FX Analysis and Technical Outlook 8211 April 8th 2016

One of the major themes for this past week was that of mixed signals from government officials, which is arguably not an uncommon occurrence. Most […]

One of the major themes for this past week was that of mixed signals from government officials, which is arguably not an uncommon occurrence. Most […]

One of the major themes for this past week was that of mixed signals from government officials, which is arguably not an uncommon occurrence. Most notably, these signals emanated from the US Federal Reserve as well as major oil-producing nations.

On the Fed side, while this past week was not an action-packed one when it comes to economic data events, the widely-anticipated minutes of last month’s FOMC meeting were released. A primary takeaway from those minutes, however, was simply that there was much debate among Fed members over raising interest rates. The fact that there was even consideration by some members that a rate hike in April might be warranted and a distinct possibility, however unlikely, gave a slightly hawkish tone to the proceedings. At the same time, though, “a number” of policymakers urged caution due to global economic developments, which is nothing new for the Fed. Overall, the minutes appeared to skew towards the already-established dovish side, but did little to affect current speculation over the Fed’s next action, or inaction. As an immediate result of the release of last month’s meeting minutes, the US dollar fluctuated in a wide range but failed to find any clear direction, as it has generally drifted only modestly lower in subsequent days. Due to the fact that the Fed’s doves appear to significantly outweigh its hawks, however, pressure on the dollar is likely to be sustained further, at least for the time being.

Crude oil has also fallen victim to the vicious push and pull of mixed signals, most notably concerning the potential for a deal to limit oil output. Since the late January and early February lows, oil prices have rebounded dramatically, based largely upon hopes for such a deal to occur as well as declines in US oil production. Early in the week, however, it was reported that an apparent stumbling block had surfaced surrounding proposed negotiations among major OPEC nations and Russia to discuss the cap on crude production. Specifically, some OPEC nations, including Saudi Arabia, have found it difficult to accept a concerted output cap if Iran does not agree to participate. Of course, Iran is currently in the midst of aggressively ramping up its own oil production to make up for lost time and revenue after previous sanctions long imposed on the country were recently lifted. Later in the week, however, Russia continued to show optimism that a meeting to negotiate the deal, set for April 17th in Doha, Qatar, could potentially produce a successful agreement. Despite this optimism, Iran’s probable non-participation and Iraq’s high and increasing output levels could likely preclude such a deal from being struck. Overall, the negatives appear to outweigh the positives for crude oil prices, at least for the near term, and the recent rebound could begin to experience renewed pressure.

In terms of major macroeconomic events and data next week, the Consumer Price Index, a key inflation indicator, will be released in the UK on Tuesday. China will release its trade balance figures on its Wednesday morning, followed by the Producer Price Index and retail sales reports out of the US. Also on Wednesday, the Bank of Canada will issue its rate statement and monetary policy report, along with its usual press conference. Similarly, the Bank of England will release its official bank rate and monetary policy summary on Thursday. This will be followed on Thursday by the US Consumer Price Index and unemployment claims. Finally, on Friday in China, Chinese GDP and industrial production figures will be reported.

Technical Developments

EUR/USD

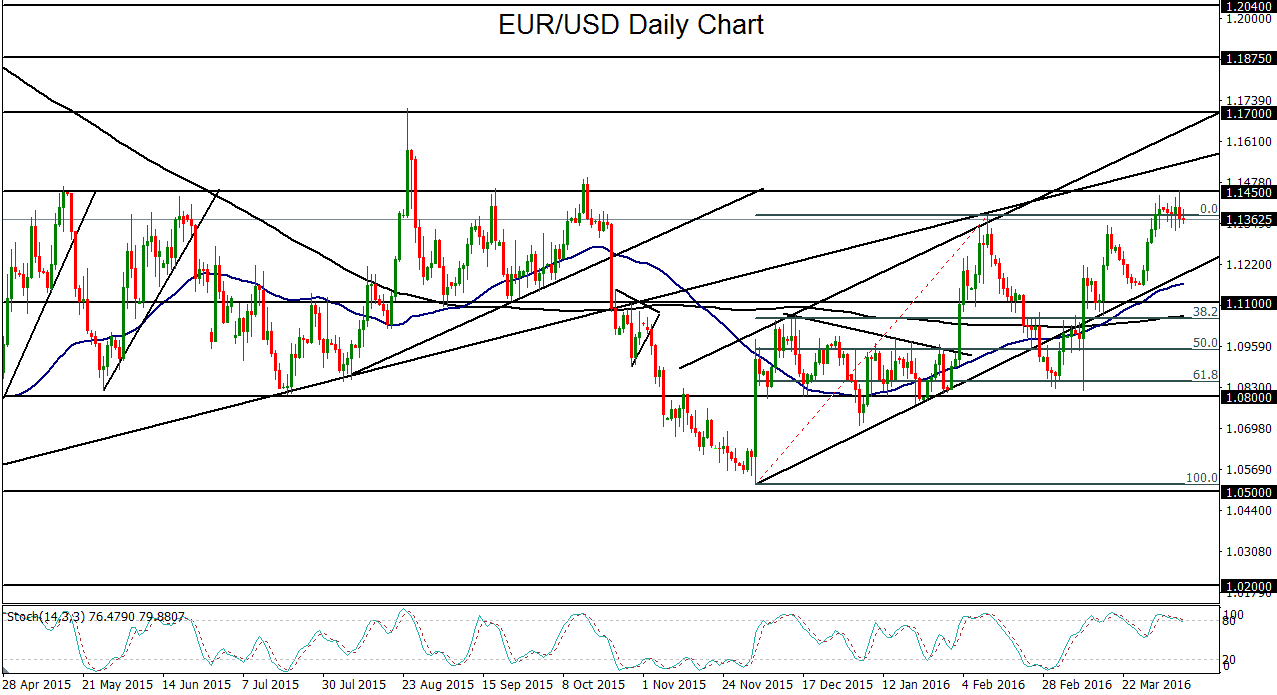

This past week saw a prolonged consolidation for EUR/USD up against major resistance around the 1.1450 area. This consolidation is the latest culmination of a rising trend characterized by higher highs and higher lows since December’s lows near 1.0500. During the course of this uptrend, the currency pair has broken out above major resistance areas, including the key 1.1100 level, largely as a result of a weakening of the US dollar. In mid-March, the 50-day moving average crossed above the 200-day moving average, suggesting a bullish outlook for the near term. Currently just off the noted key resistance level around 1.1450, EUR/USD is at a critical technical juncture. Any sustained breakout above this resistance could go on to target the next major upside target at the 1.1700 level, which was the area of the high reached in August 2015.

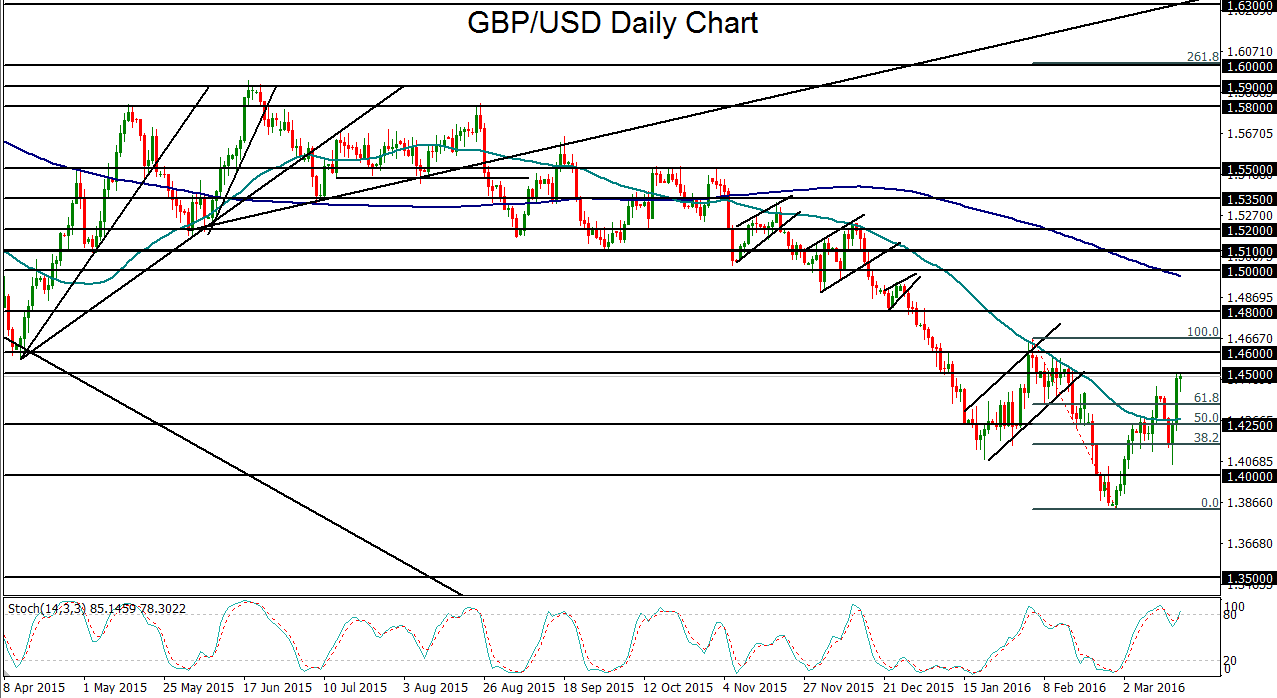

GBP/USD

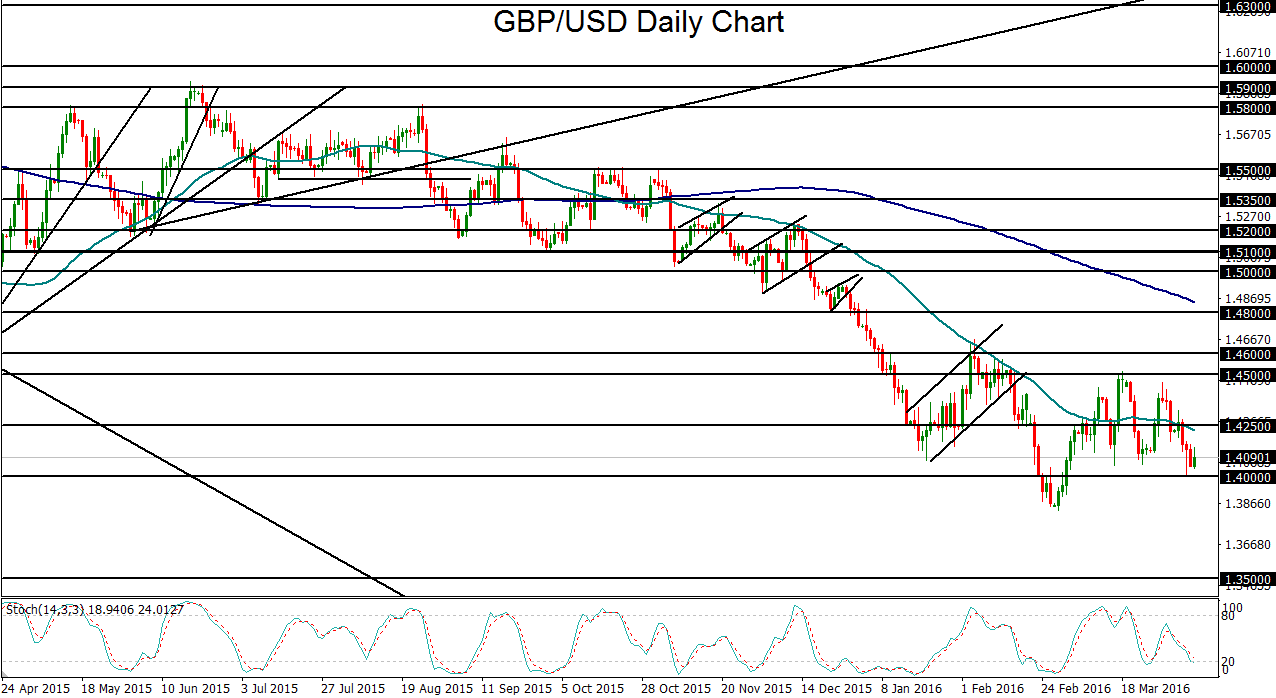

GBP/USD has continued to trade under pressure as of late. Sterling has fallen considerably against other major currencies, including the dollar, euro, and yen, due not only to a rather consistently dovish Bank of England, but also by a looming June referendum that draws ever closer, in which the UK will decide whether or not it will remain in the European Union. This pressure on GBP/USD has occurred despite general weakness in the US dollar, which suggests that the pound could have considerably further to fall in the run-up to the referendum. Recently, GBP/USD has continued to trade in a weakened state, consolidating not far above its near-7-year low below 1.4000 that was just established in late February. Next week, the Bank of England will announce its official bank rate and monetary policy summary. Although the central bank is not expected to change interest rates at that meeting, the policy summary will, as always, be scrutinized closely for any clues as to the bank’s stance on interest rates going forward. From a technical perspective, GBP/USD appears once again to be poised for an impending breakdown below the key 1.4000 psychological level. With any further breakdown below February’s multi-year low of 1.3835, a continuation of the long-term downtrend will have been confirmed, with the next major downside target considerably lower at the key 1.3500 support level.

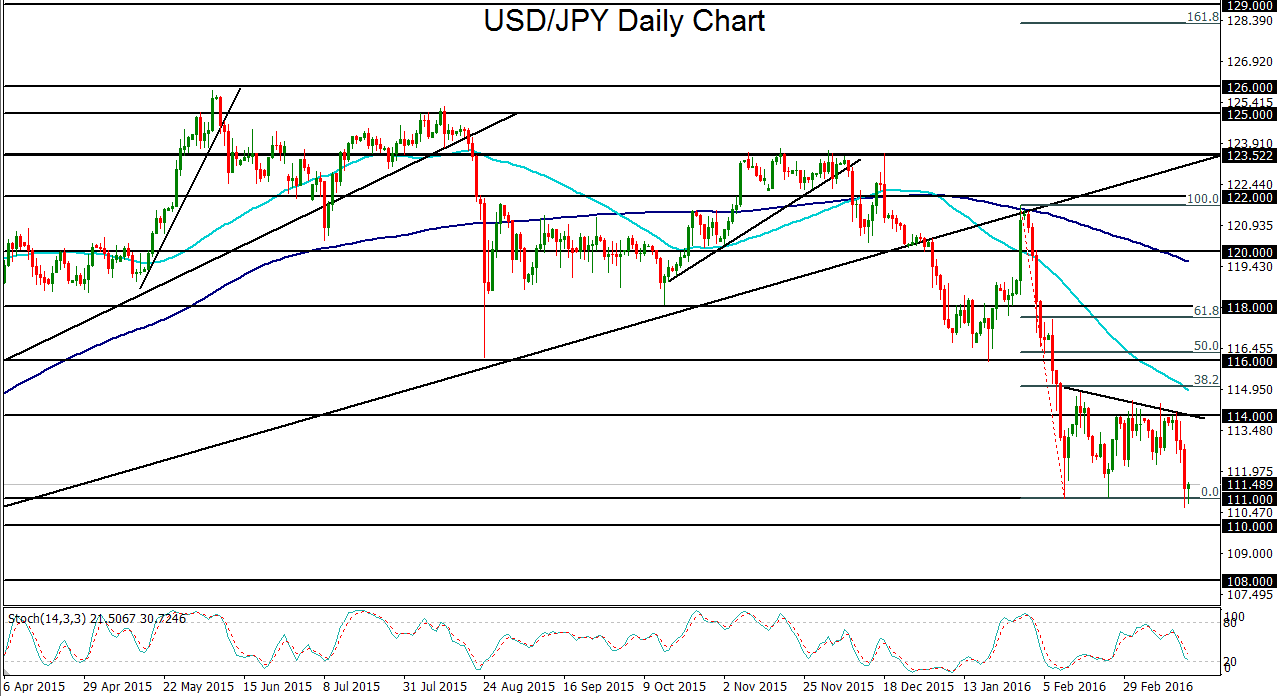

USD/JPY

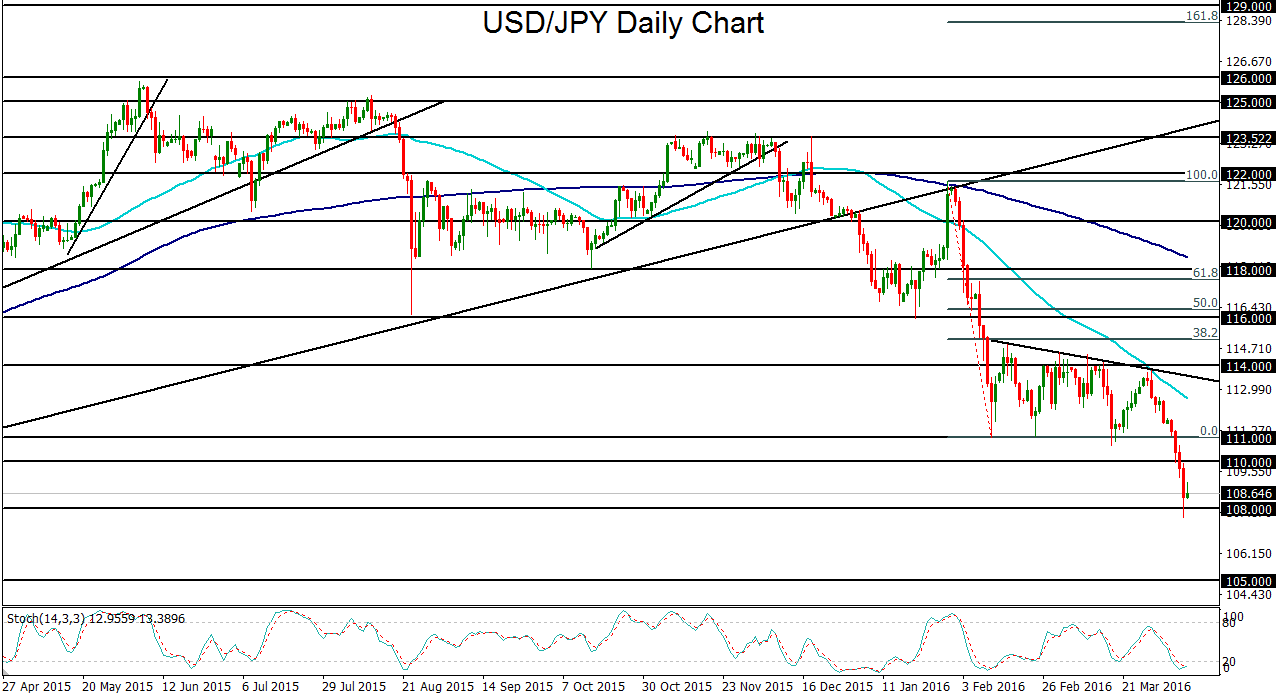

USD/JPY continued its plunge this past week, falling well below the 110.00 psychological level to hit a major downside support target at 108.00. In the process, the currency pair established a new 17-month low. USD/JPY’s sharp fall within the past week-and-a-half has been primarily because of weakness in the US dollar due to ongoing caution on the part of the Federal Reserve in hiking interest rates further, along with skepticism with regard to the Bank of Japan’s effectiveness in intervening to weaken the yen. This past Wednesday’s release of meeting minutes from last month’s FOMC meeting indicated debate among Fed members regarding the conditions for another rate hike, but highlighted the group’s persistent concern over weak economic growth, which will pose a major obstacle to raising interest rates further. The Fed’s continuing dovish stance on monetary policy have placed increasing pressure on the US dollar as of late. Although the surging yen has raised speculation that the Bank of Japan may soon intervene to weaken its currency, skepticism remains over the efficacy of the central bank’s attempts to do so, especially in light of its recent easing into negative interest rate territory, which had no lasting impact on restraining yen appreciation. After retreating from both its 50-day moving average and the upper border of a large descending triangle pattern, USD/JPY broke down below major support at 111.00 early this past week. After doing so, the currency pair quickly followed-through by dropping down to key psychological support at 110.00. Then, as previously noted, price action plunged further on Thursday to hit the major support target at 108.00. In the absence of a successful attempt by the Bank of Japan to intervene in the strong yen, a weakening dollar could push USD/JPY lower in the short-term. In the event of a sustained breakdown below the 108.00 level, the next major downside target is at the 105.00 support level.

{kind=link}

{kind=link}

{kind=link}