Gold tests key level head of US jobs report

Since the outcome of the Brexit vote two weeks ago today, the dollar has risen sharply against both the euro and more noticeably the pound; […]

Since the outcome of the Brexit vote two weeks ago today, the dollar has risen sharply against both the euro and more noticeably the pound; […]

Since the outcome of the Brexit vote two weeks ago today, the dollar has risen sharply against both the euro and more noticeably the pound; government bonds have repeatedly rallied to new highs – that’s to say their yields have fallen to record low levels, while the equity markets have been all over the place. Amidst all this confusion and uncertainty, investors have flocked to traditional safe-haven assets: precious metals. Gold and especially silver have seen their prices rise relentlessly for the best part of two weeks. The appetite for gold and silver has not only been reflected in their rising prices, but also by a surge in net long positions, strong ETF inflows and higher coin sales in the US. At the same time, outflows have risen sharply from European equity funds and investor sentiment indices have tumbled, confirming the flight to quality. But with the passage of time – barring any further economic shocks – sentiment is likely to start improving again. Meanwhile the record low and falling yields means investors will continue to find the higher-yielding equity markets more appealing, while the dollar could further extend its gains as a result of a sudden improvement in US data, which could raise interest rate hike expectations once again. So while gold and silver look strong now, there is scope for significant profit-taking in both.

Today’s focus is fixated on the US monthly jobs data with earlier indications this week suggesting it will be a strong report. A headline non-farm payrolls reading of 175,000 is expected with the average hourly earnings index seen rising 0.2% month-over-month. If the actual numbers turn out to be much stronger than expected, the US dollar could jump and precious metals slump; the opposite is also true. Looking beyond the NFP report, the economic calendar will be populated with plenty of data from mid next week. We will have the latest Chinese trade figures on Wednesday, followed by their GDP and industrial production figures on Friday. If these numbers turn out to be weak, sentiment could turn sour once again, further boosting the appeal for safe haven assets. Also on Friday, we will have some important data from the world’s largest economy, the US: CPI, retail sales and consumer sentiment should provide plenty of direction for the dollar and in turn buck-denominated precious metals.

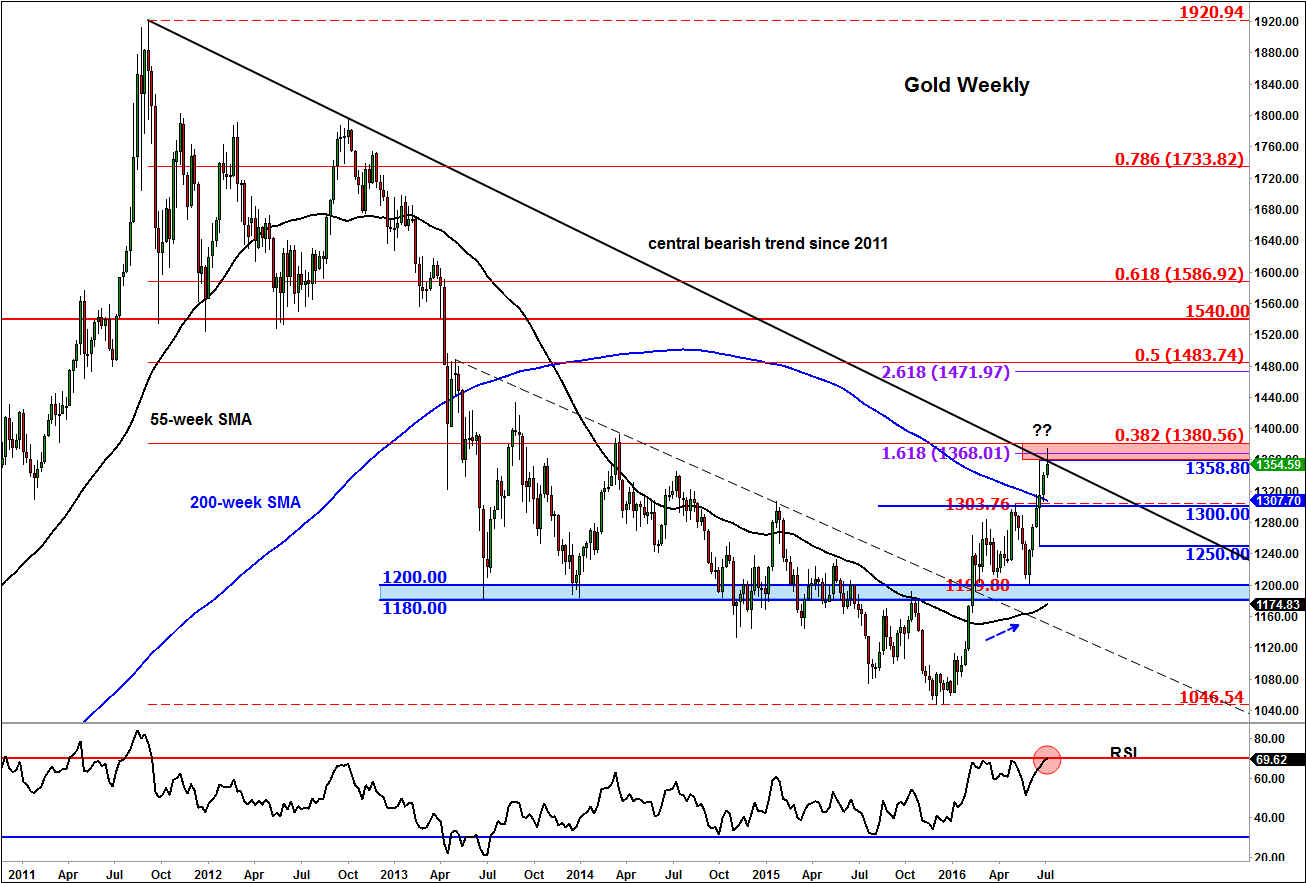

Technical outlook: scope for some profit-taking?

After climbing for five consecutive weeks, the yellow precious metal has now reached a potentially strong resistance area around $1358-$1380. As can be seen from the weekly chart, below, this is where the central bearish trend line that had been place since the year 2011 meets a couple of Fibonacci levels: the 38.2% retracement against that 2011 all-time high and the 161.8% extension of the most recent downswing. Unsurprisingly, the momentum indicator RSI has reached the “overbought” threshold of 70 on the weekly and daily time frames.

Given the above technical considerations, a pullback of some sort would not come as a surprise to me whatsoever. In fact, this could be a healthy outcome as far as the bullish argument is concerned as it will allow the oscillators to unwind from overbought levels, providing opportunity for new buyers to step in at better levels. That being said, investors may not find any real reason to take profit. So watch price action closely. If prices consolidate near the highs and the RSI unwinds through time rather than price action then this would point to further sharp gains. The potential levels of support that will need to hold are shown on the chart in blue, the most important one in my view being $1300 (the meeting of old support with the 200-week moving average).