GBP USD shows signs of life

The GBP/USD ended higher last week on the back of surprisingly stronger-than-expected UK economic data and as the dollar eased along with expectations about an […]

The GBP/USD ended higher last week on the back of surprisingly stronger-than-expected UK economic data and as the dollar eased along with expectations about an […]

The GBP/USD ended higher last week on the back of surprisingly stronger-than-expected UK economic data and as the dollar eased along with expectations about an imminent rate hike in the US. But the Cable did sell off heavily on Friday, which took some shine off the week’s rally. Apparently, Friday’s weakness in sterling was due to speculation about the time when UK Prime Minister Theresa May will trigger the Article 50 exit clause to start the process of leaving the EU. At the weekend, a speech by Fed’s Vice Chairman Stanley Fischer gave rise to renewed speculation about a sooner-than-expected rate hike there once again. As a result, the Dollar Index further extended its bounce from Friday, causing the EUR/USD to drop below the 1.13 handle once again this morning. However, the pound held its own relatively well and by mid-morning it was trading at a good 1.31 against the dollar. In fact, the pound was also up against the other major currencies, including the euro and yen. As there was no fresh news out to support the pound, the currency was perhaps finding support from short-covering.

New record high for sterling short positions

Indeed, net short positions in sterling climbed to a new record high of 94,238 contracts in the week to Tuesday, up from about 90,000 the previous week, according to the latest positioning data from the CFTC. Speculators have been adding to their short positions every week since the UK voted to leave the EU. Clearly, the GBP has been becoming a one-sided trade. But what this means is that you will get to see lots of short squeeze rallies every now and again, especially as the main GBP-negative factors are already out of the way now, including the Brexit vote and BoE’s response. But ultimately we are in a bear market environment, so the bounces are unlikely to last long. However, the worst of the GBP’s declines could be behind us now, especially if we see further improvement in UK data in the coming weeks.

This week though, there won’t be much data to concentrate on until Friday when the second GDP estimates for both the UK and US are released. In addition, the Jackson Hole symposium will also get underway then, when the Fed’s Chairwoman Janet Yellen may hint at a rate hike. So, it could a quite few days in terms of data and news, but that should change on Friday.

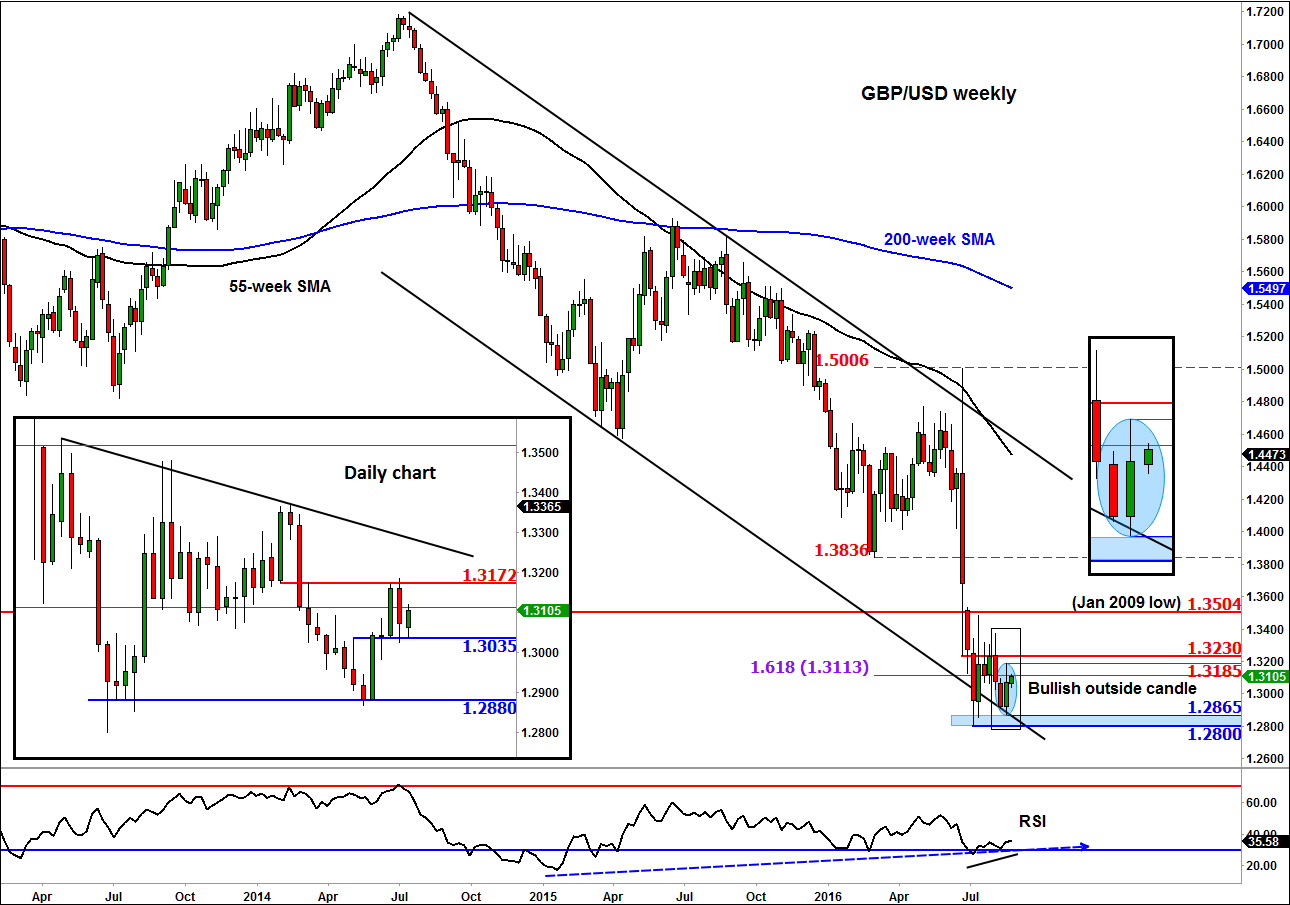

Technical outlook

From a technical perspective, the GBP/USD remains depressed near the support trend of its long-term bearish channel, but with a few signs of life – such as the bullish engulfing candle that was formed on the main weekly chart last week. In addition, the RSI has been in a state of positive divergence, making higher lows as the underlying price action has been making lower lows. Together, these technical indications suggest that the bearish momentum is waning and that we may see a continuation of the bounce from last week. But for the potentially rally to be noticeable, the GBP/USD will need to clear last week’s high of 1.3185 and the pivotal level around 1.3230 which, on a weekly closing basis, has kept the gains in check for several weeks now. Meanwhile on the daily chart (inset), the Cable appears to be making incremental higher lows, with old resistance levels such as 1.3035 becoming support. If this level were to break down then it would be a bearish development in the short-term outlook, potentially paving the way for a revisit of the 1.2880 key support level.