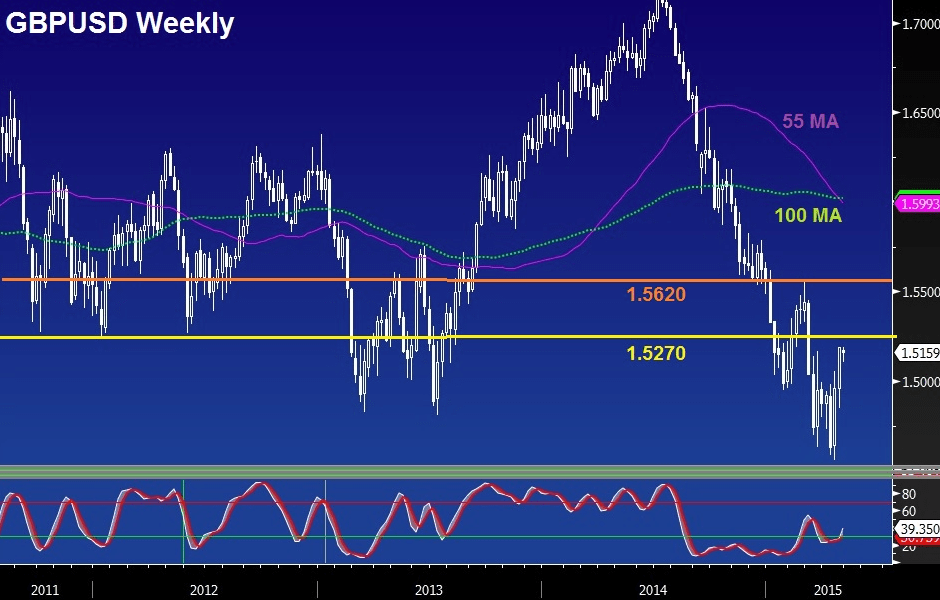

GBP could enjoy post election relief rally

Forecasting GBP/USD ahead of the 7th May UK election faces increased challenges thanks to the likelihood of another hung parliament, mixed UK economic data and […]

Forecasting GBP/USD ahead of the 7th May UK election faces increased challenges thanks to the likelihood of another hung parliament, mixed UK economic data and […]

Forecasting GBP/USD ahead of the 7th May UK election faces increased challenges thanks to the likelihood of another hung parliament, mixed UK economic data and conflicting signals from the US Federal Reserve.

According to recent opinion polls, it is increasingly assumed that none of the major political parties will win the minimum 326 seats required to gain an outright majority in parliament. This means another coalition government led by either Labour or the Conservative Party is the most likely scenario. On 8th May, Britain is at risk of seeing its first minority administration since the 1970s. There will be prolonged talks to form a government, during which the pound will experience heightened volatility.

The downside risks for GBP are associated with a Labour-SNP coalition (fiscal tightening for businesses, more taxation for the wealthy and the likelihood of undershooting budget targets). However, a Conservative-led coalition, which pushes for a referendum on the UK’s EU status is also a risk, though this has been widely discussed among traders already to the extent that it may no longer cast such a negative spell on the market and the pound.

I expect the most likely scenario to be a Conservative-led minority government, formed by Conservatives, Liberal Democrats and the Democratic Unionists Party accumulating about 305-315 seats, which would be insufficient to attain the 326-seat majority but would bring Tories ahead of Labour by a five-to-eight seat margin. This would combine the benefits of incumbent and market-friendly party victory, while eliminating the risk of EU referendum due to Lib Dem opposition to any referendum bill.