GBP USD extends fall on increasing Brexit support

Despite a dollar pullback on Wednesday, sterling weakness dominated price action for GBP/USD, extending the currency pair’s plunge from Tuesday. This sharp retreat for GBP/USD […]

Despite a dollar pullback on Wednesday, sterling weakness dominated price action for GBP/USD, extending the currency pair’s plunge from Tuesday. This sharp retreat for GBP/USD […]

Despite a dollar pullback on Wednesday, sterling weakness dominated price action for GBP/USD, extending the currency pair’s plunge from Tuesday. This sharp retreat for GBP/USD in the first half of the week has been driven largely by a resurgence of popular support in favor of the UK leaving the European Union, as reflected in the latest polls. These polls have shown that the possibility of a “Brexit” outcome still remains a major risk factor for financial markets, most notably the pound, in the run-up to the June 23 EU referendum only three weeks from now.

Whereas the “Remain” camp had enjoyed a commanding lead in both telephone and online polling within the past several weeks, the “Leave” camp has significantly closed the gap in the most recent polls. In some cases, Brexit supporters have now assumed the lead – polls conducted in conjunction with The Guardian newspaper have shown this lead extend to 52% vs 48% in favor of a UK exit. A major factor leading to this increased Brexit support has been widely attributed to concerns over UK immigration control and policy.

As the EU referendum draws closer, GBP/USD also continues to be impacted by vacillating speculation over the possibility of a US interest rate hike by the Federal Reserve. Although the Fed has telegraphed its intentions of raising rates in coming months if economic data continues to cooperate, a June hike remains much less likely due to the increased risk of a Brexit that could very well weigh on the Fed’s tightening aims. In contrast, while a July rate hike is significantly more likely, it will be heavily dependent on the outcome of the EU referendum, in addition to further improvements in US data. A Remain outcome should further raise the probability of a July hike, while a Leave outcome could very well preclude a Fed decision to raise rates this summer.

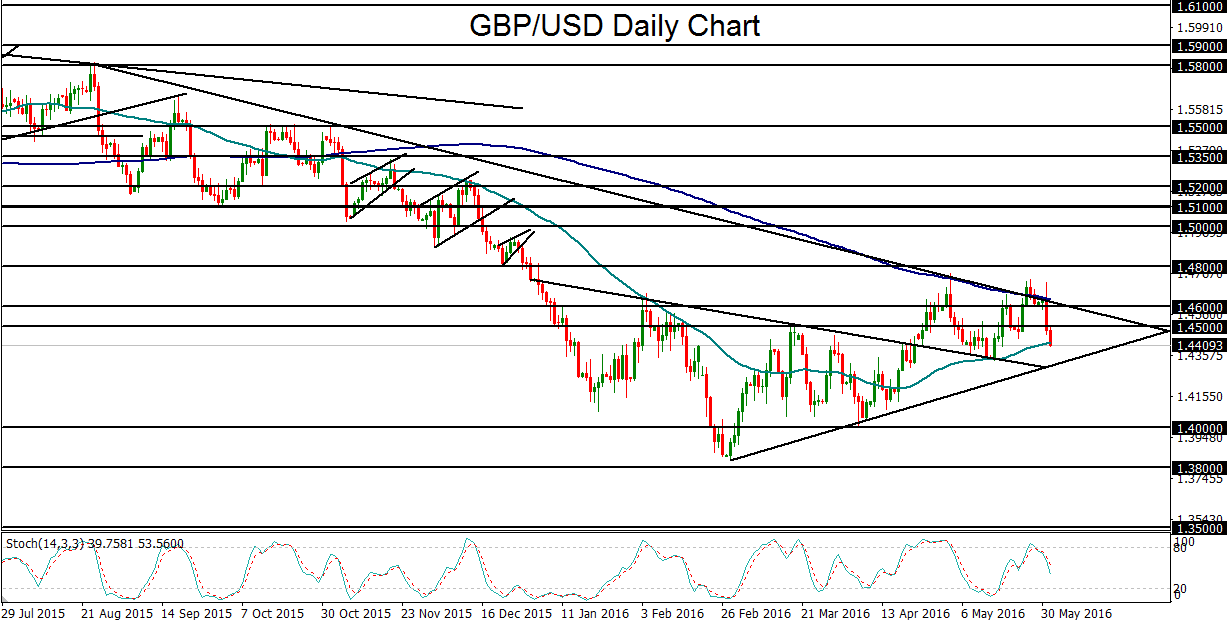

In light of these upcoming risk events, it is no surprise that GBP/USD has begun to price-in the real market risk of a potential Brexit. Since the multi-year low of 1.3835 was hit in late February, the currency pair has been trading within a rising trend as Brexit worries gradually abated. This rise and recovery, however, have remained within a longer-term downtrend as outlined by both a descending trend line extending back to the August high of last year as well as a steadily falling 200-day moving average. Although the past week has seen GBP/USD rise slightly above both the moving average and trend line, this week’s fall has signified a strong retreat from resistance.

Currently trading well under the 1.4500 level, GBP/USD should continue to be pressured as long as it remains below the noted resistance. This pressure could be especially strong if this Friday’s US Non-Farm Payrolls data is encouraging, further supporting a near-term Fed rate hike. More importantly, however, if UK polling continues to follow its current trend in favor of the pro-Brexit camp, GBP/USD could have significantly more to fall in the coming weeks. With any further retreat from the 200-day moving average and the noted downtrend line, the next major downside target remains at the 1.4000 psychological support level.