GBP CAD Soft UK data unlikely to derail rally

Sterling rallied strongly yesterday when the Bank of England Governor Mark Carney said rate rises were getting closer. But it has lost some of its […]

Sterling rallied strongly yesterday when the Bank of England Governor Mark Carney said rate rises were getting closer. But it has lost some of its […]

Sterling rallied strongly yesterday when the Bank of England Governor Mark Carney said rate rises were getting closer. But it has lost some of its mojo following the publication of the latest UK employment figures this morning which showed the unemployment total has risen for the first time in two years. According to the ONS, some 1.85 million people were unemployed in the March-to-May period, which represents an increase of 15,000 from the previous reading. This helped to push the three-month average rate of unemployment to 5.6%, down from 5.5% in April. Separately, jobless claims rose by 7,000 applications in June following a 6,500 drop in May, confounding expectations for a decline of 8,900. But the average earnings index rose to 3.2% from 2.7% previously. Though this was also slightly weaker than 3.3% expected, it was still the best reading for five years. Excluding bonuses, wages rose to 2.8% from 2.7%, the best pace since February 2008.

Overall it was a mixed-bag jobs report for the UK economy. Investors should not read too much into just one period’s worth of data. Instead they should focus on the trend, which has been falling for both the jobseeker’s allowance and the unemployment. More importantly perhaps, earnings are on the rise which could see inflation start to head north. This in turn may cause the Bank of England to start scaling back QE and embark on a rate-hiking cycle – though probably not before the US Federal Reserve, which is expected to increase rates at the end of this year.

Bank of Canada rate decision looming

So, the pound could remain supported for the foreseeable future, especially against currencies where the central bank is still dovish. One such central bank is the Bank of Canada, which faces an interest rates decision later today. Economists are split – about 50% think a 0.25 percentage point cut to 0.5% is a possibility while the other 50% think the BoC will hold fire at this meeting but instead talk up the prospects of future cuts. The last time the BoC cut rates was in January when in a surprise move 0.25 percentage point was shaved off which brought rates down to their current level of 0.75%.

But that rate cut has so far had little or no impact on the Canadian economy as consumption is still weak. What’s more, the crude rally from March has stalled. This is obviously not good for Canada’s oil exports which it is heavily reliant on. Oil prices are slightly weaker today following Iran’s nuclear agreement with the P5+1 group of world powers yesterday, an agreement that could see an additional 1 million barrels of oil being added to an already-saturated market by the end of this year.

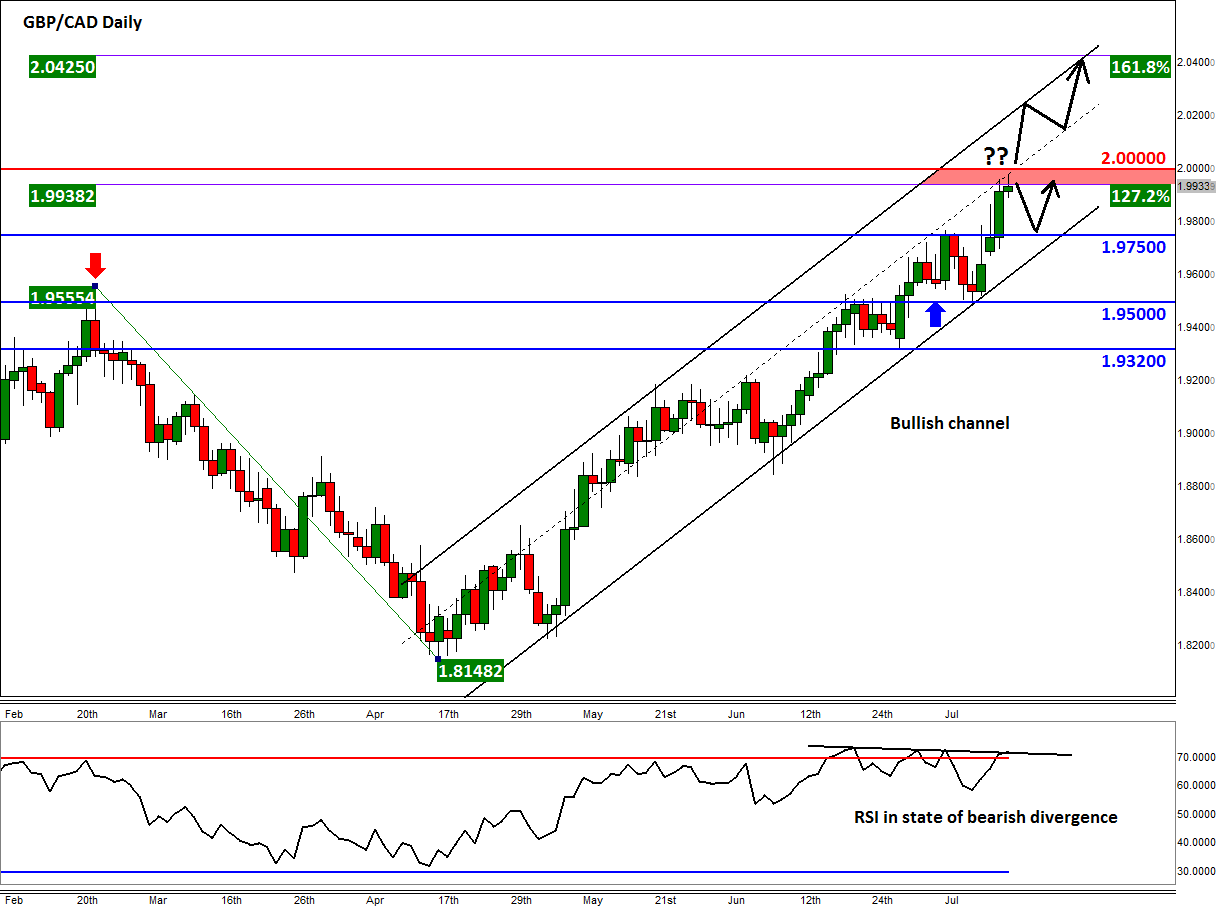

GBP/CAD at key technical juncture

Thus, the Canadian dollar could fall further in the weeks and months ahead. In the short term, the GBP/CAD may be able extend its rally depending on the outcome of the BoC decision today. We last looked at this cross on Monday of last week when we highlighted the formation of a bullish pattern and the breakout above the key 1.9500/55 resistance area. Though the GBP/CAD initially struggled to push further higher, it has now reached the first of our two immediate targets: 1.9940, the 127.2% Fibonacci extension of the last major downswing. Beyond this level is the psychologically-important hurdle of 2.0000.

The close proximity of these technical factors means there is a risk that price could retreat from around 2.00 on profit-taking – especially if accompanied by an oil price rally or if the BoC sounds less dovish and/or the GBP tumbles. The RSI meanwhile is in a state of bearish divergence: it has been making a series of lower highs while price has made higher highs. This suggests that the buying momentum may be weakening. Still, the downside could be limited to support at 1.9750 or slightly lower to the bullish trend of the channel.

That being said, while the GBP/CAD remains inside its rising channel, one can only be bullish on this pair. Indeed, if prices were to break above the psychological 2.0000 hurdle, there is not much further resistance seen until the resistance trend of the bullish channel or the 161.8% Fibonacci level at 2.0425, whichever comes first (depends on the speed of the potential rally). Thus, there is still further room to the upside even though rates are looking a little bit overbought.