Gold bears still in control as FOMC week finally arrives

After rallying strongly at the start of August, gold has now fallen for the third straight week and has relinquished three quarters of those gains […]

After rallying strongly at the start of August, gold has now fallen for the third straight week and has relinquished three quarters of those gains […]

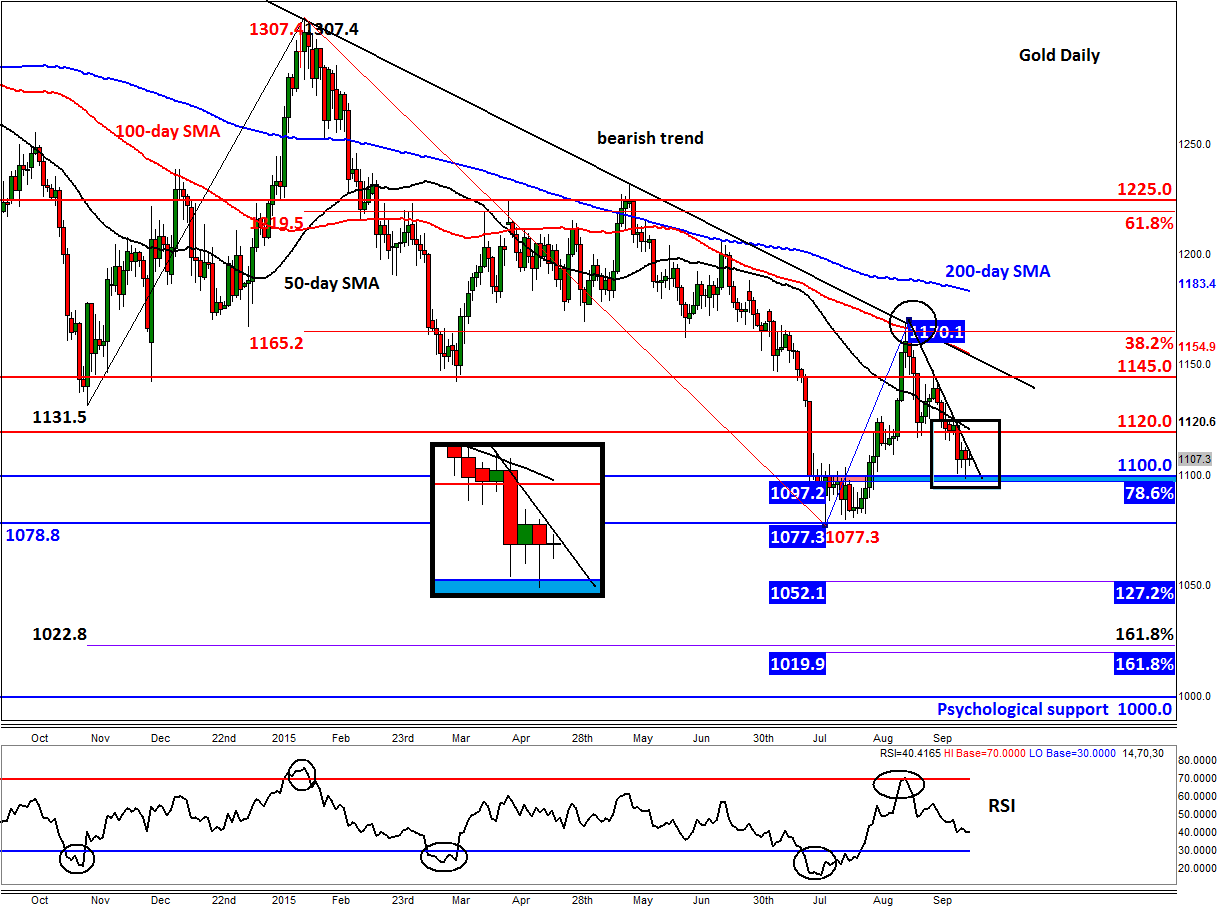

After rallying strongly at the start of August, gold has now fallen for the third straight week and has relinquished three quarters of those gains already. The precious metal has dropped even despite a weaker dollar last week and increased volatility across the stock markets. This does not bode well for the metal, particularly if the bulls also lose control of the technically-important level of $1100 on a closing basis. At the timing of this writing though, the precious metal is holding its own above this level in what so far has proved to be a quiet trading session.

Though it may all be about the Fed this week, we’ve already seen some important data from China at the weekend and more global macroeconomic pointers will be released over the next several days that could spur some volatility ahead of Thursday’s much-anticipated FOMC meeting. But as far as gold is concerned, only the US numbers will probably matter due to the metal being priced in the dollar. In this regard, US retail sales and industrial production data on Tuesday, and CPI on Wednesday, will be among the more important releases ahead of the FOMC statement and press conference on Thursday.

As far as the Federal Reserve is concerned, if the central bank sends out a dovish signal on Thursday, this may help to boost stocks and undermine the dollar. Gold may benefit as lower rates for longer would decrease the relative opportunity cost for holding the metal. However, the likely “risk-on” trade may mean that investors will pay less attention to gold and allocate more of their trading capital into equities. Nevertheless, the precious metal could rise a little in the short-term, under this scenario. However, if the Fed decides to send out a more hawkish message, including a rate increase, this may help unpin the dollar and undermine both stocks and buck-denominated gold. Thus in both scenarios, the upside appears to be limited for gold – unless of course we see massive drops in both equities and the dollar later in the week.

Meanwhile From a technical point of view, gold’s next key support level is, as mentioned, around $1100, a level which was formerly resistance and held firm upon the first test on Friday. This level also roughly corresponds with the 78.6% Fibonacci retracement ($1978) of the most recent corrective upswing. Given that several other such “key” support levels have been broken in the past, it appears as though another breakdown here is the more likely outcome as opposed to, say, a rally above resistance and the 50-day moving average at $1120. If the bears win the battle here, the shiny metal may then drop to test the 5.5-year-low low of $1077 that was hit in July, ahead of potentially further falls towards the Fibonacci extension levels shown on the chart.

Therefore, as things stand, the path of least resistance continues to remain to the downside. But things could change dramatically given for example the sheer number of high-impact economic events this week. In terms of trade management, the bears will need to proceed with a higher degree of caution at this stage – particularly if we see a decisive break of the above-mentioned resistance around $1120. If that happens, technical momentum buying could easily see gold rise to the next level of resistance at $1145, before deciding on its next move.