After so much debate, back and forth, a few extensions and two Prime Ministers later, UK Parliament has decided to call a general election in order to break the Brexit deadlock. With Brexit paused for a few weeks, any sharp movements in the GBP/USD in the interim will likely come from the other side of the pond and the dollar. And there are plenty of factors which could move the reserve currency sharply this week. Not least, the Federal Reserve.

December 12

The December 12 election could decide when the UK will finally exit the EU now that a no-deal departure is off the table. The focus will now turn to the election campaigns by the leading parties and, in turn, to polls to indicate which direction the electorate is heading. Although Johnson’s Conservatives are favourites to win the majority of the votes, which would pave the way for his Brexit deal to be passed, recent elections suggest anything could happen. There is more than 6 weeks to go and a lot could change. So, it is still possible, for example, that we could have a hung parliament, which could be the worst case scenario.

Watch the polls

From now on until the date of the election, the pound may hang around or below the $1.30 handle as investors await political direction. The currency will remain headline-driven, especially as we approach December 12 as new polls emerge. So, domestic data will continue to play second fiddle to political developments moving forward.

Could the Fed’s hawkish cut undermine cable?

Given that the Fed has met analyst expectations about interest rates over the past 73 consecutive meetings, a 25 basis-point cut, which is widely expected this time, is therefore almost certain. What is not so certain is whether this rate decision will be a so-called dovish cut or a hawkish cut. With some FOMC officials recently dissenting in favour of no cuts, policy makers may not see the need to ease more in December, even if consumer confidence has hit a four-month-low or manufacturing activity has slowed down noticeably. With the S&P and Nasdaq at record highs, and a thawing US-China friction, policy makers at the Fed may signal a pause in the rate cutting cycle.

Plenty of US macro data to impact the dollar

Also this week, we will have plenty of key macro data from the US, starting with ADP private sector payrolls report at 13:15 later this afternoon. Meanwhile the third quarter Advance GDP estimate is due to come out at 13:30 GMT today and is expected to confirm a slowdown in growth at the world’s largest economy. Growth is seen expanding by just 1.6% on an annualised quarter-over-quarter basis (quarterly change x4). We will have a handful of macro pointers tomorrow followed by the key non-farm payrolls report on Friday, when we will also have the latest manufacturing PMI.

So, as we move to the second half of the week, the focus will turn to the US economy and away from UK parliament in so far as the cable is concerned.

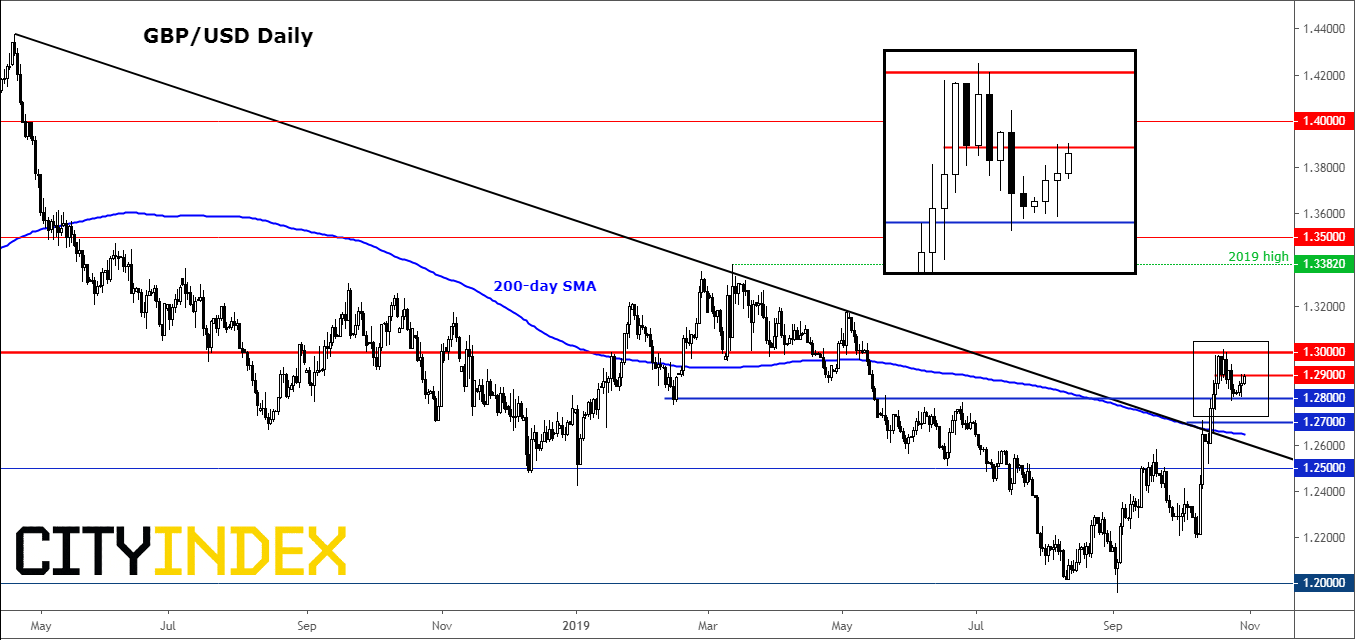

Levels to watch on GBP/USD

Source: Trading View and City Index.

With rates recently stalling near the $1.30 handle and given the prospects of a hawkish cut from the Fed today, the GBP/USD could ease a little further in what still is an overall bullish price structure. Key short term resistance comes in or around 1.2900 followed by the psychologically-important 1.30 handle. On the downside, 1.2850 and 1.2800 are among short term levels that the bulls must defend if they are to retain control. A potential breakdown could see rates drop to the next key level of 1.2700 which I consider a support level based on the weekly price action.

Latest market news

Today 08:33 AM

Latest Forex articles

Yesterday 04:47 AM

April 16, 2024 12:00 PM

April 16, 2024 04:24 AM