The pound has been sold against almost all major currencies over the past couple of days, including the dollar, thanks to the release of notably softer-than-expected UK data. The latest sign of a slowdown is that the UK’s dominant services sector nearly stagnated in June, according to a closely-watched survey. Investors will be focusing on US macro pointers in the afternoon as they assess the health of the world’s largest economy. We will have the latest ISM services PMI later in the afternoon, but first the ADP private sector jobs report in less than an hours’ time. They will be the last of this week’s key US data until the official non-farm jobs report is published on Friday, with US banks being closed in observance of Independence Day on Thursday.

Miserable week for UK data continues

The UK services PMI dropped to 50.2 from 51.0 in May, missing analyst expectations of an unchanged reading. This comes on the back of a string of weaker-than-expected macro pointers. We have seen the weakest manufacturing PMI print since February 2013, weakest construction PMI since April 2009 and the worst composite PMI number since July 2016.

Together, these soft PMI numbers point to a contraction in the economy of 0.1%. That’s according to the chief economist at Markit, who also suggested that it would be "unprecedented for the BOE to not loosen policy with the all-sector (composite) PMI at its current level".

There are no prizes for guessing what Markit blames the downturn on: Brexit-related uncertainty, which has “increasingly exacerbated the impact of a broader global economic slowdown. Risks also remain skewed to the downside as sentiment about the year ahead is worryingly subdued, suggesting the third quarter could see businesses continue to struggle."

BoE rate cuts jumps above 50%

As well as soft data, investors have dumped the pound after the Governor of the Bank of England, Mark Carney, said that “a global trade war and a no-deal Brexit remain growing possibilities not certainties.” This raised speculation that the BoE could consider cutting interest rates. Indeed, the probability of a rate cut this year jumped to over 50%, more than doubling from the end of last week, according to Bloomberg calculations.

So, everything considered, at this stage, it is difficult to argue for pound strength.

Focus turns to the US

In the afternoon, we will have a handful of macro pointers to look forward to from the US, the most important of which will be the APD payrolls report and the ISM non-manufacturing PMI. ADP is expected to come in at 140K following last month’s disappointing 26K print, while the ISM PMI is seen at 56.1, down slightly from 56.9 previously. As well as the headline PMI, investors will be eyeing the employment component of the ISM report as it provides a strong clue for hiring ahead of the publication of the non-farm payrolls report on Friday.

If these US numbers comes in above expectations then the GBP/USD could further extend its losses, while disappointment could see the greenback resume its bearish trend - although the pound would probably not be the currency to trade the dollar’s potential weakness against.

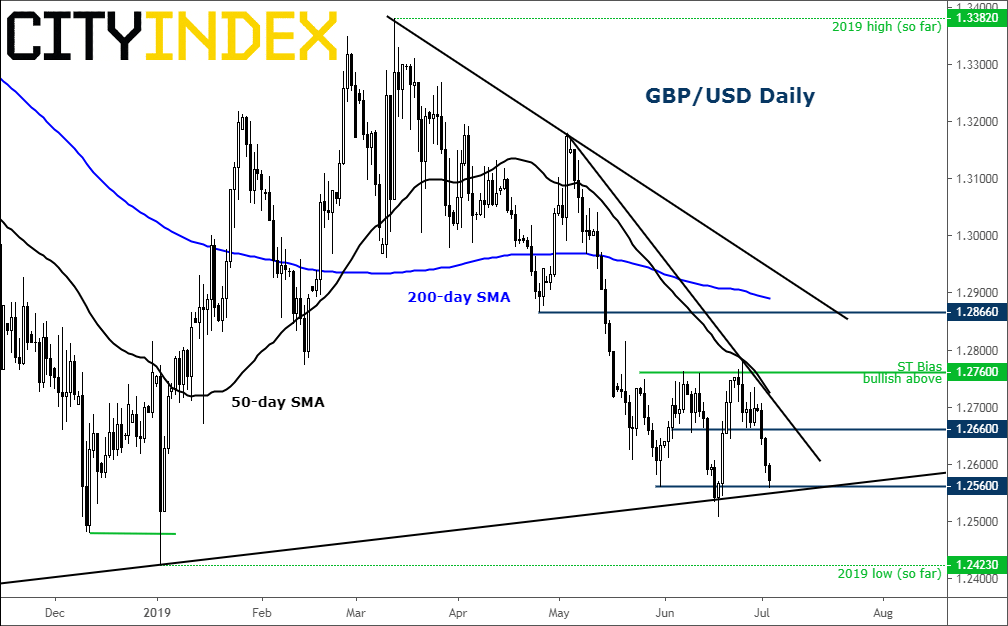

GBP/USD technicals

Ahead of the publication of US macro pointers, the GBP/USD was testing potential support at 1.2560. In the event the cable breaks through this level, then a push towards the January low at 1.2420/5 area would become likely. On the upside, potential resistance comes in around 1.2660, an old support level. We would drop our bearish view only if the cable were to create a higher high above its most recent high (circa 1.2760).

Source: Trading View and City Index

Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM