Gold US rate rise may push metal to 1000

So, the ‘FOMC day’ has come to pass and the rate hiking cycle has begun, as had been widely expected. It looks like the majority […]

So, the ‘FOMC day’ has come to pass and the rate hiking cycle has begun, as had been widely expected. It looks like the majority […]

So, the ‘FOMC day’ has come to pass and the rate hiking cycle has begun, as had been widely expected. It looks like the majority of the market participants have interpreted the Fed’s forward guidance as more hawkish than expected – hence the dollar has rallied, if only moderately so far. Remarkably, gold also managed to end Wednesday’s session higher. But was that the bull’s last hurrah? The precious metal had already given up its entire weekly gains by Thursday afternoon, when this report was written.

This time of the year is usually a happy occasion but surely that’s not how the gold bugs must be feeling right now. As we head into the penultimate week of 2015, the remainder of this year’s economic calendar is unsurprisingly populated with more “bank holidays” than macro data. Thus, there is little macro reasons to help change the direction gold is currently heading towards. Trading conditions are likely to be quieter as speculators wind down ahead of the festive period, but long term trends are unlikely to be affected much. If anything, they are most likely to continue, which means we could see firmer dollar and even weaker gold prices over the next few weeks.

Indeed, if the market strongly believes that the Fed will continue to raise rates as per the FOMC’s dot plots, then the dollar may continue pushing a lot higher since most other major central banks are still very dovish. This is not good for assets that are denominated in the dollar, especially gold and silver. Unlike bonds or equities, the metals pay no interest or dividends, and cost money to store. However, if the stock markets start to roll over, say on concerns about the impact of the stronger dollar on future company earnings, then some of the USD’s impact will be neutralised, causing gold to potentially bounce back on safe haven flows. However, inflation is still non-existent for most major economies and until it starts to rise more noticeably gold is unlikely to show major reactions to short term equity market volatility.

The very long term outlook for the metal is still bullish however because of the strong physical demand from central banks and consumers, most notably in India and China. But not many people are currently focusing much on the physical aspects, especially since the paper market (futures and options) is comparatively huge. Thus, for now the short-term outlook remains bearish – and not just from a fundamental point of view.

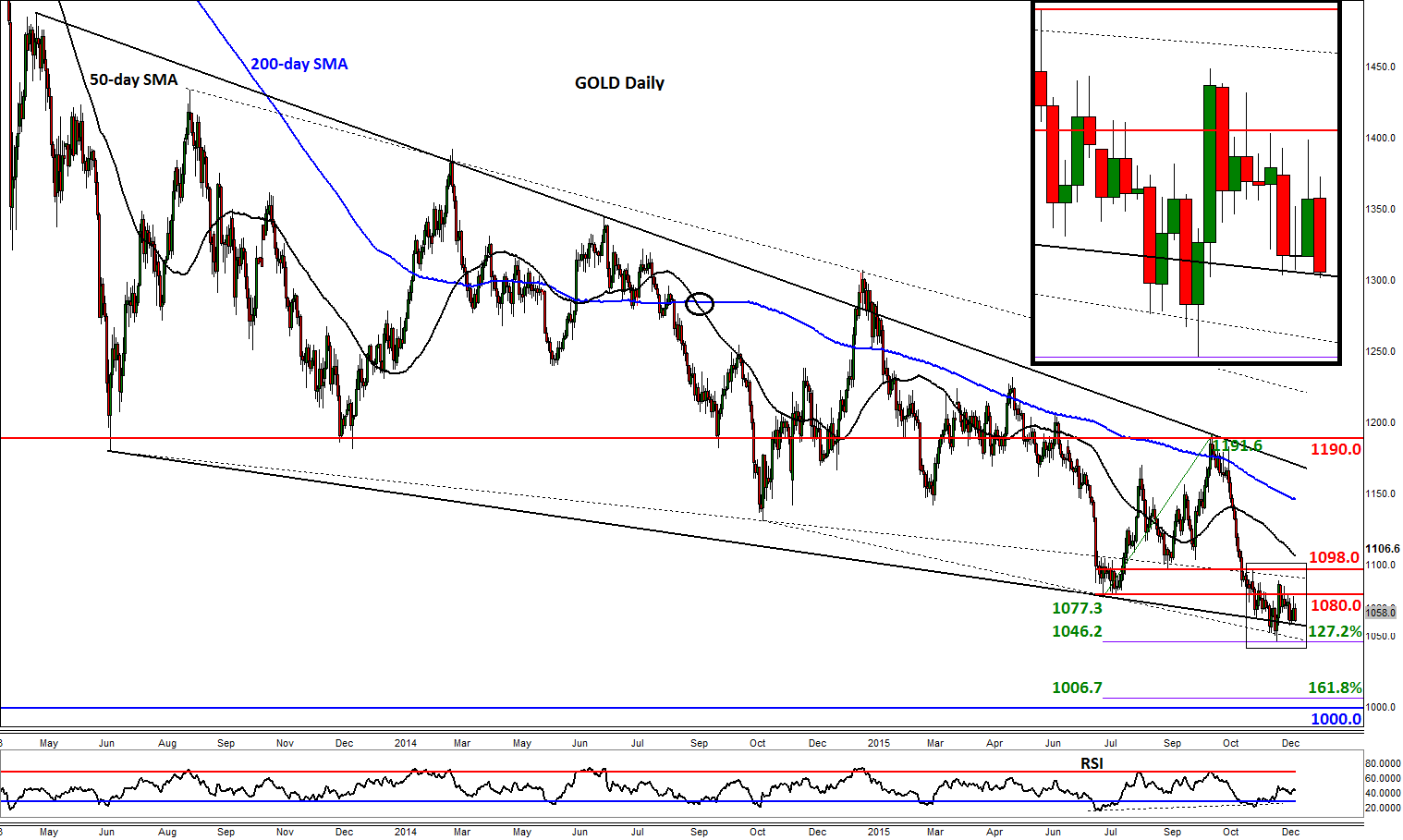

Indeed, from a technical perspective, there are not a lot of bullish indications to be seen when looking at a chart of gold. Granted, the daily RSI may be in a state of positive divergence with price, suggesting that the bearish momentum is weakening, but the start of the Fed’s hiking cycle could lead to renewed selling pressure once more. Gold is currently hovering dangerously around the lower trend of its long-term triangle pattern after it failed to hold conclusively back above the broken support at $1080, which remains a key short-term resistance level. Other near-term resistances include $1098 and the 50-day average at $1106/7. If the aforementioned trend line breaks down, gold may break last month’s low and the 127.2% Fibonacci extension level at $1046, before potentially dropping towards the 161.8% extension level at $1006/7 next. The psychologically-important $1000 handle is thus also in sight now.