GBP USD BoE holds policy focus turns to key US data

Following the recent improvement in UK data, the Bank of England was widely expected to sound a little more upbeat about the economic outlook with […]

Following the recent improvement in UK data, the Bank of England was widely expected to sound a little more upbeat about the economic outlook with […]

Following the recent improvement in UK data, the Bank of England was widely expected to sound a little more upbeat about the economic outlook with virtually no one forecasting any further easing of monetary policy. And so it proved that way, with the BoE holding interest rates and QE unchanged at 0.25% and £435 billion respectively, in a unanimous decision. The minutes showed few surprises. The bank did acknowledge the improvement in UK data and consequently expects growth in the third quarter to be 0.2% compared to zero previously. Among the MPC, Kristin Forbes and Ian McCafferty said that they still believed that the current outlook did “not fully warrant” the additional stimulus, though they would not vote against its continuation “for now” as it could have negative implications for the economy. The Bank did however re-iterate that if the outlook is broadly consistent with their August projections, then “a majority of members expected to support a further cut” to close to zero.

Sterling, already boosted by this morning’s forecast-beating retail sales data, staged a bit of a relief rally initially, though selling pressure quickly resumed. But the drama is not over for the GBP/USD pair, because now the focus turns to the US economy where it is going to be a very busy day today. The US “data dump” in the afternoon includes the latest readings on retail sales, jobless claims, producer price index, industrial production, capacity utilization rate and Philly Fed and Empire State manufacturing indices. All of that look forward to shortly. But one should remember that for the dollar to make a noticeable move on the back of these numbers, we will need to see a big surprise, especially in retail sales.

Perhaps even more important for the dollar and the markets in general will be Friday’s data which include the latest headline and core Consumer Price Index (CPI) measures of inflation and a closely-watched consumer sentiment survey. Unsurprisingly, most of the focus will be on those CPI figures as they will be the last significant US data for policymakers at the Fed to base their decision on next week. The volatility in the pound should rise further in the coming days as a result.

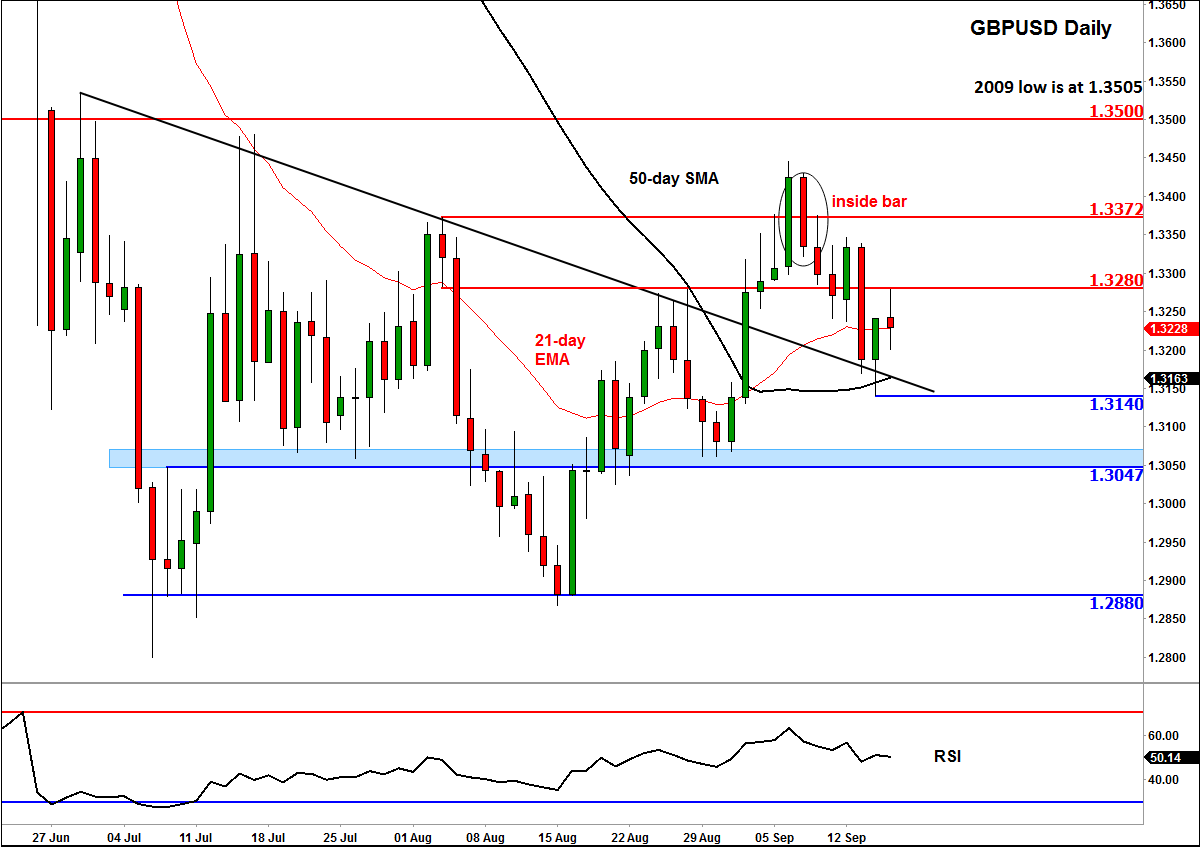

But once the dust settles down, we will hopefully get to see the formation of a distinct trend and move away from the current consolidation phase, which is what the daily chart of the GBP/USD currently shows. That being said, there have been some slight bullish indications in recent times, although to be honest I am clutching at straws. Nevertheless, a short-term downward trend has broken down and the 50-day moving average is now pointing higher with price sitting above it, for now. In the short-term, a bullish scenario would be if price were to break resistance at 1.3280. If seen, this should pave the way for a move towards 1.3370/5 area next, which was previously resistance. The key level to watch is around 1.35. This psychological level also corresponds with the low that was made back in 2009 (at 1.3505). Meanwhile a bearish scenario would be if the Cable were to snap back below the 50-day moving average on a daily closing basis.