Investors have turned cautious overnight as geopolitical tension in Asia, combined with fears of a second coronavirus flare up in China are weighing on risk sentiment, overshadowing hopes of a cheap covid-19 life saving drug. Asian markets moved lower, European bourses are pointing to a move southward on the open, meanwhile safe havens such as the US Dollar and gold are trading mildly higher.

China now has 130 reported new cases in Beijing and is struggling to contain the spread of the virus, without sealing off its most important city. Schools have been close and flights cancelled. South Korea has also reported 43 new cases in 24 hours, in the US Florida’s infections reached a new high and Texas has seen hospitalisations surge.

Fears of a second wave could weigh heavily on confidence. As Powell warned a full US economic recovery will not occur until Americans are sure that covid-19 has been bought under control. That goes not just for the US but across the globe.

Market confidence is being challenged, even after US retail sales obliterated expectations on Tuesday, boosting hopes that a quick recovery from the coronavirus crisis was still possible. However, Federal Reserve Powell warned that output and employment would remain short of pre-pandemic levels for a long time.

Drug Breakthrough

News of a major breakthrough in the fight against coronavirus has failed to bring in a strong reaction in the market. A low dose, cheap steroid dexamethasone can hep save lives for those patients on ventilators. This is a positive step forward,which is helping to underpin sentiment.

News of a major breakthrough in the fight against coronavirus has failed to bring in a strong reaction in the market. A low dose, cheap steroid dexamethasone can hep save lives for those patients on ventilators. This is a positive step forward,which is helping to underpin sentiment.

Trade Deal Optimism

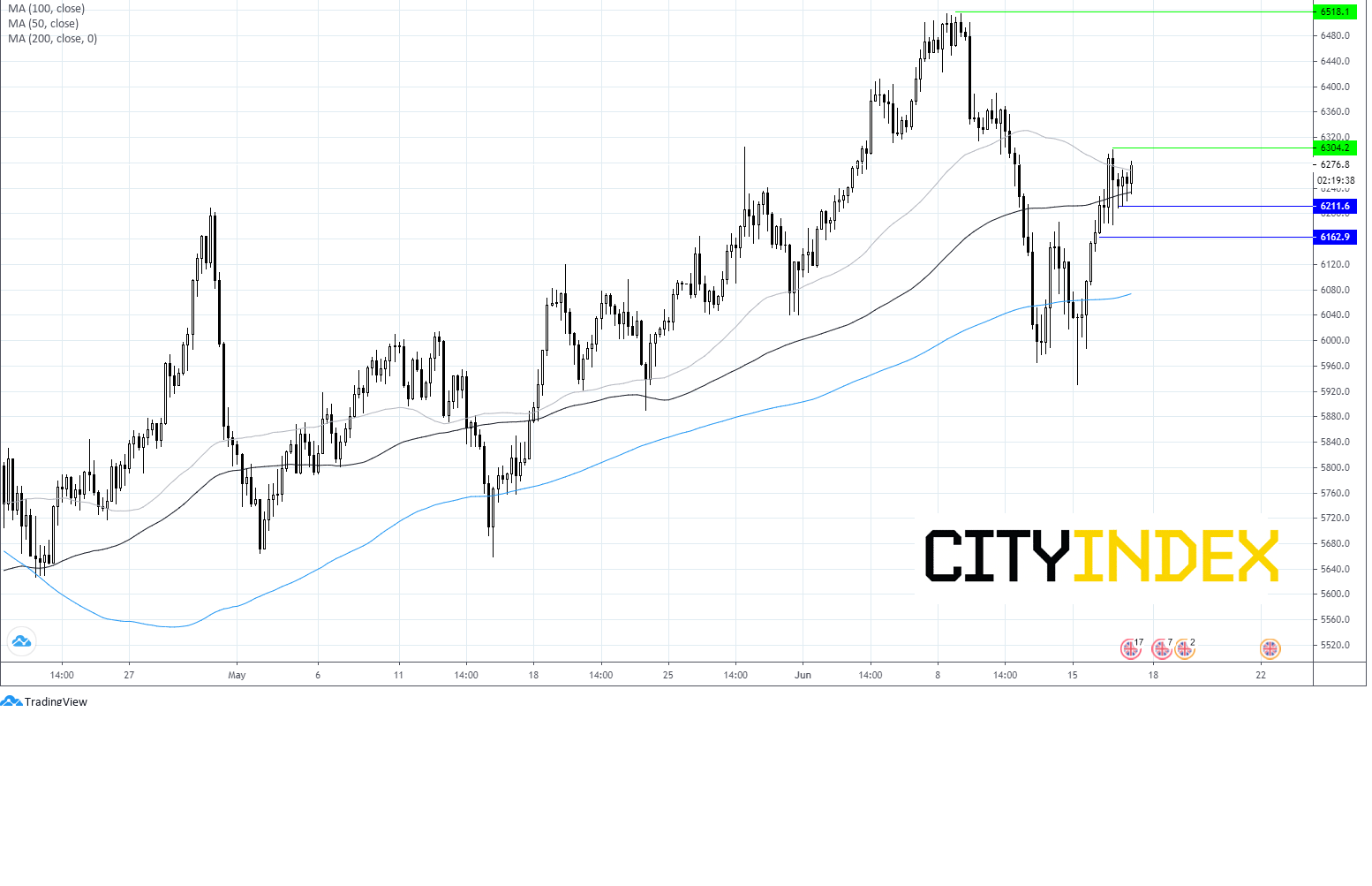

In the UK, the FTSE looks set to fare marginally better than its European peers. Hopes that Boris Johnson could scarp the two-meter rule soon, in addition to optimism surrounding trade deals with Australia and New Zealand are helping to underpin sentiment.

In the UK, the FTSE looks set to fare marginally better than its European peers. Hopes that Boris Johnson could scarp the two-meter rule soon, in addition to optimism surrounding trade deals with Australia and New Zealand are helping to underpin sentiment.

GBP Gains As Inflation +0.5% yoy in May

The Pound has unexpectedly spiked into positive territory versus the USD following the release of some pretty grim inflation data. Consumer prices were flat month on moth in May, however, on an annual basis inflation increased a lacklustre 0.5%, down from 0.8% but in line with expectation. In a classic glass half full approach, the Pound is taking solace from the fact that inflation wasn’t worse than forecast.

This reading is unlikely to prompt the Bank of England to cut rates when it gives its rate announcement tomorrow. An additional £100 billion in QE is already priced in.

Latest market news

Yesterday 11:48 PM

Yesterday 11:16 PM

Yesterday 05:00 PM

Yesterday 01:13 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM