The chart also reveals that among the giant US banks, the star stock performer over the last two years has been Morgan Stanley.

It also performed almost twice as well as the S&P 500 stock index during that time.

(Please click image for magnified view)

Key

JPM – JPMorgan

SPX – S&P 500 index

GS – Goldman Sachs

MS – Morgan Stanley

C – Citigroup

VIX – CBOE Vix Volatility Index

The start of the European Central Bank’s €60bn per month bond-buying program in March was a more predictable source of volatility for banks and therefore, perhaps more profitable.

Fixed-income, commodity and currency trading revenues are at least likely to be stronger than those from credit and mortgage product activities which continue to largely contract at the big banks.

Goldman, Morgan Stanley and JPMorgan, with their well-known slant towards equity derivatives can be expected to have benefited from rising stock markets and episodes of strong volatility during Q1.

Looking at M&A, corporate activity data service Dealogic estimates advisory revenues from such businesses increased 9% in Q1.

Similarly, the mini booms in IPOs, buybacks and other stock offerings ought to feed through to increased equity fees.

With credit markets off their peaks though, debt market revenues will not be as strong.

(Please click image for magnified view)