US CPI Disappoints

Even though the US – Sino trade dispute is occupying centre stage on Friday, US inflation data still managed to grab trader’s attention, but for all the wrong reasons. CPI data showed that inflation in the US increased 0.3% month on month in April, down from 0.4% in March and missing expectations of 0.4%. The dollar extended losses even though inflation on an annual basis ticked higher to the Fed’s target level of 2%, it was also short of forecasts. Today’s CPI combined with yesterday’s slightly weak PPI figures will not encourage the Fed to take its finger off the pause button.

UK GDP - In line with expectations

Sterling took advantage of the weaker dollar moving northwards after investors had barely reacted to earlier UK GDP data. Thee were no real surprises from the GDP print, with Q1 growth at 1.8% yoy as forecast. Pound traders initially shrugged off the “as expected” data only pushing higher after the weaker US VPI print.

Whilst the headline figure suggests that the UK economy is showing resilience amid lingering Brexit uncertainties, the reality is not quite so rosy. The UK economy performed ok in the first quarter, however than was mainly thanks to stockpiling ahead of the March Brexit deadline. The production and stockpiling of unsold goods is obviously is neither sustainable or commendable as a way of boosting economic growth.

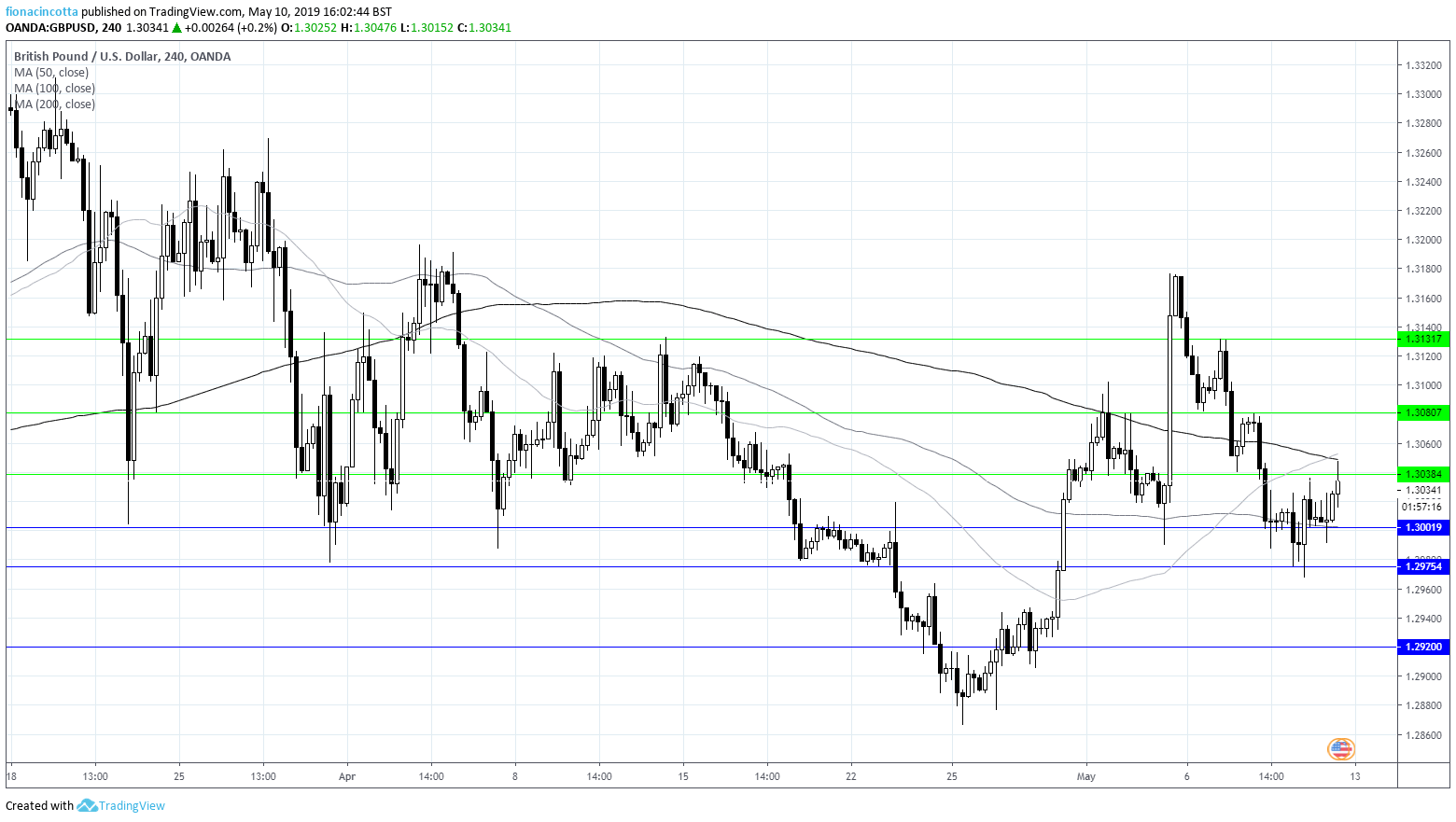

GBP/USD to break above $1.3050?

Following the UK GDP & US CPI, GBP/USD is trading 0.2% higher, with immediate support at $1.30, ahead of support at $1.2975 and $1.2920. On the upside a break through resistance of $1.3053 (50 SMA), could open the door to $1.3080 before $1.3130.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM