GBP USD could turn volatile as investors eye UK US CPI

Last week, the British pound was among the strongest of currencies in G10. The week before, it was one of the weakest. Clearly, speculators who […]

Last week, the British pound was among the strongest of currencies in G10. The week before, it was one of the weakest. Clearly, speculators who […]

Last week, the British pound was among the strongest of currencies in G10. The week before, it was one of the weakest. Clearly, speculators who had established short positions in GBP, especially against the USD, after that surprisingly dovish Bank of England Inflation Report, used the opportunity of a mostly US data-void week to book profit on their positions throughout last week. In addition, we had some stronger employment data from the UK last Wednesday which provided additional support for the pound, while the second-tier US numbers were mostly weaker than anticipated. At the start of this week, the GBP/USD is finding itself under a bit of pressure thanks to a stronger dollar, though the pound crosses are showing resilience once more. But is the pound about to get pounded again?

Well, to a certain degree a lot will depend on the outcome of tomorrow’s UK inflation data from the ONS. The headline Consumer Price Index (CPI) is expected to have remained unchanged at -0.1% year-over-year in October, while core CPI is seen steady at +1.0%. The Retail Price Index (RPI) is expected to show a small uptick to 0.9% from 0.8% previously. But it is not just the UK data that traders will need to worry about tomorrow.

From the US, we will also have the CPI data, with the headline and core versions both expected to show +0.2% month-over-month readings. Obviously inflation is the key missing piece in the jigsaw for the Federal Reserve and if the CPI shows a strong reading then calls for a December rate increase will only rise, potentially leading to further strength in US dollar. This could be bad news for the Cable.

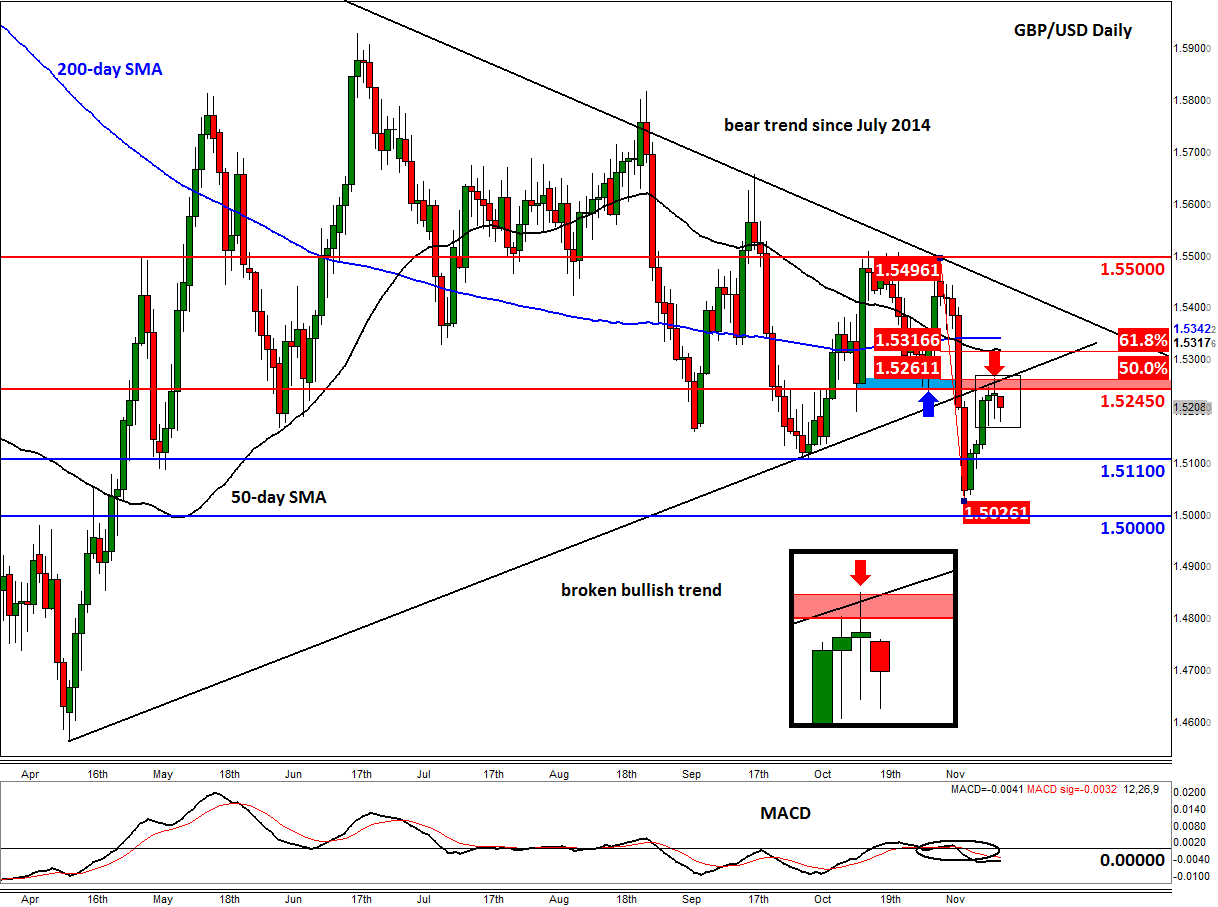

So, depending on the outcome of tomorrow’s inflation data from both the UK and US, the GBP/USD may be about to resume its move lower especially since it has also held below the technically important 1.5245/60 area, which we highlighted in our report last week. This area was previously support and corresponds with the underside of the broken bullish trend line and the 50% retracement level of the most recent drop. So, for as long as it remains below here, one could remain reasonably confident that next major move could be to the downside rather than the upside. If the GBP falls says on the back of a potentially weaker UK CPI reading tomorrow, then it could mark the start of a major move to the downside, though in the near-term it may find support here and there including around 1.5110 and the psychologically-important 1.50 handle. However, a closing break above the aforementioned 1.5245/60 region would invalidate any short-term bearish setup and may lead to a sharp short squeeze rally.

In short, the GBP/USD is on the verge of a potentially sharp move as it holds below an important resistance area ahead of the release of key inflation data from both sides of the pond, starting with the UK CPI tomorrow morning.