Gold undermined by rallying equities dollar

The rallying equity markets and firm US dollar is proving to be a toxic mix for the buck-denominated and perceived safe-haven gold. After eking out […]

The rallying equity markets and firm US dollar is proving to be a toxic mix for the buck-denominated and perceived safe-haven gold. After eking out […]

The rallying equity markets and firm US dollar is proving to be a toxic mix for the buck-denominated and perceived safe-haven gold. After eking out a small gain for the month of July, the metal started August on the front foot last week before turning decisively lower on Friday in response to the US jobs report, which came out much stronger than expected. The precious metal has started the new week a touch weaker today, but unfortunately things could turn ugly for gold in the days and weeks to come.

While the historically low and negative yields are meant to be positive for non-interest bearing assets like gold and silver, unfortunately for the metals, this is an even more positive environment for the higher-yielding equity markets. In addition, US quarterly earnings results have been generally better than expected, making equity more attractive than safe haven assets. What’s more, the dollar has been able to maintain its bullish bias on renewed speculation about another rate increase from the US Federal Reserve later this year after the weakness in the jobs market at the start of the summer proved to be a blip rather than a change in the trend. Other macro pointers from the world’s largest economy have generally been positive, too. This week we will find out – in the form of retail sales, consumer sentiment and retail earnings results – whether the strength in the labour market has been strong enough for the American consumers to loosen up their purse strings. If so, one would think that both the US dollar and equity prices will be able to extend their gains, which should be further bad news for gold. Conversely, gold could find some support if there is no evidence of rising consumer spending and confidence.

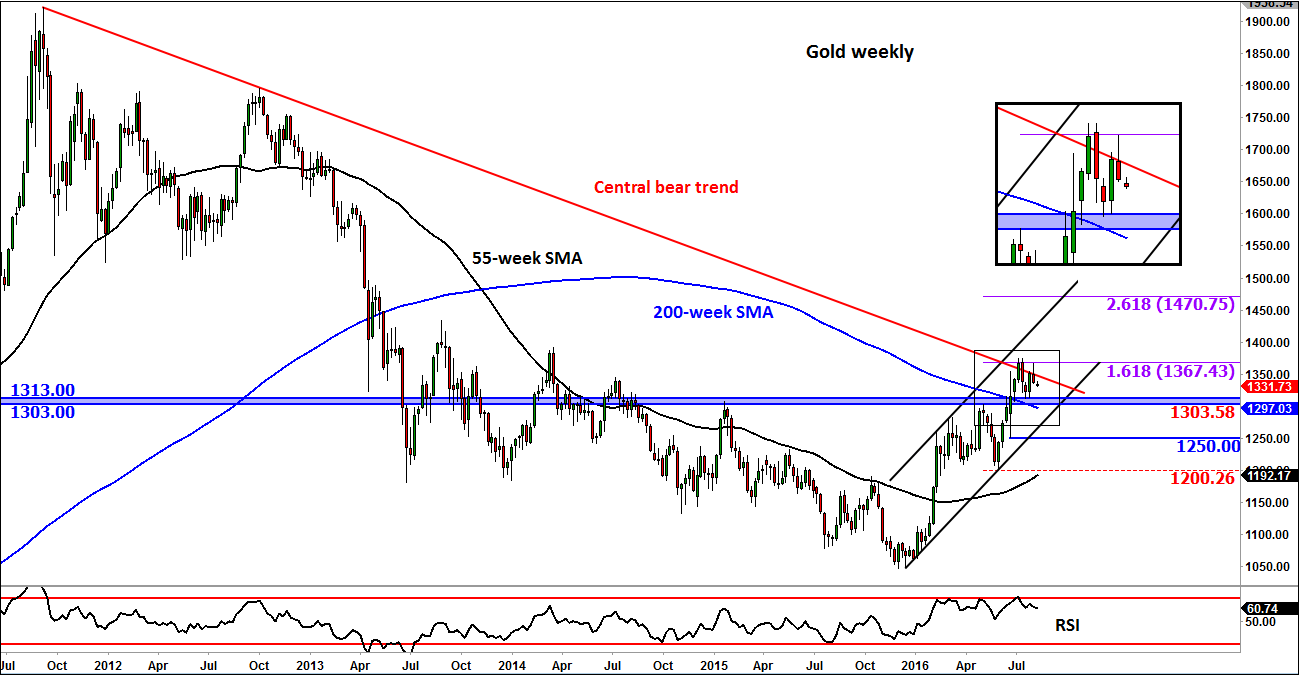

Meanwhile from a technical point of view, gold’s repeated failure to break conclusively above its central bearish trend line that has been in place since September 2011 is also very significant. The precious metal continues to run into offers around $1367, a level which marks the 161.8% Fibonacci extension level of the previous corrective swing. What’s more, the momentum indicator RSI is now trending lower on the weekly time frame after it had climbed to the “overbought” threshold of 70 and higher a few weeks ago.

Put another way, gold has reached an exhaustion point around a long-term key resistance area. So, in theory, then, gold may start to head lower now. If this view is correct, traders should anticipate support levels to break down, potentially leading to further sharp down moves over time. But if this hypothesis is not correct, then we should see some false breakdown scenarios, which could provide decent buying opportunities. Whatever is the case, traders may wish to observe price action closely in the coming days. They should let price dictate direction and then trade in the direction of the near-term trend, which we think is going to be bearish. But in the very short-term outlook, expect to see some oversold bounces too as the trend has not yet turned bearish.