GBP likely to continue its downside move against the yen

The British pound’s sharp sell-off in March was largely a result of increasing references to deflationary risks from several Bank of England Monetary Policy Committee […]

The British pound’s sharp sell-off in March was largely a result of increasing references to deflationary risks from several Bank of England Monetary Policy Committee […]

The British pound’s sharp sell-off in March was largely a result of increasing references to deflationary risks from several Bank of England Monetary Policy Committee members. The BoE’s chief Economist Andy Haldane went on to indicate that “…a case can be made for policy easing today” if downside risks to inflation were to materialise. This shifting rhetoric signals a change in policy makers’ stance and further diminishes the probability of a rate hike this year, though Carney’s statement last week that the next rate move will be up pours some cold water on these MPC member attempts. UK inflation fell to 0% in February, hitting the lowest annual rate since comparable records began in 1989. Markets expect inflation to enter negative territory, which will leave little choice for the BoE but to remain dovish.

GBP traders will witness increasing volatility in April as the major political parties start their six-week campaign ahead of the 7th May general election. None of the parties is expected to win the minimum 326 seats required to gain an outright majority, which should lead to another coalition government led by either the Labour or Conservative Party. Uncertainty will be the name of the game at the expense of the pound.

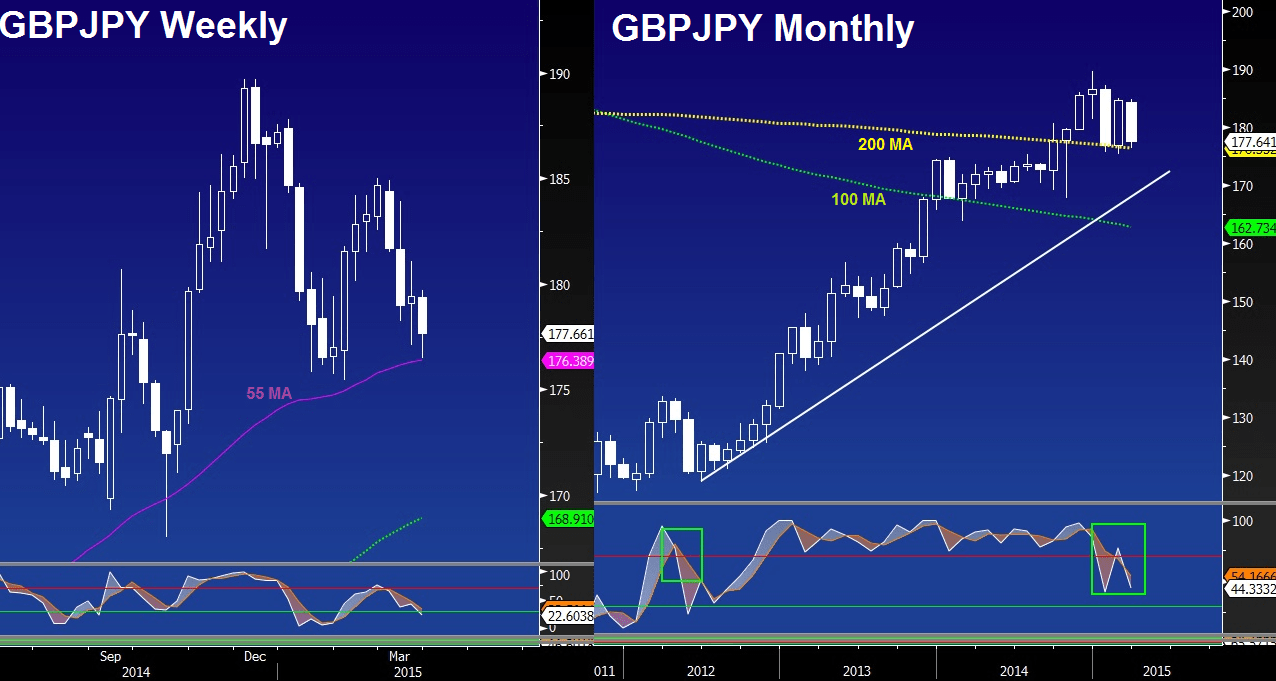

I expect GBP to extend weakness predominantly against JPY as plunging oil prices and a falling yen from the past three years combine to reduce Japan’s importing costs and further improve export competitiveness to the benefit of the currency. These factors have led the Government to upgrade its economic assessment for the first time since July 2014. Re-emerging volatility in global equities will also likely help drag down yen crosses.