German car shares may drive DAX to new 2015 lows

The firmer footing found by Germany’s benchmark DAX30 index, a day before, was difficult to maintain on Thursday. Partly fuelled by a near-40% collapse in Volkswagen […]

The firmer footing found by Germany’s benchmark DAX30 index, a day before, was difficult to maintain on Thursday. Partly fuelled by a near-40% collapse in Volkswagen […]

The firmer footing found by Germany’s benchmark DAX30 index, a day before, was difficult to maintain on Thursday.

Partly fuelled by a near-40% collapse in Volkswagen shares amid a widening scandal over falsified emissions, the DAX has slumped to September lows, again approaching its weakest levels since mid-December 2014.

VW has become the whipping boy for many European stock market ills over the last few days but it could be joined by others.

Even as investors struggled to get a handle on the extent of VW’s deception of US regulators and how sharp its consequent penalties there would be, setting limits on the broader issue of car makers’ emissions compliance has been even trickier.

Europe’s most powerful executive body, the European Commission, signalled on Thursday the strong likelihood of a widened probe into how many carmakers might have used illegal “defeat” devices to cheat emissions tests.

It was the clearest indication yet that European regulators suspected VW’s admission of its own pollution emissions could be a ‘smoking gun’ for the rest of the industry.

For German investors, this immediately put its other two iconic automobile giants with heavyweight DAX listings, BMW and Daimler, in the frame.

Whilst BMW and Daimler moved swiftly to distance themselves from emissions cheating, this has not prevented both of their respective stocks from falling by 13%-15% since Friday last week, when the VW scandal hit the headlines.

A spokesman for Daimler said on Thursday the maker of Mercedes-Benz cars did not use so-called ‘defeat devices’ employed by Volkswagen and complied with rules on nitrogen oxide emissions around the world.

And a spokesman for Bavaria’s most famous corporate resident was quoted in Germany’s Bild magazine as saying: “There is no function in BMWs for recognising exhaust cycles, and all exhaust systems remain active outside of exhaust cycles.”

In other words, BMW was stating that its cars produce the same emissions whether they are being tested for pollution, or not; unlike Volkswagen’s.

Either way, investors were reserving judgement at the time of writing.

Daimler shares were down 5% and BMW’s were losing 6.7%.

The immediate worry for market watchers is that the German auto sector’s 35% earnings contribution and c. 25% market cap weighting in the DAX could destroy any hope of recovery from recent global growth worries that battered the market in recent weeks.

Calculations using consensus forecast data from Thomson Reuters suggest the DAX’s aggregate EPS forecast might have to be trimmed by as much as 5% for this year and perhaps about 6% in 2016.

And, with Germany being the largest and the strongest economy, by many measures, in the Eurozone, it’s more than conceivable that earnings impact in Germany could be transferred to other regions in the bloc, re-establishing the negative feedback loop between Europe’s weakest and strongest regions.

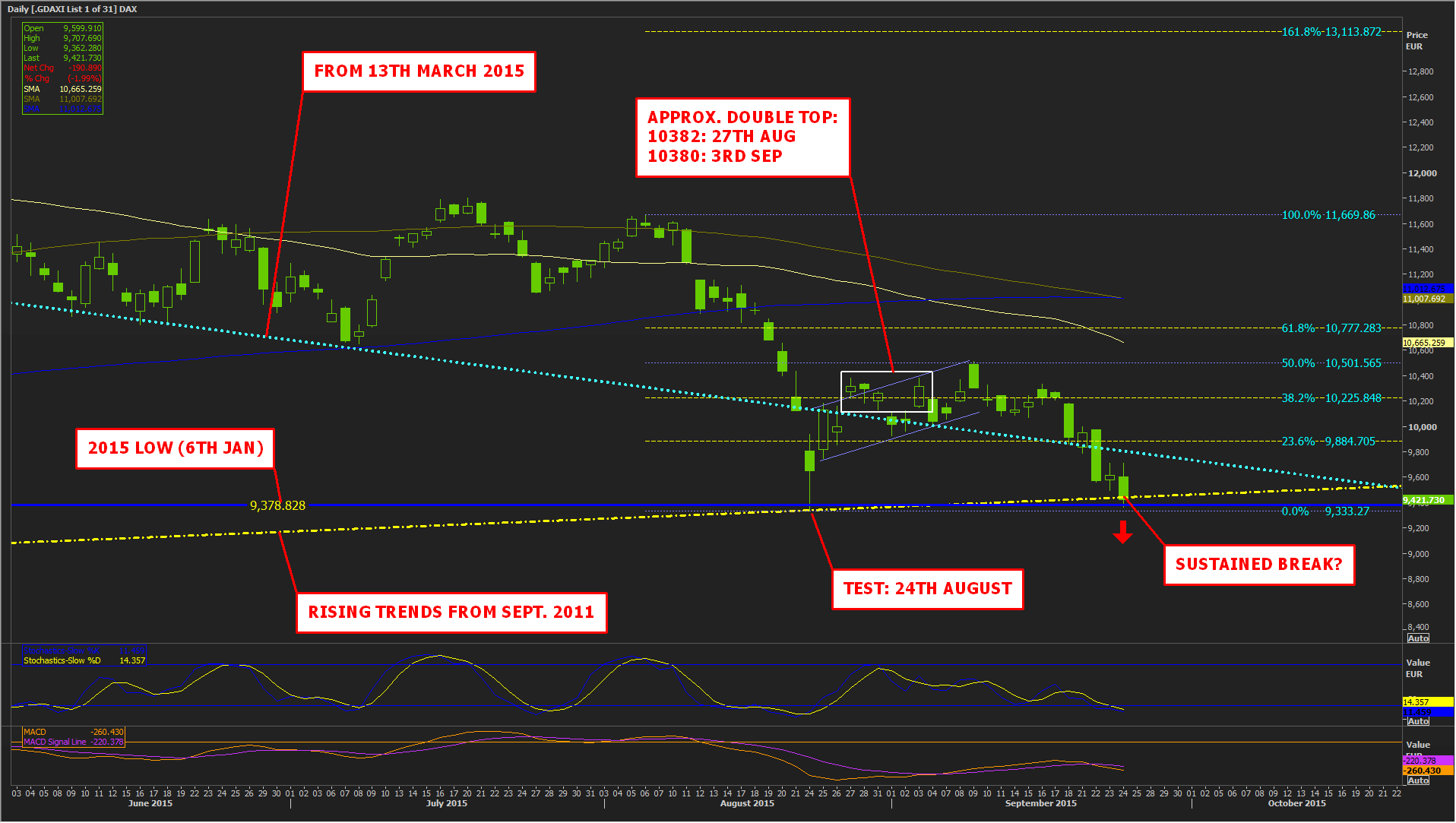

As these fears preyed on DAX investors earlier in the week, they drove the index through a closely eyed descending trend line that had limited the severity of its bear trend since March 2015.

Please click image to enlarge

With the help of Volkswagen’s eventual dismissal of its embattled CEO Martin Winterkorn, on Wednesday, German shares had recovered, giving hope that selling had reached a floor.

The DAX was right on the brink of an arguably even more important trend, a line that went back to Europe’s sovereign debt crisis in 2011.

This had convincingly supported the market during the China-fuelled turmoil of late August.

But Thursday’s sell-off finally pushed the index through it.

The DAX has been left once again, eye-to-eye with 2015 lows—just 60 points away at the time of writing.

The trouble is, the German market is now in an even tighter spot than it was at the end of last week.

It’s now difficult to find convincing further support nearby for the DAX, should it break both its last remaining long-term trend, and the year’s nadir around 9378.

That, in theory would pave the way to further declines even beyond DAX’s c.25% loss since highs for the year in April.

I scratch my head to find meaningful levels that could break the market’s fall if its 2015 low breaks.

We have to move to a longer-term chart before potentially firmer ground becomes visible.

As we have noted, relatively weak support was seen before (on 9th January) about 50 points from DAX’s ‘cash market’ settlement on Thursday at 9427.

However the index dug its heels in more convincingly between January 7th and January 21st.

It bounced off lows between 9148-9170 during those three weeks.

That’s about 260-to-280 points away from the DAX cash settlement on Thursday.

In the event of that band also failing, investors might have to begin pinning hopes on the index’s 200-week moving average, 7% away at 8733.

Please click image to enlarge