Glencore shares could dig deeper

UK-listed mining giants have borne the brunt of China’s determined yuan devaluation campaign this week, but Glencore, the commodity trader-to-base metals producer, was one of […]

UK-listed mining giants have borne the brunt of China’s determined yuan devaluation campaign this week, but Glencore, the commodity trader-to-base metals producer, was one of […]

UK-listed mining giants have borne the brunt of China’s determined yuan devaluation campaign this week, but Glencore, the commodity trader-to-base metals producer, was one of the worst hit, including on Friday.

It topped its weekly loss with an additional 2.2% fall, placing it close to the bottom of the FTSE 250 Mining Index.

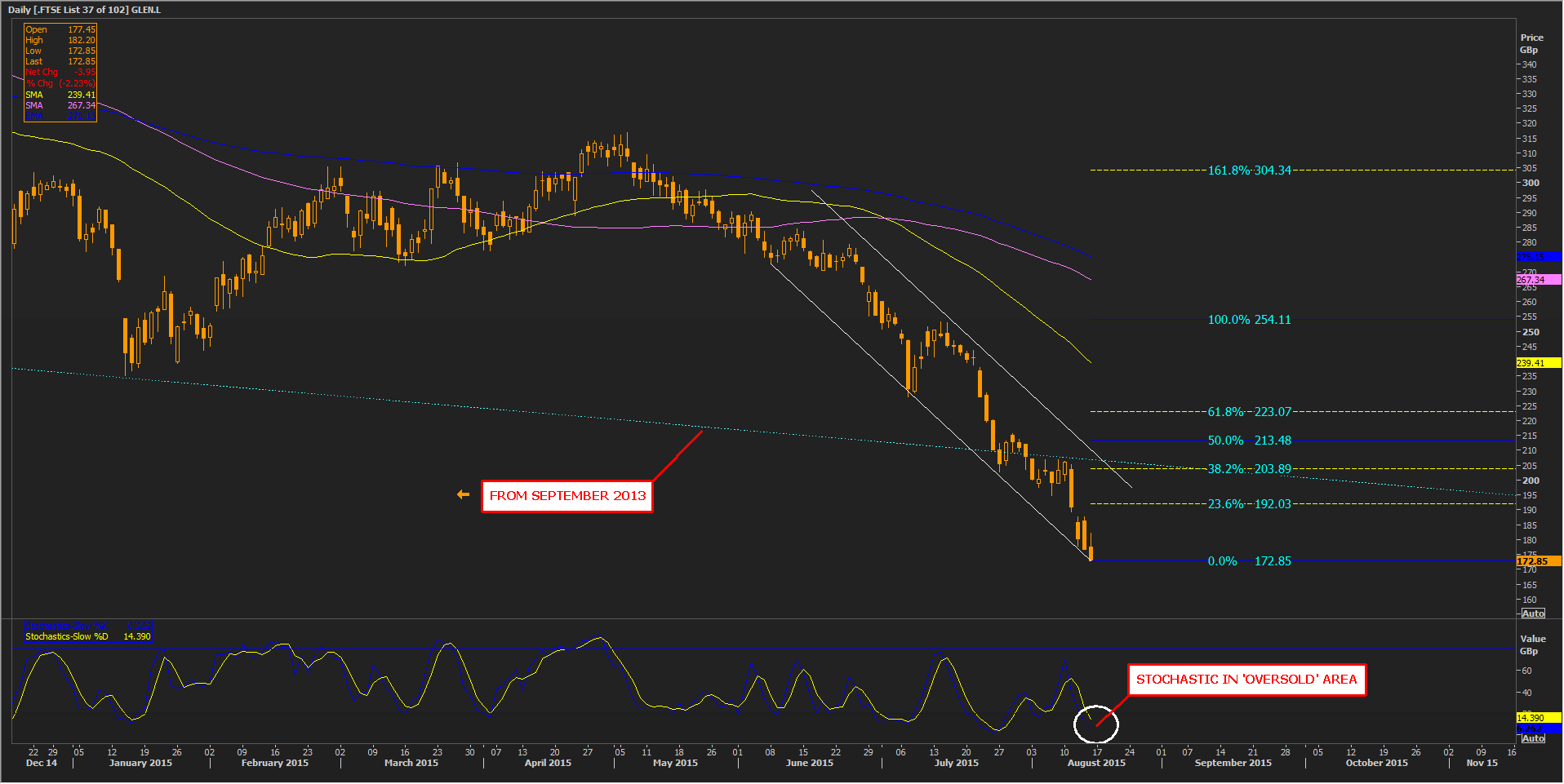

It also etched a new all-time low at 172.85p, its 10th since breaking below a long-term trend earlier this month.

Glencore’s full first-half earnings will be released on Wednesday 19th August.

But after it this week announced write-offs, forced asset sales, industrial capex cuts and production falls, already pessimistic market forecasts might even need to be revised lower still.

| H1 Jun-2015 FORECASTS: | EPS | Revenue | ||

| $0.07 | $88bn | |||

| Mean % Change | -6.67% | 8.99% | ||

Data from Thomson Reuters

An additional weight for the Swiss-domiciled conglomerate with a corporate structure that is complex and byzantine even by the standards of multinational resource firms has been the fallout from its attempts to slash spending and sell assets.

On Thursday, Glencore said it would reduce its capex plans for production of copper and nickel, which trade near six-year lows, amid a supply glut and slowing Chinese demand.

The company said it had sold its interests in a copper mine in the Philippines, and nickel mines in the Dominican Republic and Ivory Coast.

Glencore received just $290m for all three of these assets, no doubt at a steep discount to their value when inherited as part of the takeover of Xstrata Plc. in 2013.

It also said it would ‘impair the value’ of (essentially write-off) operations in Chad, Central Africa by $790m.

So, in terms of its growth outlook, even among the largest FTSE 100 base metals miners, where there are few pictures of health, Glencore may be uniquely challenged.

And, it’s arguable that at least part of its steep discount to peers on a number metrics, hinges on its status as an ‘impure’ mining play.

Uncertainty might be the main reason for implied avoidance by investors (see Price/Free cash flow; Price/Book Value per Share and EV/Sales forecasts below).

| Company | Price / EPS | EV/EBITDA, NTM | Price / Free Cash Flow Per Share | Free Cash Flow Per Share Yield % | Dividend Yield, NTM | EV/Sales, NTM | Price To Book Value Per Share |

| Anglo American PLC | 12.85 | 5.20 | -3.1% | 6.2% | 1.20 | 0.76 | |

| BHP Billiton PLC | 12.62 | 7.48 | 16.23 | 6.2% | 7.1% | 3.34 | 1.20 |

| Glencore PLC | 17.69 | 7.07 | 6.93 | 14.4% | 6.5% | 0.42 | 0.74 |

| vs. PEER MEAN | +32.8% | +10.5% | -57.8% | +11.4% | +0.2% | -81.4% | -38.6% |

| Rio Tinto PLC | 14.51 | 6.49 | 16.60 | 6.0% | 5.9% | 2.22 | 1.64 |

Data from Thomson Reuters; all forecasts for next fiscal year except ‘NTM’ – Next Twelve Months

If, as investment bank Goldman Sachs said this week metals “demand has low sensitivity to yuan denominated prices and hence depreciation likely has limited effects”, then optimism about eventual medium-term benefits for miners from China’s devaluation might be misplaced.

That should move the emphasis for investors in multinational miners firmly back on their ‘self-help’ abilities.

These will of course vary, depending on those perceived to be strongest and weakest.

From a technical perspective, investors are likely to show only minimal reaction to Glencore’s H1 disclosure on Wednesday, if as suspected, the most important news in its results has already been revealed.

But since Glencore shares having broken down through the specific trend that commenced in September 2013, further all-time lows could be seen, although the stock is currently ‘oversold’ according to its Slow Stochastic indicator.

Rebounds in the medium term look set to be limited by the descending trend mentioned above, especially because it coalesces closely with an important projection (38.2%) from all-time lows.

Please click image to enlarge