GBPUSD 1 5560 70 in focus as credit rating and Greek fears take hold

Sterling doesn’t seem fazed by the latest mutterings from Standard & Poor’s the credit rating agency. Late last week the S&P said that a referendum […]

Sterling doesn’t seem fazed by the latest mutterings from Standard & Poor’s the credit rating agency. Late last week the S&P said that a referendum […]

Sterling doesn’t seem fazed by the latest mutterings from Standard & Poor’s the credit rating agency. Late last week the S&P said that a referendum on the UK’s EU membership could hurt the UK’s credit rating as it may make it difficult for the UK to fund its deficit and a referendum could damage its trade relationships within the UK. These are all relevant fears, but with the election out of the way, politics is not a key driver of the pound right now.

Key fundamental risks for the pound:

Rather than politics, the market is instead focusing on this week’s major fundamental risks which include:

On balance, the market is expecting some strong UK data this week, which could boost rate hike expectations, particularly if inflation picks up even more than expected. So far, GBP swaps are pricing in 50 bps of rate hikes over the next year, but if this week’s data surprises on the upside then the market may accelerate its expectation of when the BOE may start to hike rates.

The impact on the pound:

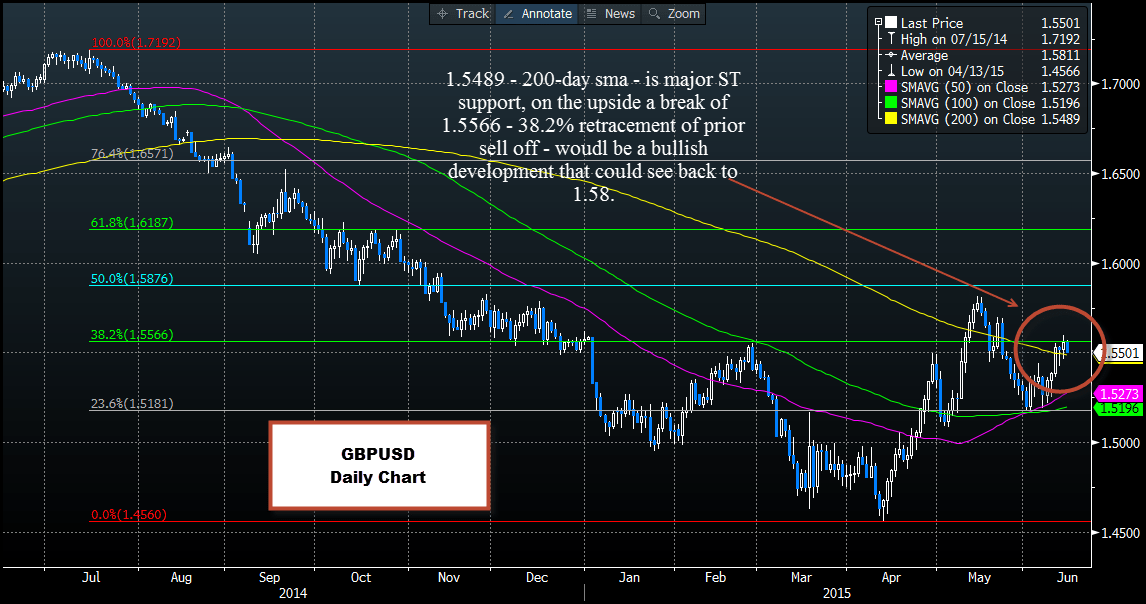

Since the key driver of the FX market right now is relative interest rates, this week’s data matters for GBP. GBPUSD has fallen back on Monday as the dollar gets a boost from safe haven flows on the back of the Greek news. All eyes will be on whether it can manage to hold above the 200-day sma at 1.5489. While this is important support, we expect the pound to be volatile in the next few days as the market digests all of the fundamental news. If GBPUSD does fall below 1.5489 the bulls should not lose hope, as a strong CPI reading on Tuesday could see GBP bounce off recent lows.

In the longer term, we continue to think that the bias could be higher for GBPUSD, but there are a few hurdles it needs to jump first:

We need to see a close above 1.5566 this week before we can get excited about a rebound in the pound. However, this level will be in focus as the market waits to see if the fundamentals and technicals can line up to give sterling bulls something to shout about.

Takeaway: