GBP on the precipice

Sterling remains the weakest performer in the G10 so far today, in fact against a basket of expanded major currencies the only one that has […]

Sterling remains the weakest performer in the G10 so far today, in fact against a basket of expanded major currencies the only one that has […]

Sterling remains the weakest performer in the G10 so far today, in fact against a basket of expanded major currencies the only one that has performed worse than the pound is the Columbian peso, after the country voted to reject a peace deal with the rebel group Farc.

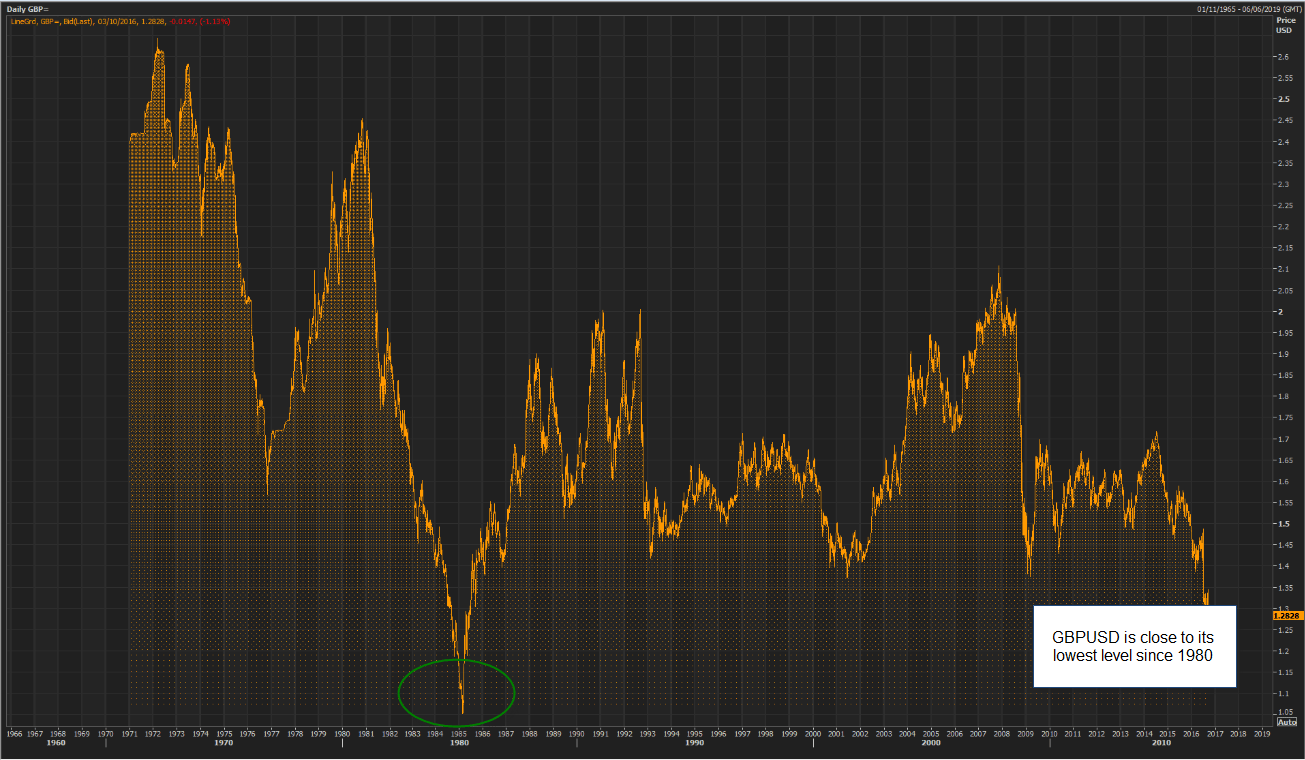

The driver of sterling weakness was Theresa May’s Tory Party conference speech, which suggests a hard Brexit is on the cards. Article 50 is likely to be triggered by March next year, however, Article 50 only deals with the practicalities of leaving the EU, it does not include a trade deal. Any trade negotiations between the UK and Europe will need to be held separately, and here lies the problem, on Monday some EU members stated that there will be no tariff free trade without single market membership, something Theresa May does not seem that bothered with maintaining. This is spooking FX traders, as a hard Brexit could mean economic misery for the UK. The pound touched a fresh 5-year low versus the euro on Monday, and GBP/USD is edging closer to its post-Brexit low of 1.2798, reached on 6th July.

This is a pivotal level for GBP/USD, if it can hold above 1.2798, then we would expect a short-term bounce in the pound, as profit taking on short GBP positions may halt the selling pressure in the short-term. However, if it falls through this level then it could herald a new wave of sterling selling, and potentially another bout of downward pressure on GBP/USD towards 1.25 and even 1.20 in the coming weeks.

GBP/USD depends on US economic data

On balance we would expect to see some stickiness around 1.2798 in GBP/USD as the market switches its focus to the US economic data due out this week. We have already had one positive surprise, the ISM manufacturing index jumped to 51.5 for September, from 49.4 in August. If we see more economic strength emanating from the US then this may strengthen the case for a Fed rate hike in December, which could weigh heavily on GBP/USD. Thus, at the start of a new week and a new quarter, sentiment towards the pound remains extremely shaky. This is good news for UK manufacturers’, not so good for those looking for a longer term GBP recovery.

Figure 1: GBP/USD: close to its lowest level since 1980

Source: Reuters

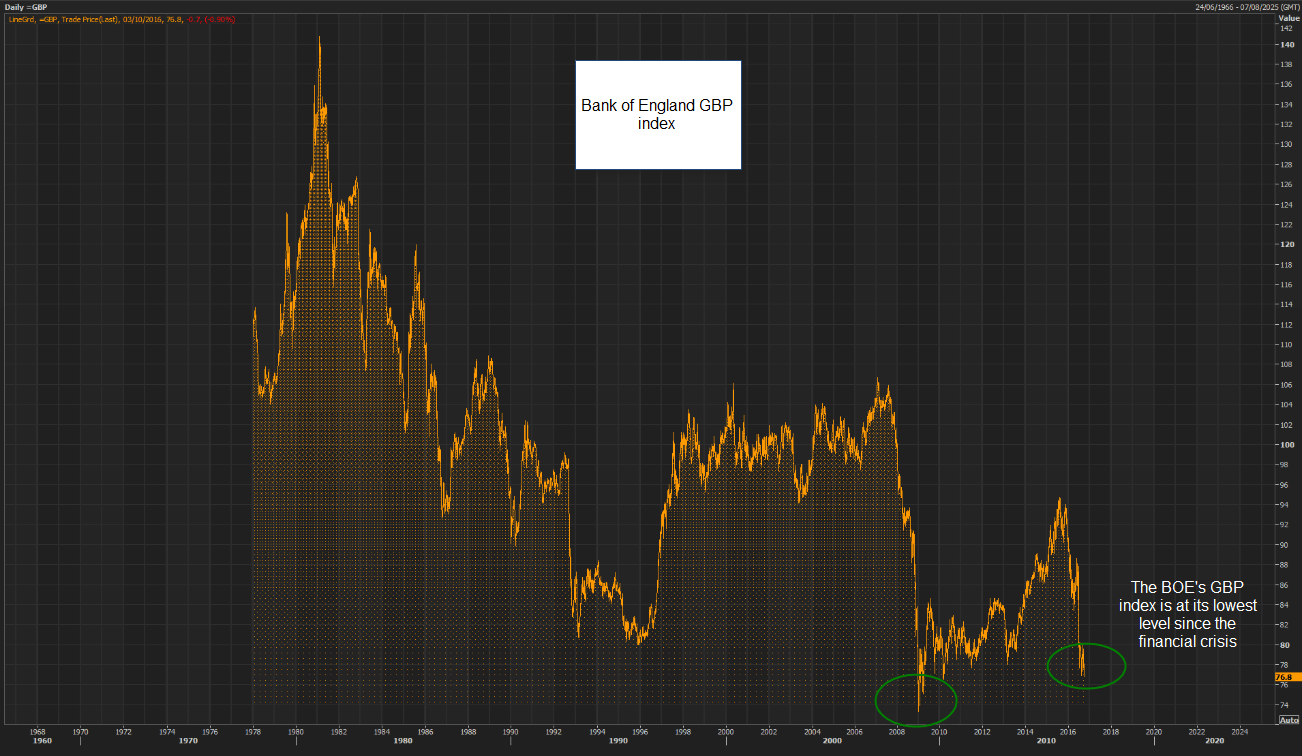

Figure 2: The BOE GBP index, this is at its lowest level since the financial crisis.