Gold won t burnish Anglo American finals

Most inveterate gold bugs are aware of Dr Franz Pick, a Post-War sensationalist advocate of gold as global currency. It’s Dr Pick to whom the […]

Most inveterate gold bugs are aware of Dr Franz Pick, a Post-War sensationalist advocate of gold as global currency. It’s Dr Pick to whom the […]

Most inveterate gold bugs are aware of Dr Franz Pick, a Post-War sensationalist advocate of gold as global currency.

It’s Dr Pick to whom the bold claim “The dollar will be wiped out” is often attributed, though the provenance is as dubious as the not-so venerable analyst himself.

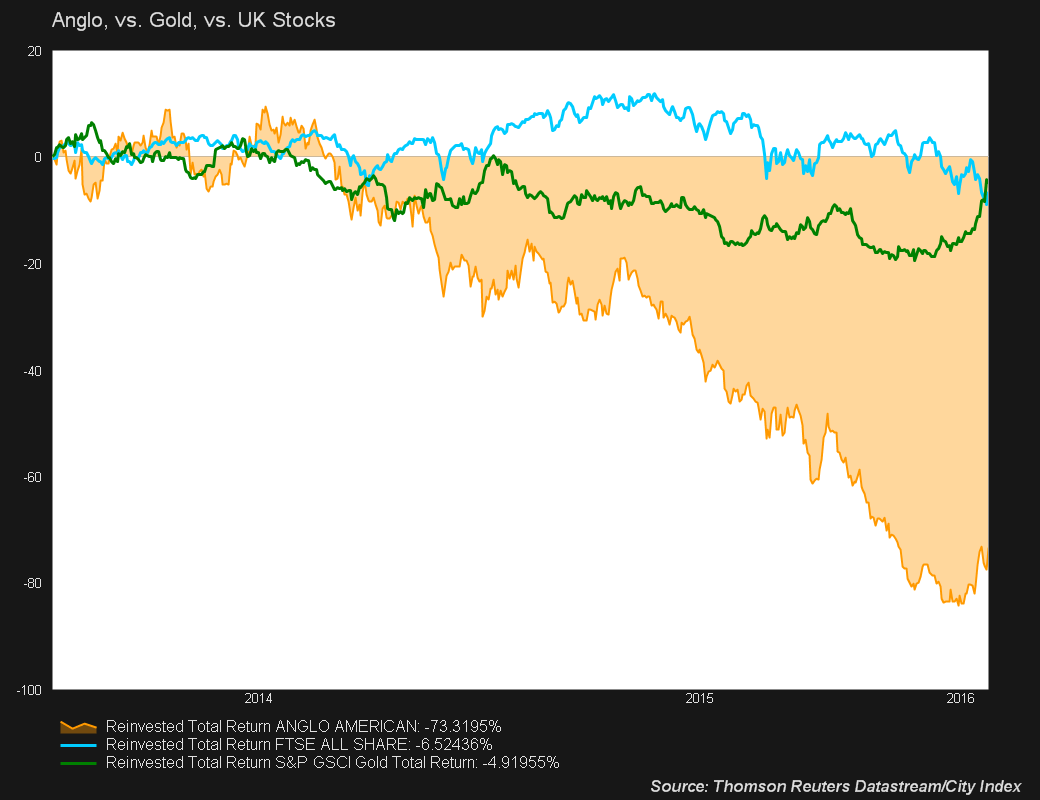

Either way, whilst the end of the dollar’s ‘secular bear trend’ played havoc with gold, the metal has still bested all speculation on mining shares of late.

It’s a particularly sore point for investors in Anglo American Plc., which used to produce most of the world’s gold and remains among the Top Ten gold miners.

Please click image to enlarge

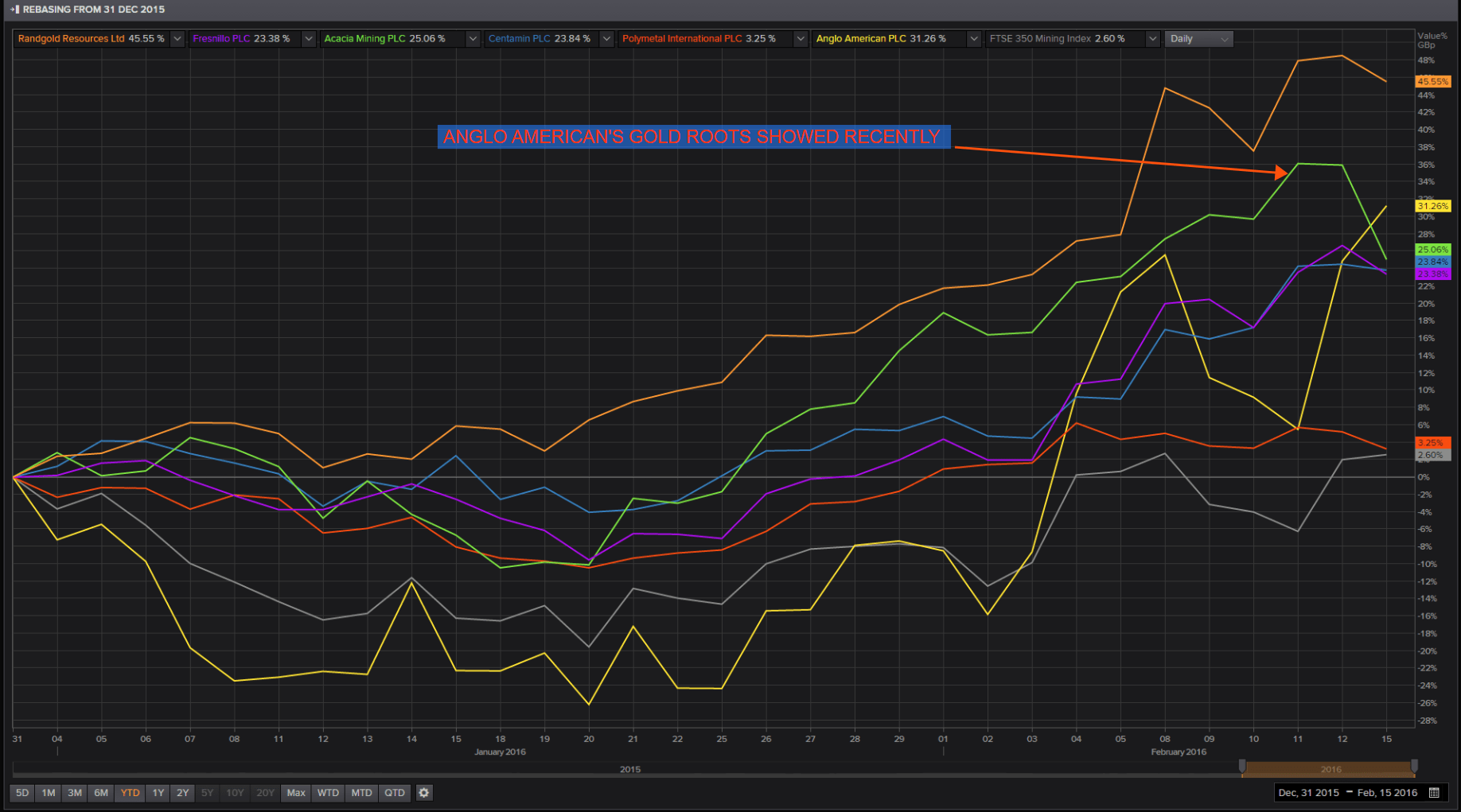

Despite terrible longer-term returns, Anglo shares outperformed fellow FTSE 100 miners last month, and Anglo has also held its own against the wider sector so far in 2016.

Please click image to enlarge

A short squeeze following a 75% loss last year, exposure to the most favourable dollar/rand exchange rates in history, and a frenzied re-organisation and disposal programme, boosted the company that still produces most of the world’s platinum.

But none of that will put a gloss on its final results due on Tuesday 16th February.

Any hopes that a recent strong showing by the sector would last, after gold prices rose sharply last week, were dashed on Monday.

An aggressive ‘risk-on’ rally across Europe saw gold and gold miners lose favour.

And although rating agency changes are notorious for lagging the market, a downgrade of Anglo’s rating deeper into ‘junk’ by Moody’s, was an additional caution.

With sobering results from subsidiaries AngloGold, Anglo American Platinum, and Kumba Iron Ore, already released, the sting from dire group figures has already been clipped.

However, earnings from Rio Tinto last week underlined that even apparently ‘priced-in’ results can still unpleasantly surprise investors on the day.

A dividend re-think was pivotal in Rio’s case.

AAL’s yield—recently 4.5%—isn’t flashing a warning for the 2015 pay-out, unlike that of its peer group which averages about 8%.

But any undershoot in Anglo’s spot prices for the year will be in focus for the FY 2016 dividend.

We estimate that a $3.75bn capital expenditure would eat into approximate $16.6bn credit/short-term liquidity to the tune of $1.5bn, but still leave room to maintain dividends costing about $1.1bn.

Scrub that if commodity prices deteriorate any further.

Capex and price forecasts will therefore be a major focus for Tuesday.

Here are the main Full-Year (FY) 2015 figures investors are expecting, according to Thomson Reuters.

Additionally, investors won’t scrimp on sharp scrutiny of Anglo’s performance on cash and costs, after it made several announcements on restructuring in recent months.

Anglo is expected to announce a total mining cash cost of $36m though it didn’t break out a group figure a year ago.

Even so, total group production costs are expected to have been slashed by 13% to $19.6bn, partially helped by the weak rand.

The final cash balance won’t look as promising.

It might be booked as much as $169m in the red, after a negative balance of $137m was reported at the end of the year before.

Net debt may only tick 1% lower to $12.7bn, if pessimistic market forecasts prove correct.

At the same time, Anglo might write off as much as $2.6bn, moderately less than it did in FY 2014.