Glencore shares out of a hole though credit concern lingers

The latest Glencore twist saw the shares roaring as much as 20% higher, at the start of Monday trading, after buyers of its Hong Kong […]

The latest Glencore twist saw the shares roaring as much as 20% higher, at the start of Monday trading, after buyers of its Hong Kong […]

The latest Glencore twist saw the shares roaring as much as 20% higher, at the start of Monday trading, after buyers of its Hong Kong stock struck even harder, sending it surging 70% ahead.

Much like the stock’s collapse in the opposite direction a week ago to the day, ‘explanations’ for the thunderous reveille on Monday were not entirely convincing.

Once again, Glencore itself pleaded ignorance early on.

“The Board confirms that it is not aware of any reasons for these price and volume movements or of any information which must be announced to avoid a false market in the Company’s securities” the company said via the HKSE.

The ostensible reasons for resurgent good sentiment included reports that the heavily indebted miner was discussing the sale of a stake in its agricultural assets to a number of institutional investors.

Saudi Arabian sovereign wealth fund SALIC and China’s state-backed grain trader COFCO were mentioned, together with Canadian pension funds, but there has been no official corroboration.

Further asset disposals has emerged as the most likely means by which the group can reduce its worst-among-peers leverage (c. $30bn net debt) and stave off risk of a credit rating downgrade that would make its financing costs even more punishing.

Glencore CDS spreads continued to shrink from ‘credit event’ risk levels on Monday.

The 5-year paper was trading at 631.488 basis points (bp), down 97.926bp and now well off an Investec-fuelled peak of 825bp.

Glencore share buying by august insiders like Tony Hayward, former CEO of BP, now Glencore’s chairman, and board member John Mack, erstwhile high-profile chief of Morgan Stanley, has also done the stock no harm.

The remarkable recovery of sentiment on the embattled miner’s equity has now returned the stock back to late-September prices, though that’s still about 80% below its IPO price.

Support from bulge-bracket Wall Street banks in concert with influential shareholder buys has put the other end of the argument about Glencore more firmly into the public domain.

This more bullish view is hinged on the fact that GLEN has ready access to credit and aims to reduce debt by about a third in the near term, perhaps backed by aforementioned assets sales and others.

The one thing Glencore has studiously avoided offering during its fight back is a categorical breakdown of its short-term credit profile.

An estimated $18bn in short-term credit that Glencore’s trading arm is on the hook for has arguably been at the crux of concerns over its debt.

Whilst Glencore’s affirmation that it remained “operationally and financially robust”, and that it had “positive cash flow, good liquidity and absolutely no solvency issues,” fired the starting gun on the shares’ recovery, doubts linger in absence of definitive clarification.

Monday news that Glencore’s borrowings include $24bn in syndicated loans backs the impression that its defenders have been somewhat selective.

Syndicated loans are an area that has hitherto received lower attention from investors than other types of leverage.

Brokerage research out on Monday suggested there is roughly $125B in total debt on issue to the top seven commodity traders and another $120B-$150B in bank letters of credit.

In the absence of a direct statement from Glencore about credit arrangements for its trading arm, upside surges in Glencore shares of the kind seen this morning could soon get rarer.

The London-listed stock is now more than 70% above the lows it saw a week ago.

That being said, this company and its stock have confounded expectations for several days.

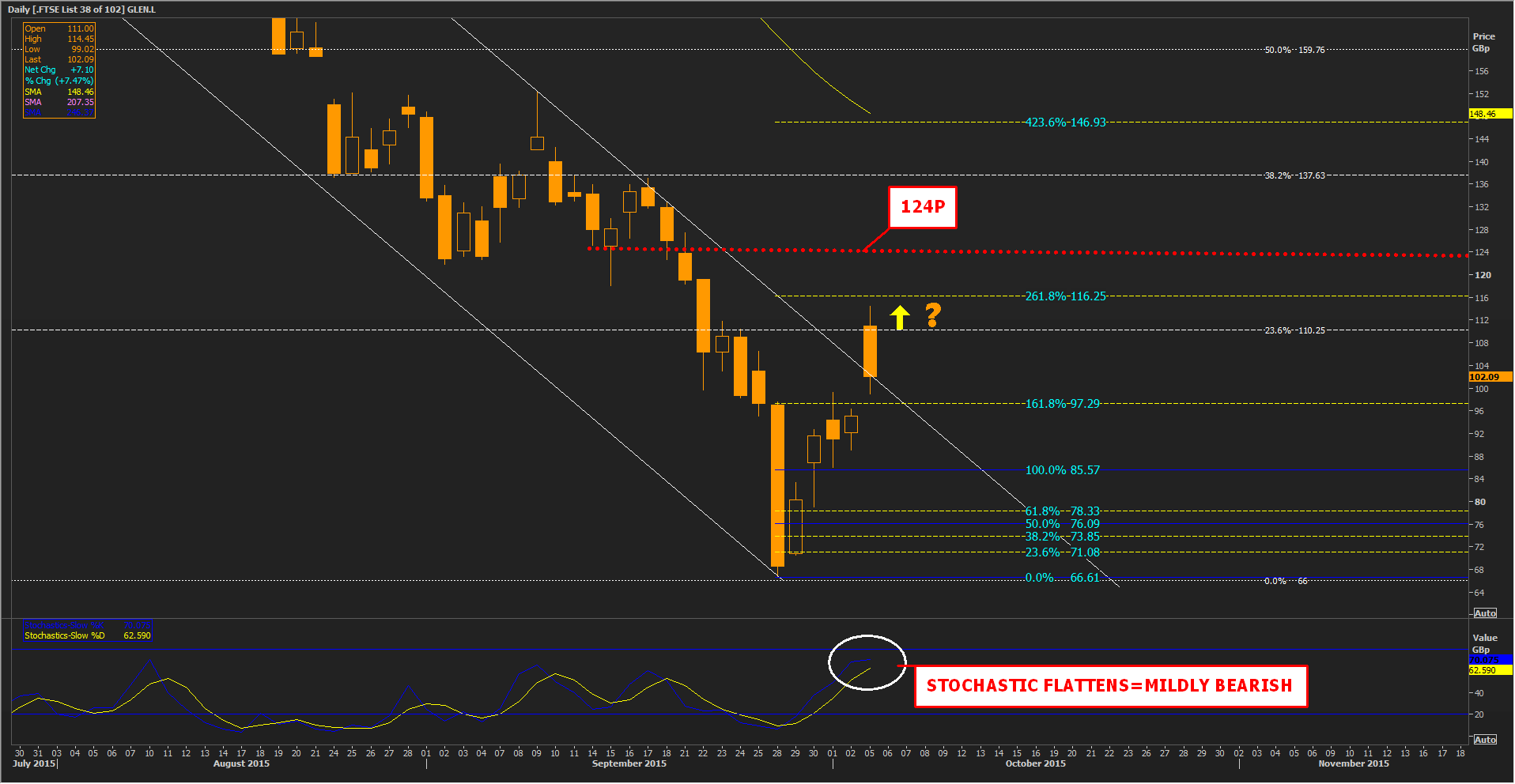

Potential overhead challenges like an important Fibonacci (261.8%/116.25p) and a weak former support, now resistance (124p) probably have less weight.

Upside momentum is slackening (see Slow Stochastic sub-chart) but is not technically overbought.

Please click image to enlarge