GBP/USD has advanced in early trade following the release of GDP data. Whilst on an annual and monthly basis economic growth beat expectations, on the more closely watched quarter on quarter basis the economy failed to grow. There was no surprise here.

Consumer spending was weak whilst business investment fell by 1%. But this is old news. The BoE had factored in 0% growth in Q4. This data is not going to make a rate cut by the BoE any more likely.

December’s hard data was also uninspiring, with manufacturing production missing estimates on both a monthly and yearly basis and with downbeat industrial production. Construction numbers were a rare source of light unexpectedly increasing 0.4% month on month vs a 0.4% decline forecast.

Better data to come?

Yet the disappointing hard data prints could change over the coming months, as we have seen in recent survey’s, optimism has improved considerably following December’s general election. The big question is whether the improved soft data will filter down into stronger hard data? The BoE thinks it will, slowly, with 0.2% growth forecast for Q1 and 0.3% growth forecast for Q2.

The BoE will not be tempted to cut rates on today’s prints instead the wait and see approach remains fitting, helping to lift the pound marginally.

Yet the disappointing hard data prints could change over the coming months, as we have seen in recent survey’s, optimism has improved considerably following December’s general election. The big question is whether the improved soft data will filter down into stronger hard data? The BoE thinks it will, slowly, with 0.2% growth forecast for Q1 and 0.3% growth forecast for Q2.

The BoE will not be tempted to cut rates on today’s prints instead the wait and see approach remains fitting, helping to lift the pound marginally.

Powell’s Testimony Before Congress

Attention will now turn to Fed Chair Jerome Powell who is due to testify before Congress today and tomorrow. His testimony comes at a key junction for the US economy as is leaves behind a bruising trade dispute with China, as the Fed battles low inflation but a sold labor market.

Jerome Powell will hope to give his views on the economy and hint towards the path of monetary policy without tying himself or the Fed down. We expect is to be an overall upbeat testimony with a nod towards the threat of coronavirus to the global economy.

Attention will now turn to Fed Chair Jerome Powell who is due to testify before Congress today and tomorrow. His testimony comes at a key junction for the US economy as is leaves behind a bruising trade dispute with China, as the Fed battles low inflation but a sold labor market.

Jerome Powell will hope to give his views on the economy and hint towards the path of monetary policy without tying himself or the Fed down. We expect is to be an overall upbeat testimony with a nod towards the threat of coronavirus to the global economy.

Level to watch:

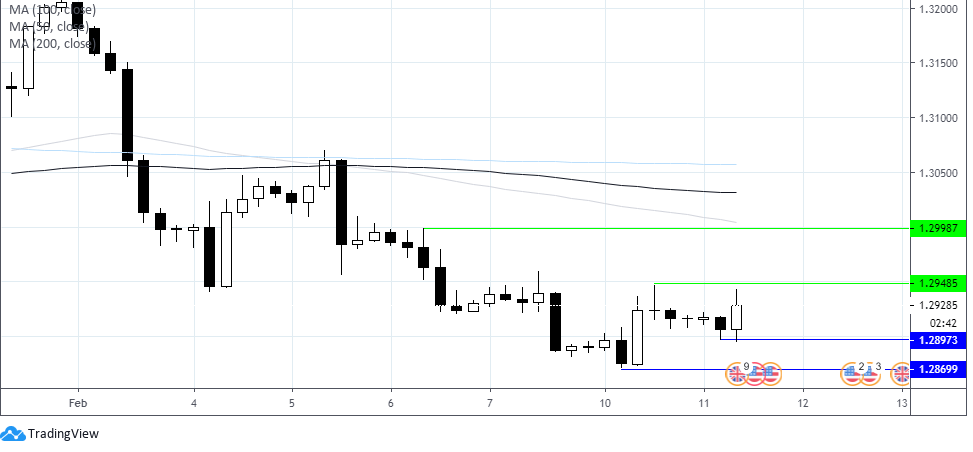

Despite jumping 0.1% higher GBOP/USD continues to trade firmly below its 50, 100 and 200 sma on the 4 hour chart with bearish momentum.

GBP/USD met resistance at yesterday’s high of $1.2948. A move above here could open the door back to $1.30 (high 6th Feb, round number & 50 sma) a level which could negate the current bearish trend.

Immediate support can be seen at yesterday’s and today’s low of $1.2895. A break through here could open the door to $1.2870 the low on (10th Feb).

Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Yesterday 08:18 AM

Latest Dollar articles

Yesterday 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM