GBP USD sustains climb as dollar continues to get pounded

Despite rather lackluster economic data out of the UK last month, a continuing aura of dovishness emanating from the Bank of England, and ongoing anticipation […]

Despite rather lackluster economic data out of the UK last month, a continuing aura of dovishness emanating from the Bank of England, and ongoing anticipation […]

Despite rather lackluster economic data out of the UK last month, a continuing aura of dovishness emanating from the Bank of England, and ongoing anticipation of a potentially pound-pounding “Brexit” referendum in June, the GBP/USD has not only managed to stay afloat, but also to thrive during most of the month of April and now into May.

Much of the sharp rise for the currency pair since early April from the 1.4000 level, just off February’s multi-year lows, has been driven by a recent weakening of the US dollar that has been pressured by a dovish Fed and some disappointing US economic data. Last week, the Fed issued its monetary policy statement which, though it kept interest rates unchanged as expected, highlighted the central bank’s increasingly cautious policy stance with respect to further rate increases. Additionally, much of April was characterized by weak US economic releases, including lower-than-expected readings for key inflation indices, retail sales, manufacturing, durable goods orders, consumer confidence, and estimated GDP.

While the dollar has suffered from these data-driven blows, the pound has not been without its own issues. Key among these issues for the past several weeks and months, has been the prospect of the UK exiting the European Union (Brexit), which will be voted on during a late June referendum. Polls of UK citizens ahead of the vote have continued to vacillate, with most recent polls suggesting a slight edge for those who support a Brexit. Analysts have projected that a UK exit of the EU could have severely negative consequences for the British pound.

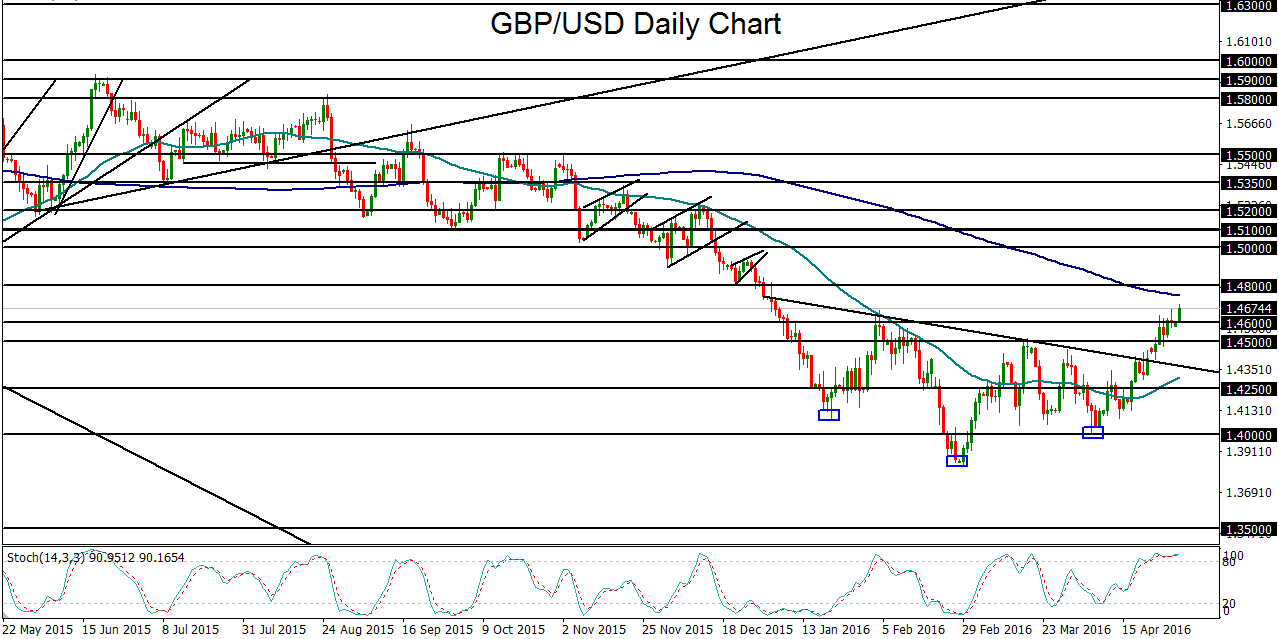

Despite this dark shadow hanging over the UK’s currency, GBP/USD has continued to recover sharply from its lows, at least for the time being. Slightly more than a week ago, the currency pair broke out above a major, inverted head-and-shoulders pattern, which indicated a potential bottom having been established after nearly a seven-year low of 1.3835 was hit in late February.

Next week, the Bank of England unveils its updated stance on interest rates during its monetary policy summary. Though the central bank is not expected to make policy changes, any shift in its message, whether unexpectedly hawkish or even more dovish, could prompt a significant move for the pound. On the dollar side, the end of this week brings highly-anticipated employment data from the US in the form of the Non-Farm Payrolls report. Again, any unexpected outcome from that data release could lead to either a change or a reinforcement of the dollar’s current downtrend.

Currently, GBP/USD has followed-through to the upside with a tentative breakout above the 1.4600 prior resistance area. In the process, it has closely approached its 200-day moving average for the first time since November of last year. With any continued upside momentum, the next major upside target is at the key 1.4800 resistance level followed by the 1.5000 psychological level, with the actual head-and-shoulders measured target residing around 1.5100.