Gold refusal to shine in risk off environment is bearish

In days like today gold is meant to shine, some would argue. After all, risk is definitely off the menu with the global equity markets […]

In days like today gold is meant to shine, some would argue. After all, risk is definitely off the menu with the global equity markets […]

In days like today gold is meant to shine, some would argue. After all, risk is definitely off the menu with the global equity markets falling viciously across the board. Germany’s DAX index for example has just closed almost 4 per cent lower, with carmakers bearing the brunt of the sell-off after Volkswagen admitted using software to rig emissions tests. Concerns over the health of the global economy have also come to the forefront of investors’ minds after the Asian Development Bank and the Chinese Academy of Social Sciences both lowered their estimates for economic growth in China. Consequently, oil and especially copper prices have dropped sharply on demand concerns, causing more pain for commodity stocks. Indeed, Glencore momentarily traded below £1 a share for the first time ever in London earlier today.

So, given this risk off environment, why is gold not able to affirm its position as the ultimate safe haven asset? In my view there are several reasons why this is the case which includes the physical supply and demand dynamics, but ultimately it boils down to the appreciating US dollar in what essentially is a deflationary environment. The greenback has stormed back to life this week after initially falling in response to what was a rather dovish FOMC statement and press conference from the Federal Reserve last week. However, several Fed policymakers have since spoken and expressed optimism about the health of the US economy. In addition, some have tried to distance themselves from being paranoid about the equity market volatility, with Bullard for example rightly arguing that the Fed cannot permanently raise stock prices. Thus, traders are betting that a 2015 rate increase is after all still on the cards and may happen either at the Fed’s October or December meetings. Consequently, the dollar is rallying and this is helping to keep the buck-denominated precious metal under some pressure.

Meanwhile, with price pressures being almost non-existent at the moment, due in part to the weaker oil prices, investors would argue that at this stage there is no urgency to buy gold for hedging purposes against inflation. The metal costs money to store and unlike stocks or bonds, it does not pay dividends or interest. Gold is also held back by a weaker price of silver, which has dual usages as a precious metal and industrial commodity. With concerns over China being at the forefront, investors are concerned that demand for silver to be used in manufacturing could fall.

Clearly, investors are making better use of their trading capital in markets which are trending. In fact, gold is also trending, but in a downward direction. Thus speculative trend followers are still doing what they have been doing for the past several years: selling into the rallies. This strategy has evidently been successful and they will therefore milk it for as long as possible and until proven wrong.

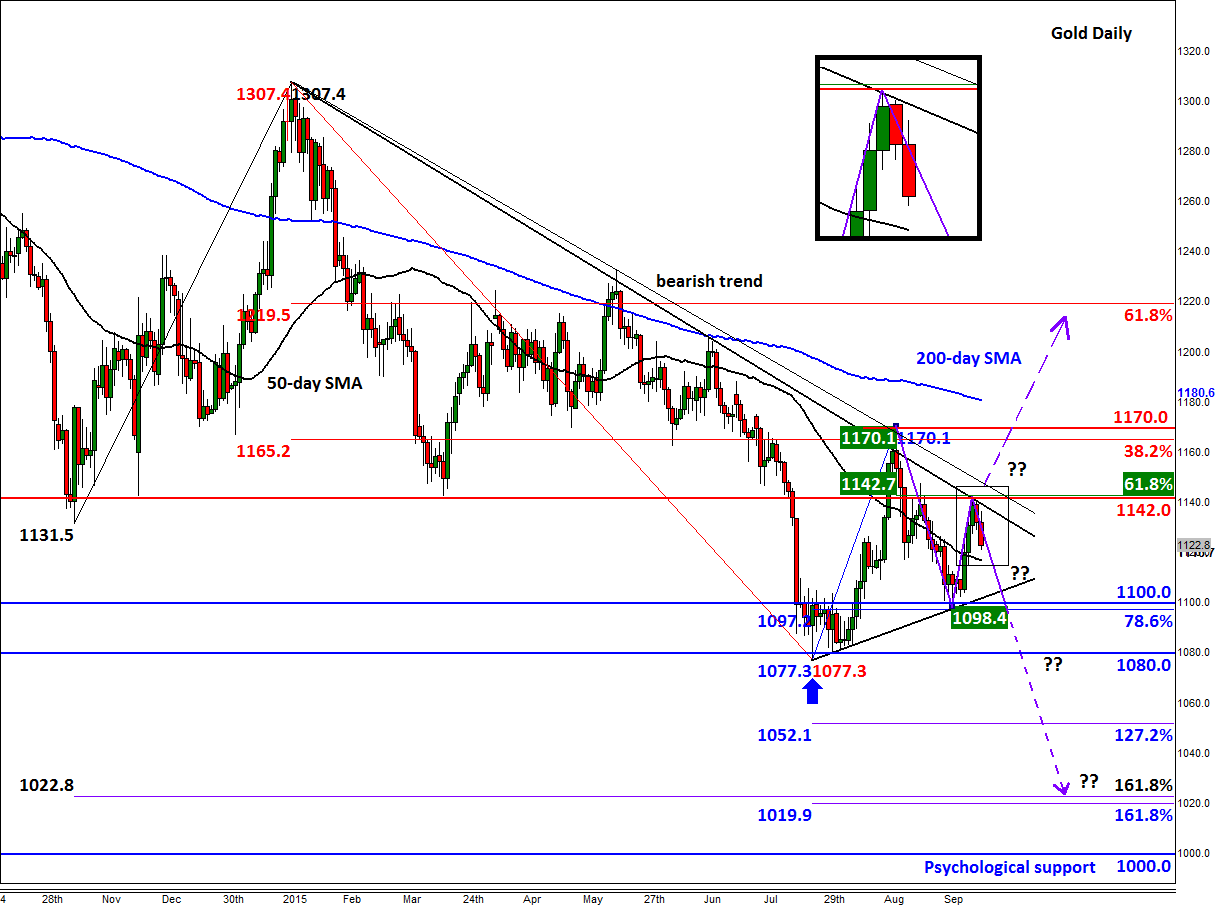

Gold bears will be proven wrong when some key resistance levels start to break down. At the moment, no such level has been taken out with gold failing to crack the support-turned-resistance and 61.8% Fibonacci retracement of its most recent downswing, at $1142/3 this week. In addition, the bearish trend line that goes back to the start of this year has remained intact while both the 50 and 200 day moving averages are pointing lower. Therefore the trend is clearly still bearish and there is a good chance it will remain that way for the foreseeable future given the still-weak fundamental drivers of gold. The lack of apparent safe haven buying today is also a sign for concern; if the metal fails to rally on days like today then imagine what it might do if and when the equity markets rally. This makes us maintain our bearish view on the metal. As such we view the prospects of a break below the short-term bullish trend line as a higher probability outcome as opposed to a break to the upside. If this happens, gold may then go on to break below the next key support at $1100 and potentially revisit – or indeed even break – the August low of $1077.

All that being said however, if the metal somehow manages to find strong support and rallies above the bearish trend line then we will be quick to drop our near-term bearish bias. Indeed, as technical analysts and traders, we should ideally let price action determine the direction and then trade in that direction.