FX Analysis and Technical Outlook 8211 November 6th 2015

Key Economic Data Releases Next Week Tuesday (10 Nov): – AUD – NAB Business Confidence – CNY – China Consumer Price Index – CNY – […]

Key Economic Data Releases Next Week Tuesday (10 Nov): – AUD – NAB Business Confidence – CNY – China Consumer Price Index – CNY – […]

Key Economic Data Releases Next Week

Tuesday (10 Nov):

- AUD – NAB Business Confidence

- CNY – China Consumer Price Index

- CNY – China Producer Price Index

- GBP – UK Inflation Report Hearings

Wednesday (11 Nov):

- NZD – RBNZ Financial Stability Report

- NZD – RBNZ Governor Wheeler Speech

- CNY – China Industrial Production

- GBP – UK Average Earnings Index

- GBP – UK Claimant Count Change

- GBP – BOE Governor Carney Speech

- EUR – ECB President Draghi Speech

Thursday (12 Nov):

- AUD – Australian Employment Change

- AUD – Australian Unemployment Rate

- USD – US Unemployment Claims

- USD – FOMC Member Evans Speech

- USD – FOMC Member Dudley Speech

- CAD – US Crude Oil Inventories

Friday (13 Nov):

- EUR – German Preliminary GDP

- USD – US Core Retail Sales

- USD – US Retail Sales

- USD – US Producer Price Index

- USD – US Preliminary University of Michigan Consumer Sentiment

Technical Developments

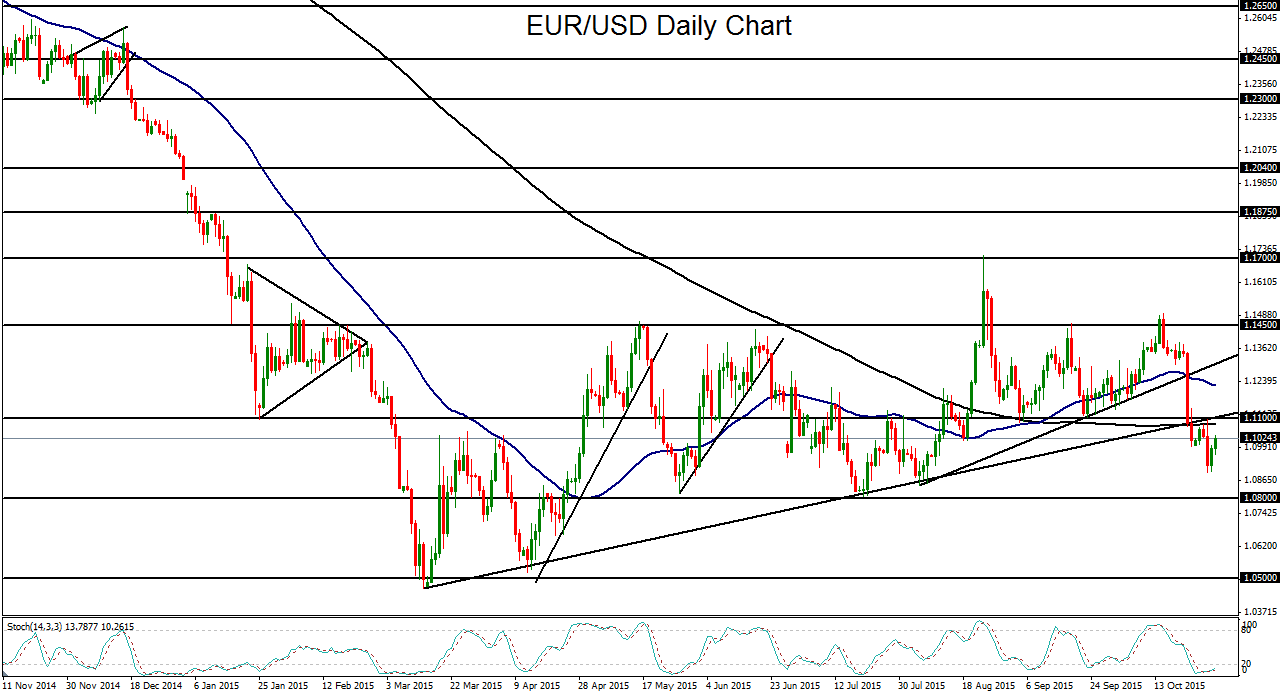

EUR/USD

EUR/USD has spent the past week trading well under key 1.1100 resistance and dropping towards its 1.0800 initial downside support target. The US Non-Farm Payrolls report on Friday, which showed a much better-than-expected number of jobs added for October, prompted the dollar to surge and the EUR/USD to plunge well below that 1.0800 target. This resumption of the bearish bias occurs after the currency pair broke down two weeks ago below a confluence of support at the noted 1.1100 level, the 200-day moving average, and a well-defined uptrend support line extending back to March’s 12-year low. After that breakdown, EUR/USD has respected that confluence of previous support factors, but now as resistance. With the 1.0800 downside support level now broken down, the outlook for EUR/USD has reverted once again to strongly bearish. If the currency pair sustains its breakdown below 1.0800, downside momentum could further pressure the currency pair towards its next major support target at 1.0500, which is the area of March’s multi-year lows.

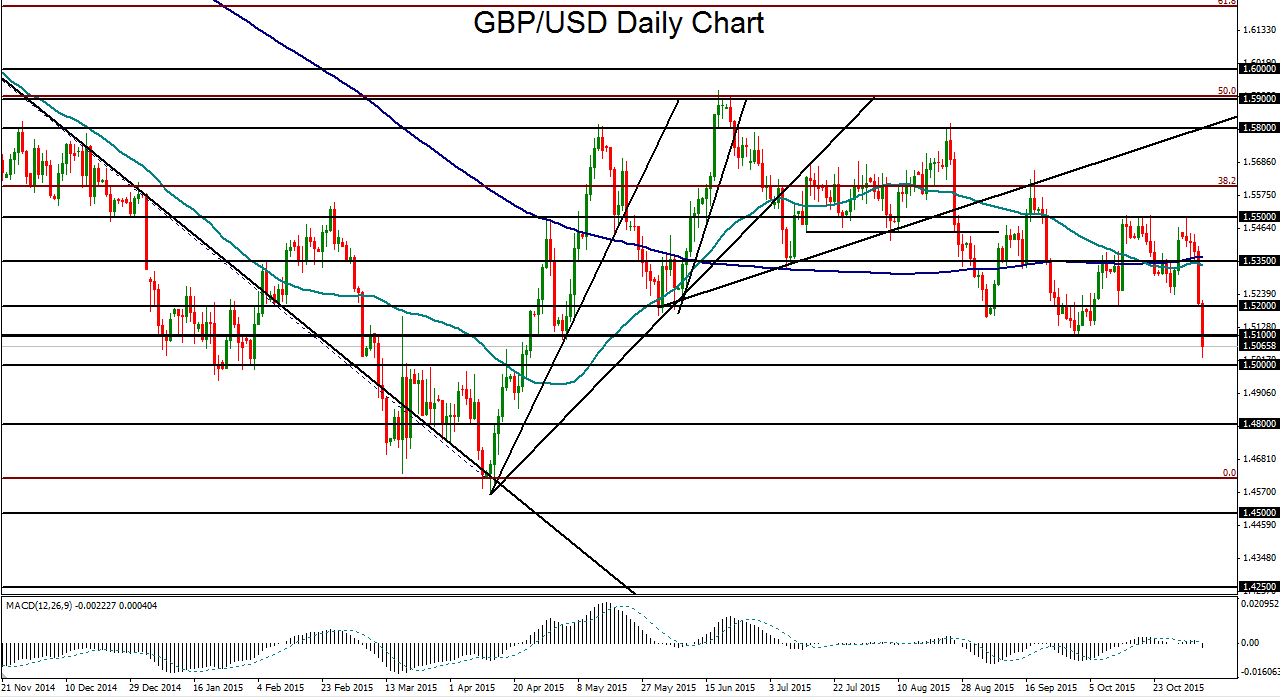

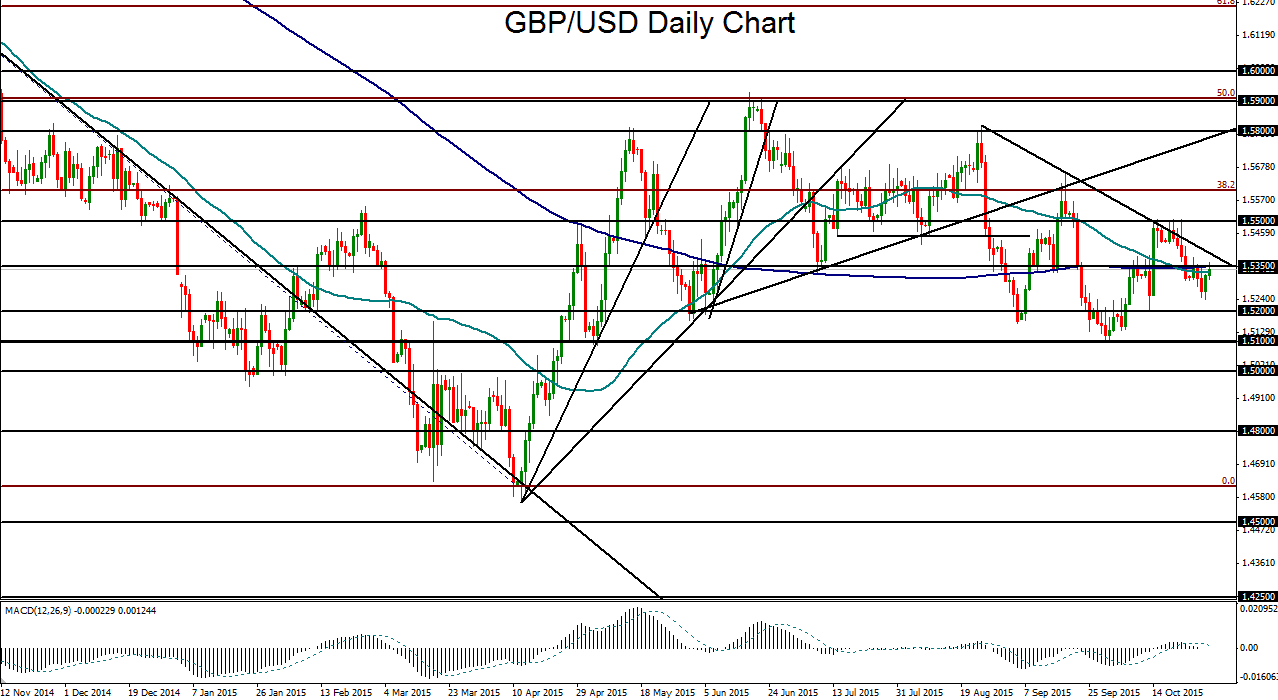

GBP/USD

GBP/USD plunged this past week from major resistance around the 1.5500 level down to its 1.5200 initial downside support target. In the process, price action broke down below key support around 1.5350, as well as both the 200-day and 50-day moving averages. After the US Non-Farm Payrolls report was released on Friday, a strengthened dollar prompted a further plunge for GBP/USD below its 1.5100 support target, where the currency pair bottomed out in early October, to approach the 1.5000 psychological support level. With this week’s dramatic slide, GBP/USD has strongly reasserted its bearish bias, especially in light of a relatively dovish Bank of England in contrast with a relatively hawkish US Federal Reserve. The next major target immediately to the downside is at the noted 1.5000 psychological level. With any break down below 1.5000, the next major downside target is at the 1.4800 support level.

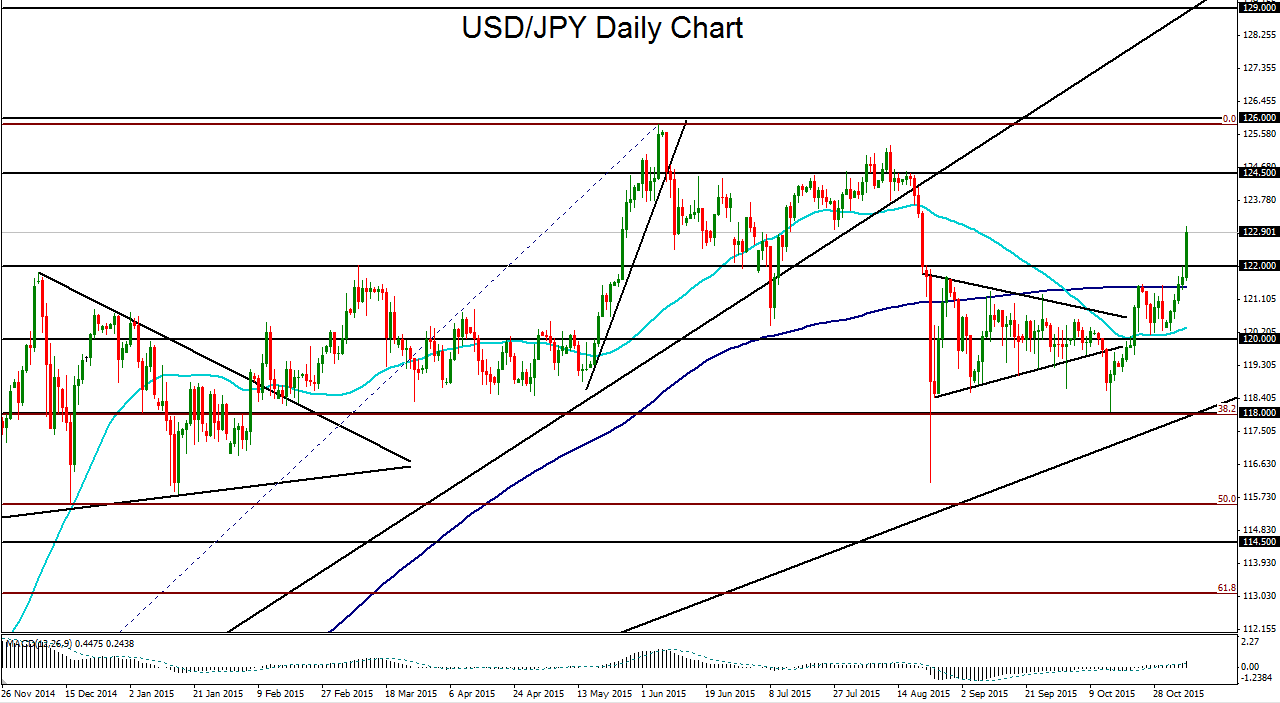

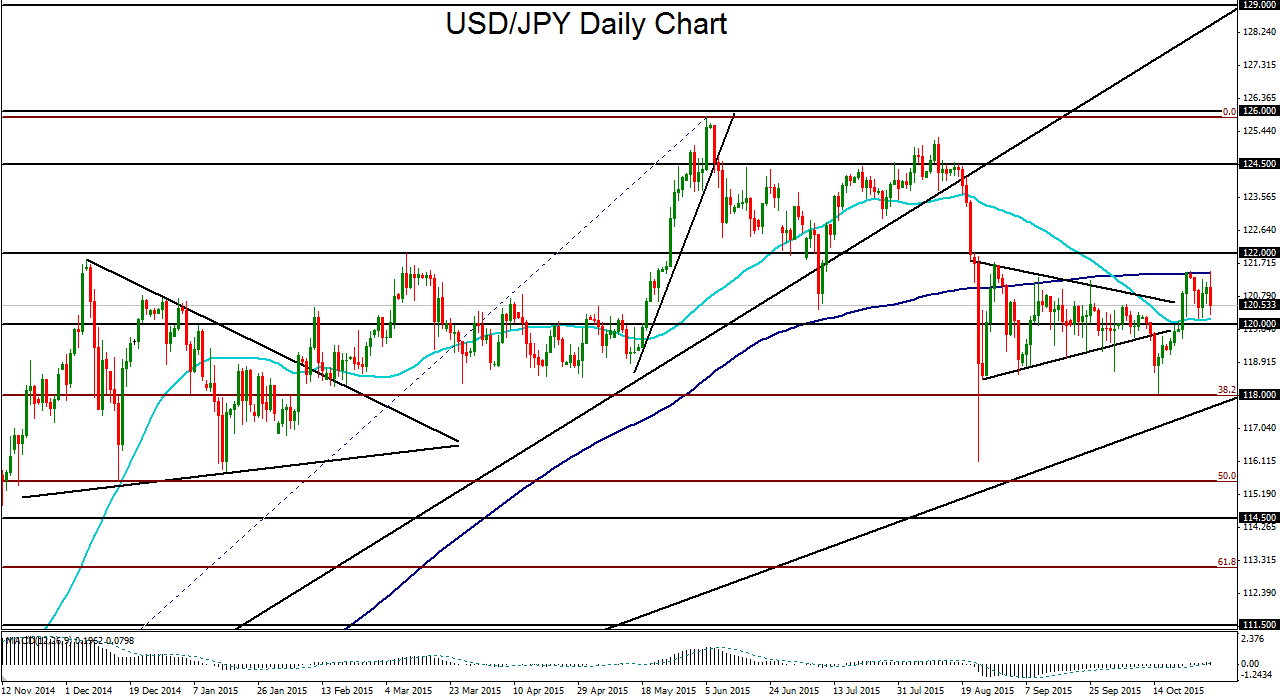

USD/JPY

USD/JPY rose sharply this past week on a rebound in the US dollar and lack of significant volatility in the equity markets. In the process, the currency pair broke out above its previous trading range between the 200-day and 50-day moving averages, and rose up to test major resistance around the 122.00 level. This rise was caused largely by increased speculation over a December rate hike by the Fed. The US Non-Farm Payrolls report on Friday prompted a forceful breakout above 122.00, reaching up to the 123.00 handle. Having made such a strong breakout, USD/JPY has risen to a critical juncture. With further upside momentum on renewed expectations of a Fed rate hike in December, the next major upside target is around the 125.00 resistance level. Tentative downside support after the breakout now resides at the noted 122.00 previous resistance level.

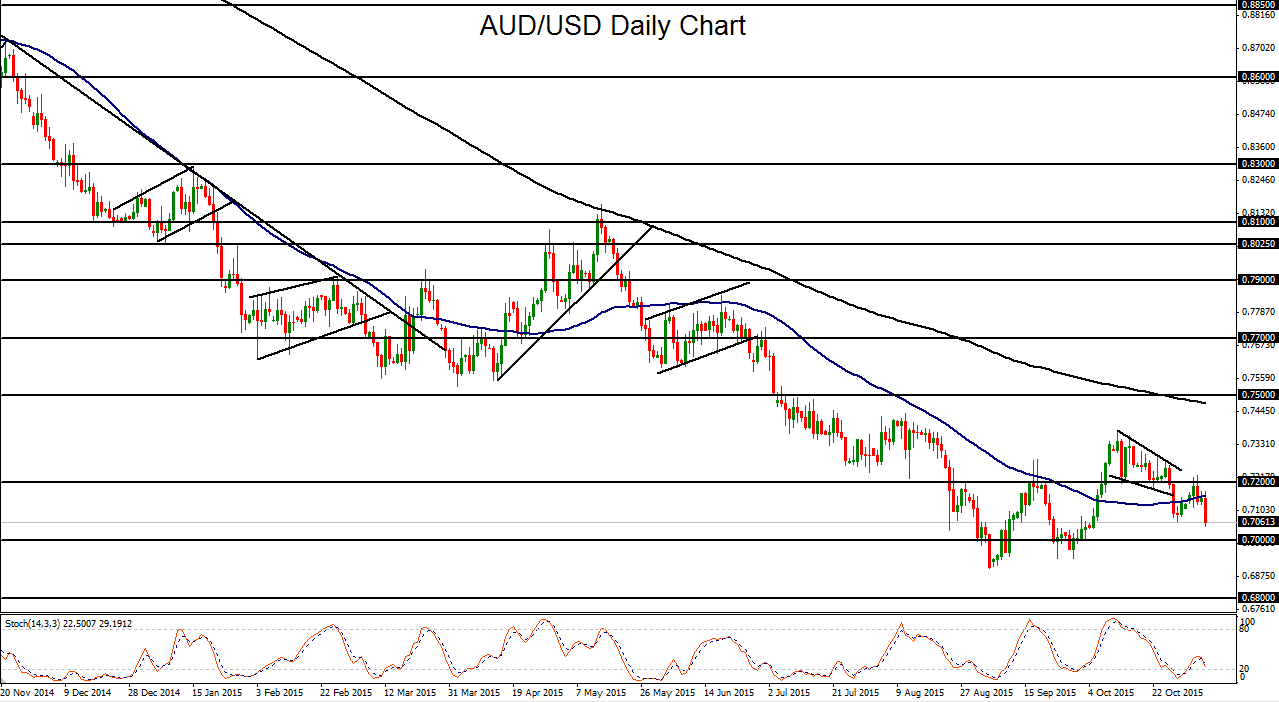

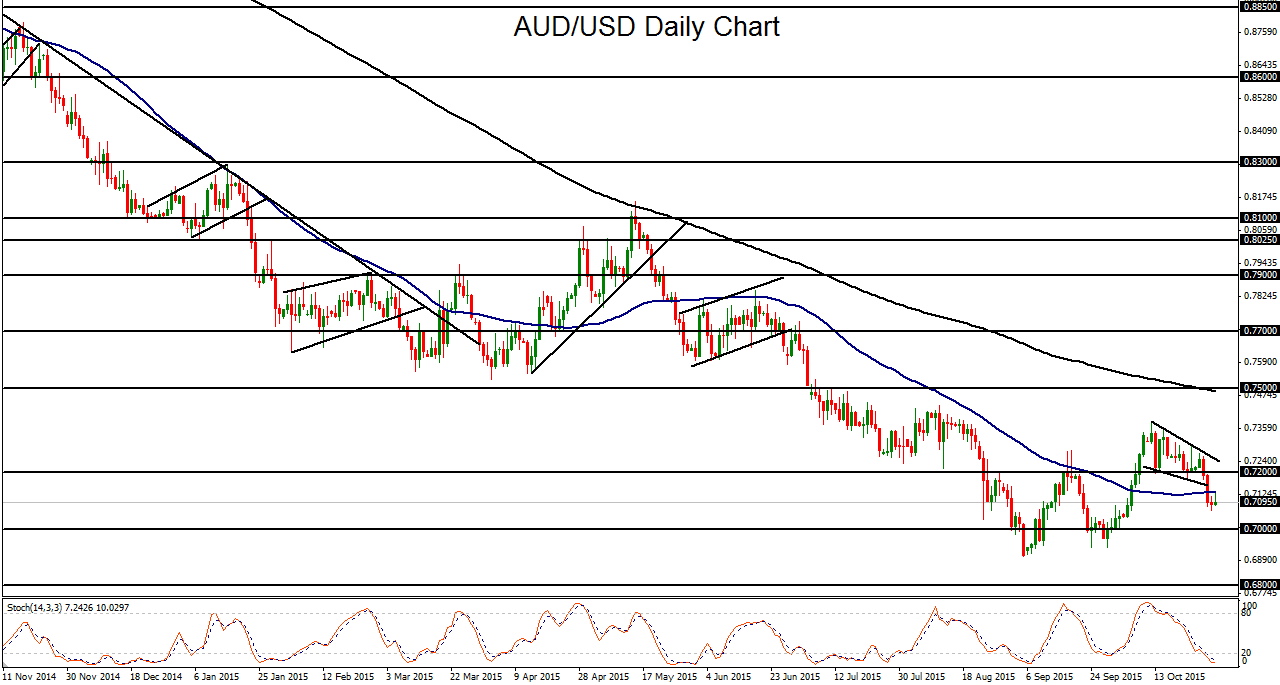

AUD/USD

AUD/USD continued to fluctuate under key 0.7200 resistance this past week as it continued to be weighed down by increased speculation over an impending Fed rate hike in the US as well as the specter of future interest rate cuts by the Reserve Bank of Australia. AUD/USD continues to be deeply entrenched within a sharp downtrend that has been in place for well more than a year, and the directional bias currently remains firmly to the downside. After the US Non-Farm Payrolls report release on Friday, AUD/USD hit a new one-month low on a strong US dollar. If the currency pair continues to trade under 0.7200, the next major downside targets immediately to the downside are at the 0.7000 psychological level followed by the 0.6800 support objective.

{kind=link}

{kind=link}

{kind=link}

{kind=link}