GBP AUD More Sterling troubles vs Aussie

One central bank nears the end of its easing cycle, while the other is set to start a new wave of quantitative easing. The former […]

One central bank nears the end of its easing cycle, while the other is set to start a new wave of quantitative easing. The former […]

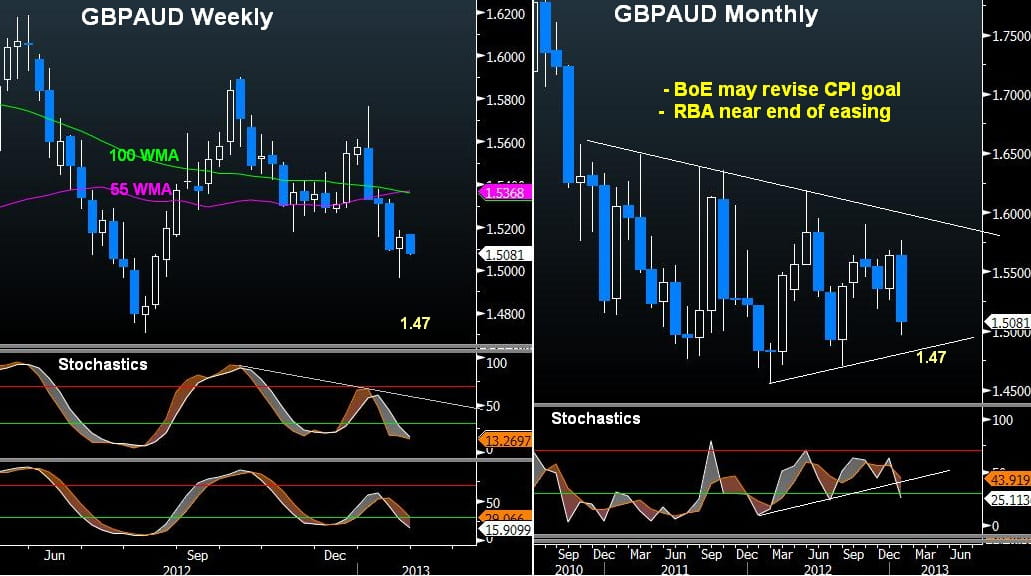

One central bank nears the end of its easing cycle, while the other is set to start a new wave of quantitative easing. The former may no longer worry about the spillover from a Chinese hard landing, while the latter is dealing with the fourth negative quarterly growth over the last six quarters. The first is none other than the Reserve Bank of Australia and the latter is the Bank of England.

The strength of the Aussie lies in its ability to remain underpinned above 1.02 during most of the last six months despite an aggressive easing campaign from May to December 2012. And the primary reason to the currency’s resilience is that the RBA’s easing was mainly aimed at reining Aussie strength, instead of stabilising macro fundamentals. Last year’s announcement by the IMF to include the Aussie in its reserve currency data dealt a sharp boost to the currency and confirmed what was already going on-global central banks had began accumulating the Aussie into their reserves as a safe alternative to the QE-driven currencies.

And even if there is a 35-40% chance of an RBA cut next month, Aussie macro metrics are not flashing any danger lights despite cooling off in copper and minerals resource. Thus, one last rate cut of 25-bps may well trigger a positive Aussie reaction was the case back in December when the easing by the same magnitude boosted the currency on the revelation that the RBA was moved by concerns of currency strength rather than the local of global macro picture.

Sterling’s recent woes are result of the renewed dip in growth, seen in Q4 GDP, which fell 0.3% after an Olympics-driven 0.9% jump in Q3. The Q3 recovery is especially suspected to be a result of special factors considering growth fell 0.4%, 0.2% and 0.3% in Q2 2012, Q1 2012 and Q4 2011. BoE governor Mervyn King (due to leave office in June) asserted the Bank was ready to provide more stimulus if needed. Those remarks were issued shortly after he responded to his successor-to-be Mark Carney, who has advocated targeting nominal GDP (growth minus inflation), seen as a possible attack on the BoE’s 16-year old policy of targeting inflation. Either way, FX markets can see through King’s pronouncements that he is in favour of further weakness in sterling rather than its appreciation.

Looking ahead, we expect further weakness in GBP/AUD, with the break below 1.49 expected by mid quarter, followed by further declines towards 1.47—the trendline support extending from last March. Any recovery is seen limited at 1.5220.