GBP JPY remains heavily pressured after Brexit driven plunge

It is of little surprise that sterling has been the hardest hit of all currencies, and indeed of all major financial markets, as a result […]

It is of little surprise that sterling has been the hardest hit of all currencies, and indeed of all major financial markets, as a result […]

It is of little surprise that sterling has been the hardest hit of all currencies, and indeed of all major financial markets, as a result of last week’s surprise UK vote to leave the European Union. The Brexit outcome prompted an immediate chain reaction of severe volatility in markets across the globe, with the British pound absorbing the brunt of the damage, as previously projected. Also as expected, safe haven assets have been strongly boosted as a result of the Brexit-driven financial turmoil, with a particularly strong impact on the Japanese yen.

Having already been in strengthening mode for many months against Japan’s wishes and periodic attempts to stem its continued rise, the yen surged dramatically after it became apparent that the Leave campaign would most likely gain the referendum victory. At the same time, of course, the pound made an historic plunge, dropping well below the key 1.3500 level against the US dollar on Friday and then following-through on Monday to hit a new 31-year low approaching the 1.3100 handle.

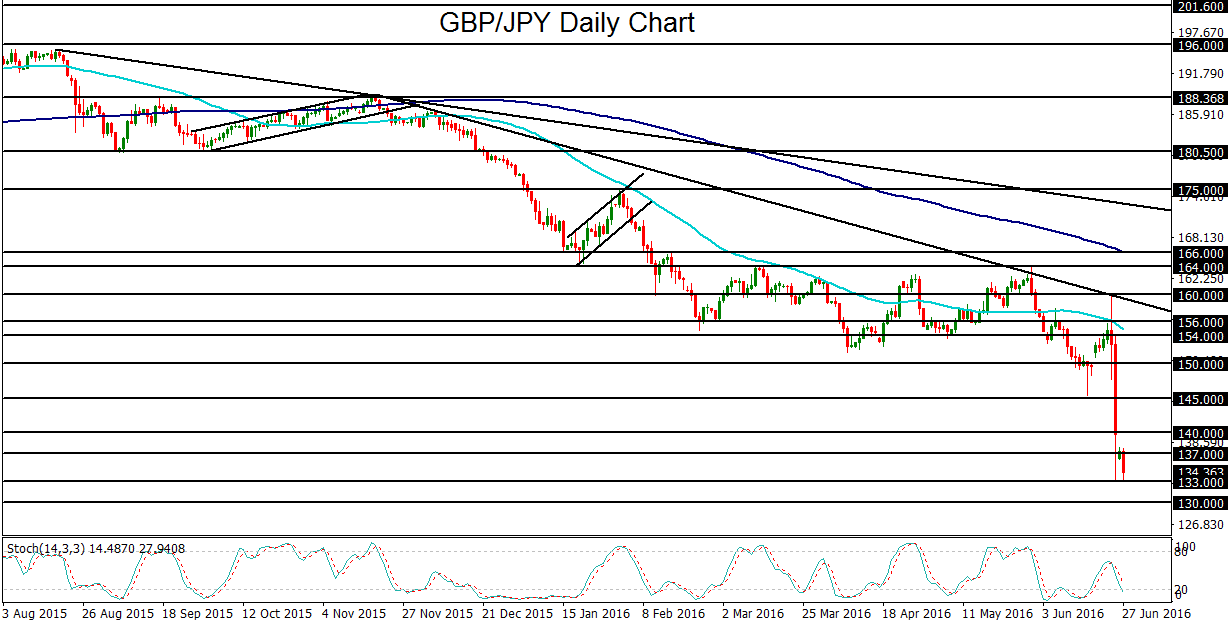

While the GBP/USD plummet has been exceptionally sharp thus far, the drop in GBP/JPY has been even more dramatic. This, again, was due to the double impact of crushing pressure on the pound combined with a rapid flight to the perceived safety of the yen.

GBP/JPY dropped in the early hours of Friday from its already-low position around 152.00 down to a low just above 133.00 support. In the process, the currency pair broke down below its prior long-term low around 145.00 that was set just a week earlier, and went on to establish a new 3½-year low. Some of Friday’s losses were pared through the course of that day, but Monday has seen continued pressure that pushed GBP/JPY back down at one point to re-test the 133.00 support level once again.

The two major central banks most relevant to this currency pair are very likely to have a significant impact on direction going forward. The Bank of England could well be in the position to turn back towards the path of quantitative easing and an interest rate cut if continued financial and economic turmoil resulting from Brexit warrant these measures. This could very likely weigh even further on the pound. As for Japan, there have been numerous warnings in the recent past from Japanese officials touting the government’s readiness and willingness to intervene should the yen become too strong or experience exceptional volatility. That volatility is now occurring, making a potential intervention by Japan a strong likelihood if the yen continues to rise. In the event of an intervention, however, while the immediate reaction might be a sharp drop for the yen, it is unclear how much of a lasting effect Japan’s actions would have on the longer-term weakening of its currency.

Notwithstanding such intervention attempts, the directional bias for GBP/JPY continues to be strongly to the downside in-line with the clear downtrend that has been in place for the past year. The currency pair should remain pressured overall, particularly in light of last week’s Brexit outcome and its ensuing consequences. With any strong breakdown below the noted 133.00 support level, the next major downside objective in the short-term is at the key 130.00 support level.