The British pound has continued to point both whilst conservative lead in the polls. With their lead narrowing and a defiantly strong British pound, it begs the question as to whether cable’s upside could be limited.

Whilst the polls vary slightly, they point towards a Conservative Party victory. Yet whilst their lead has narrowed in recent sessions, it is yet to be reflected in price action with cable remaining anchored to its highs.

This begs the question as to how much upside GBP/USD is capable of after such a stellar run and, at such giddy heights, surely leaves the British pound vulnerable to a volatile fall should polls get it wrong again.

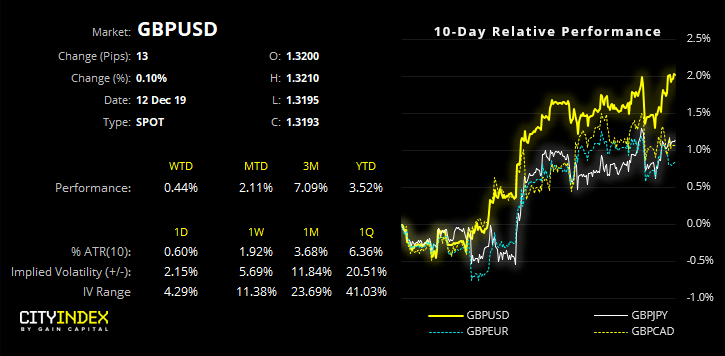

As you’d expect, implied volatility has spiked higher this week with the 1-week IV implying ~2% move in either direction. Given realised volatility relatively low, it leaves room for plenty of movement in either direction.

With polls closing at 22:00 GMT and counting officially begins, we should begin to see some action from 22:30 – 23:00 GMT, with a result pencilled in for around 0200 GMT on Friday morning.

In today’s video, we look at price action on GBP/USD and highlight why a pullback is on the cards regardless of the result. Of course, the election’s outcome will have a direct impact on its timing and just how much more bulls can squeeze out of this move.

Related Analysis:

The four likeliest UK election scenarios - as things stand right now

GBP and Election Fever

Latest market news

Today 05:45 AM

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Latest Dollar articles

Yesterday 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM