GBP USD Shifts to 2 Year Spreads

Although today’s release of UK employment date appeared neutral by the measure of the ILO figures used by the Bank of England, the second consecutively […]

Although today’s release of UK employment date appeared neutral by the measure of the ILO figures used by the Bank of England, the second consecutively […]

Although today’s release of UK employment date appeared neutral by the measure of the ILO figures used by the Bank of England, the second consecutively monthly decline of 29K in claimant unemployment as well as 2.1% jump in average weekly earnings under the ONS statistics tell a more favourable picture.

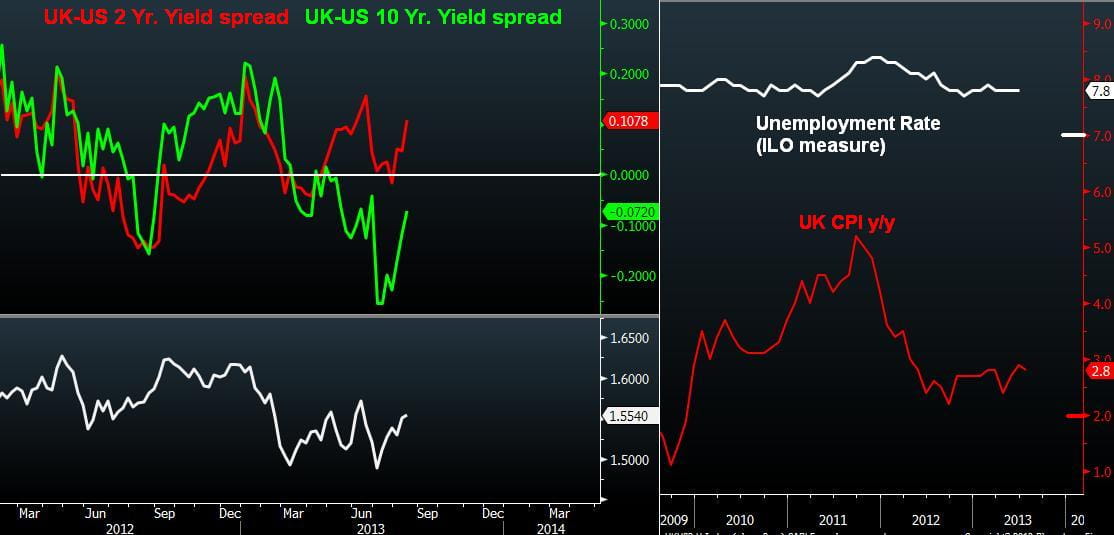

UK 2-year yields further surpass their US counterparts into positive territory while 10-year gilt yields are not far from doing the same. The sharper move in the UK-US 2 year spread to 0.11% is a manifestation of the 3 exceptions given by BoE governor Carney regarding his forward guidance on keeping rates low for about 3 years.

Two of the three conditions for keeping low rates until unemployment nears 7.0% are tied to inflation forecasts not exceeding 2.5% in 18-24 months and for inflation expectations to remain anchored. What seemed to be mere detail is now becoming the basis for bond vigilantes lifting up UK yields against the expectations and preference of the Bank of England.

The improvement in economic data has been unquestionable, but this has allowed private economists and bond traders to anticipate at least one of these conditions to materialize. Specifically, the rate of data improvement could trigger CPI towards 2.5% well before unemployment reaches 7.0%. And we could well reach a situation whereby the BoE’s CPI forecast maybe at odds with the bond market, at which point renewed dissent between the doves and hawks will reappear.

Although the Federal Reserve’s conditions for forward guidance are largely similar to those of the BoE “…at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored”, the BoE’s 7.0% unemployment guidance is deemed excessively low for the UK’s inflationary tendencies.

At the end of day, Carney’s message was not so different from Bernanke’s. Rates will not be raised before 2 year’s time. Bernanke referred to 6.5% unemployment and Carney referred to 7.0% unemployment. 2015 and 2016 are so far off that they reduce the relevance of longer-term yields and shift volatility towards the shorter-end of the curve. Regardless of whether gilt traders deem the 7.0% level too far, or too close, the conclusion could be the same: Higher rates in the event of faster decline in unemployment, or higher rates in the event of faster inflation expectations despite sticky unemployment. This will give added importance to macro data watching, and currency traders eyeing yield differentials will increasingly focus onto 2-year yields in the UK and the US as the central banks of both nations perfect the art of forward guidance.