FX Analysis and Technical Outlook 8211 April 22nd 2016

Central Banks Take Center Stage For both this past week and the coming week, some of the world’s most prominent central banks are taking center […]

Central Banks Take Center Stage For both this past week and the coming week, some of the world’s most prominent central banks are taking center […]

Central Banks Take Center Stage

For both this past week and the coming week, some of the world’s most prominent central banks are taking center stage, issuing eagerly anticipated rate decisions and policy statements.

This past week, the European Central Bank (ECB) was in focus. Not much about the ECB’s public pronouncements on Thursday was unexpected. Interest rates remained unchanged this time, as anticipated, after the surprisingly aggressive easing actions presented at last month’s meeting. ECB President Mario Draghi struck an overall dovish tone, reiterating the need to address persistent conditions of low inflation and economic growth risk. At the same time, however, Draghi urged patience in the face of prolonged weakness in inflation, hinting that any further easing will need to wait. The press conference skewed towards the dovish side primarily because Draghi kept open the potential for lower rates, in contrast to last month’s conference, when he remarked that he did not expect interest rates to decline any further. As a result of the dovish, but somewhat mixed, messages from the ECB, the euro rode a volatile wave of market sentiment on Thursday. The currency initially surged due to the conspicuous absence of any rate changes or further easing measures, but then dropped abruptly during and after the press conference when it became clear that Draghi had become more dovish than he had been last month. Overall, the central bank gave little in the way of concrete guidance for the euro aside from some dovish-leaning nuances, but the currency continued to fall into the end of the week.

Shifting to Asia, the end of this week saw the Japanese yen plunge against other major currencies as reports surfaced that the Bank of Japan (BoJ) is considering potentially more aggressive easing actions in the form of additional stimulus measures. This would entail the implementation of negative lending rates to financial institutions in Japan. Though the yen immediately began to plummet as the market digested this information, it should be noted that a similar tumble for the Japanese currency occurred when the BoJ pushed interest rates into negative territory in late January. Immediately thereafter, however, the yen embarked on a period of major strengthening for the ensuing months. Therefore, the effectiveness of the BoJ’s easing tools and tactics has come into question. Could the yen once again shrug off the central bank’s attempts at restraining its rise? Next week brings the Bank of Japan’s highly anticipated monetary policy meeting and statement. Indeed, this past week’s reports of the BoJ’s plans for more easing has set the tone for higher expectations of action next week. The question still remains, however, as to what sustainable effect that might have on the yen.

This brings us to the most watched of major central banks, the US Federal Reserve. Next week brings the potentially pivotal policy decision and statement from the Fed, in the form of the FOMC Statement. The Fed is not expected to make any changes to interest rates at its meeting next week, as the US central bank has generally become increasingly dovish since its rate hike in December, but will provide its current outlook on the common concerns of low inflation and economic growth risks. At the current time, Fed Fund futures are pricing-in only around a 1% probability of a rate hike next week, although the probability of any rate hike by the end of the year increases dramatically to nearly 70%. Largely due to the Fed’s increasing dovishness since December, the US dollar has been weakening steadily for the past few months, despite the prevalence of increasing dovishness across most other major central banks as well. As always, next week’s statement will be scrutinized in minute detail for wording nuances that might indicate a dovish or hawkish bias. If the Fed continues its increasingly dovish progression, the dollar could extend its weakness of the past few months. Any signs of emerging hawkishness, however, could help to buck the downtrend.

To add onto the Fed on Wednesday and the BoJ on Thursday, next week will also feature the rate decision and statement from the Reserve Bank of New Zealand. Aside from the central banks, some other important economic events and data releases next week are as follows:

Monday – German IFO Business Climate (EUR), New Home Sales (USD)

Tuesday – Durable Goods Orders (USD), Core Durable Goods Orders (USD), CB Consumer Confidence (USD)

Wednesday – Consumer Price Index (AUD), Preliminary GDP (GBP), US Crude Oil Inventories (CAD)

Thursday – Advance GDP (USD), Unemployment Claims (USD)

Friday – GDP (CAD)

Technical Developments

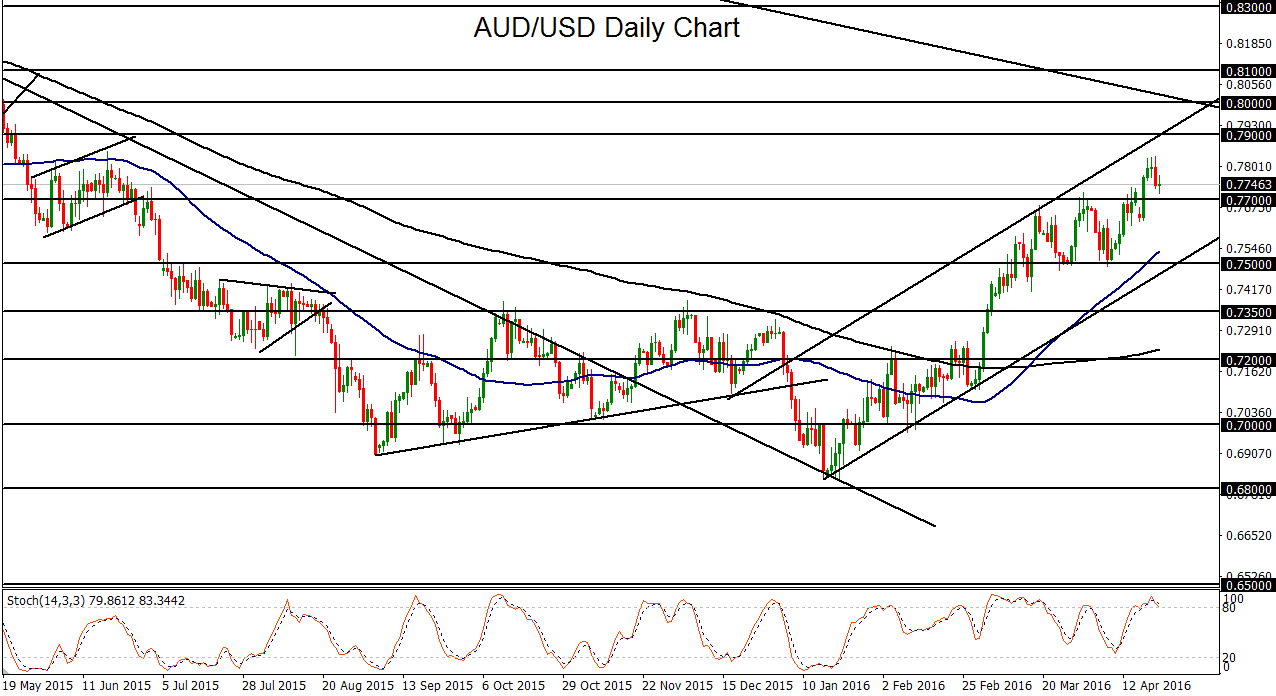

AUD/USD

A recent rebound in risk assets and commodity prices, as well as a weakening of the US dollar and relative stabilization in Asian markets (most notably China), have helped contribute to the AUD/USD rally from multi-year lows that has occurred within the past three months.

This sharp rally has boosted the currency pair from nearly a 7-year low just above 0.6800 in mid-January up to a 10-month high above 0.7800 just this past week. Within the course of this uptrend, AUD/USD has formed a rough rising channel that has broken out above progressively higher resistance levels, including the most recent breakout above 0.7700. That breakout occurred early this past week as the US dollar continued to stagnate and commodities remained supported.

Minutes from the Reserve Bank of Australia’s (RBA) most recent monetary policy meeting were also released early this past week. In those minutes, members showed concern for low wage growth in Australia, along with consistently low inflation. These factors, combined with the noted strengthening of the Australian dollar in recent months, could leave the door open for an interest rate cut by the central bank. The RBA next meets early next month, just over a week from now, to set the cash rate and provide a public rate statement. Although the central bank is not widely expected to change interest rates then, any further dovish leanings should be reflected by pressure on the Australian dollar.

As noted, the past three months have seen AUD/USD stage a sharp recovery. Most recently, this has resulted in a new 10-month high above 0.7800 in the latter half of the week after having broken out above the 0.7700 resistance level earlier in the week. Having done so, however, the currency pair has reached technically overbought levels. Major resistance factors reside directly above, including both the 0.7900 resistance level as well as the 0.8000 psychological level, which is also around the current position of a major downtrend line that extends back three years to 2013 highs.

With any turn back down due to a subsequent retreat in commodities and a potential resurgence of the US dollar, a re-break below the noted 0.7700 level could prompt an AUD/USD drop towards significantly lower levels. In this event, potential downside support targets are clearly defined at 0.7500 and 0.7350, followed by the key 0.7000 psychological level.

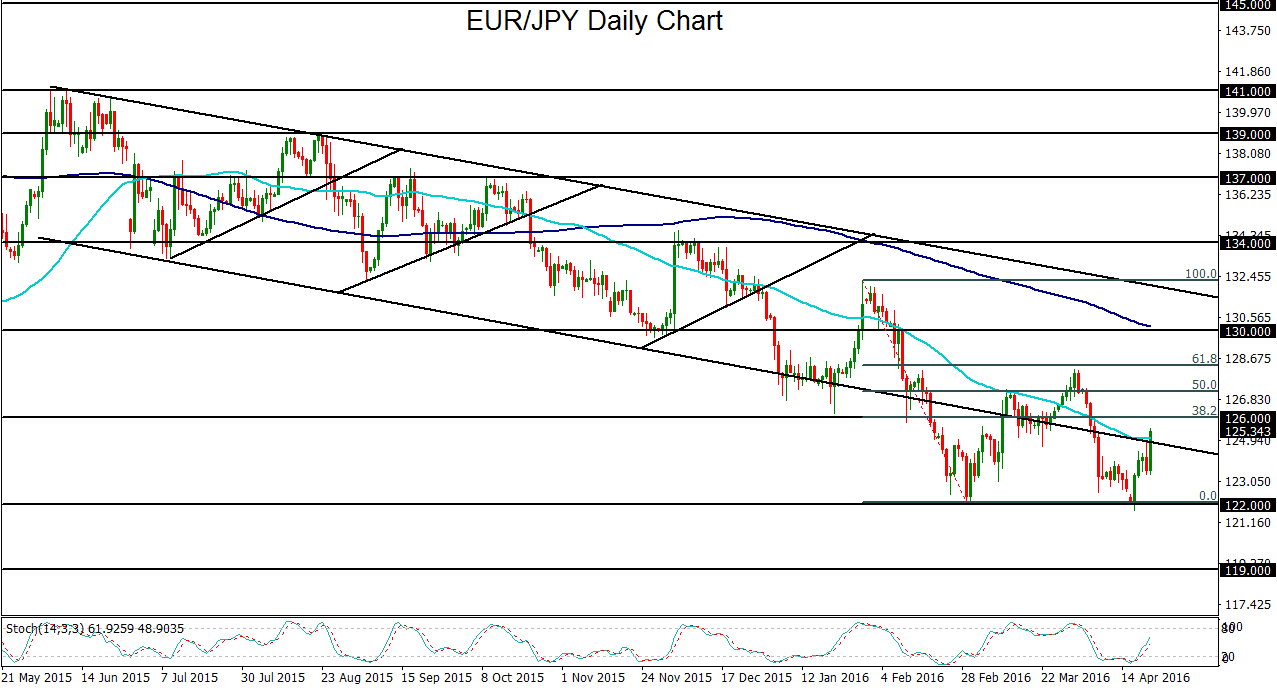

EUR/JPY

As a result of the dovish, but somewhat mixed, messages from the ECB this past week, the euro rode a volatile wave of market sentiment on Thursday. The currency initially surged but then dropped abruptly during and after the press conference when it became clear that Draghi had become more dovish than he was last month.

For EUR/JPY, this price movement was seen as a sharp rise to a two-week high of 124.95, where the 50-day moving average is currently situated, followed by an equally sharp drop that swiftly reversed those gains.

Despite continuing euro weakness on Friday, however, EUR/JPY surged due to reports that the Bank of Japan (BoJ) is considering potentially more aggressive easing actions in the form of additional stimulus measures. As a result, the yen plunged and EUR/JPY surged back up towards the 126.00 resistance level.

As it currently stands, however, EUR/JPY is still trading not far above its new 3-year low below key 122.00 support that was just hit early this week. That low formed a well-defined double-bottom in conjunction with the prior low at 122.00 that was hit in late February and early March.

While the yen plunged on Friday, the bullish trend for the Japanese currency has been strong within the last several months. Given the previous failed attempts by the Bank of Japan to weaken its currency through stimulus measures, the yen has the potential to continue its strength after the current pullback. In this event, a more dovish-leaning ECB combined with a rising yen could prompt a breakdown for EUR/JPY below major support at the noted 122.00 double-bottom level. If a sustained breakdown occurs, it would confirm a continuation of the longstanding downtrend for EUR/JPY, with the next major downside targets at the 120.00 psychological level followed by the key 119.00 support level.

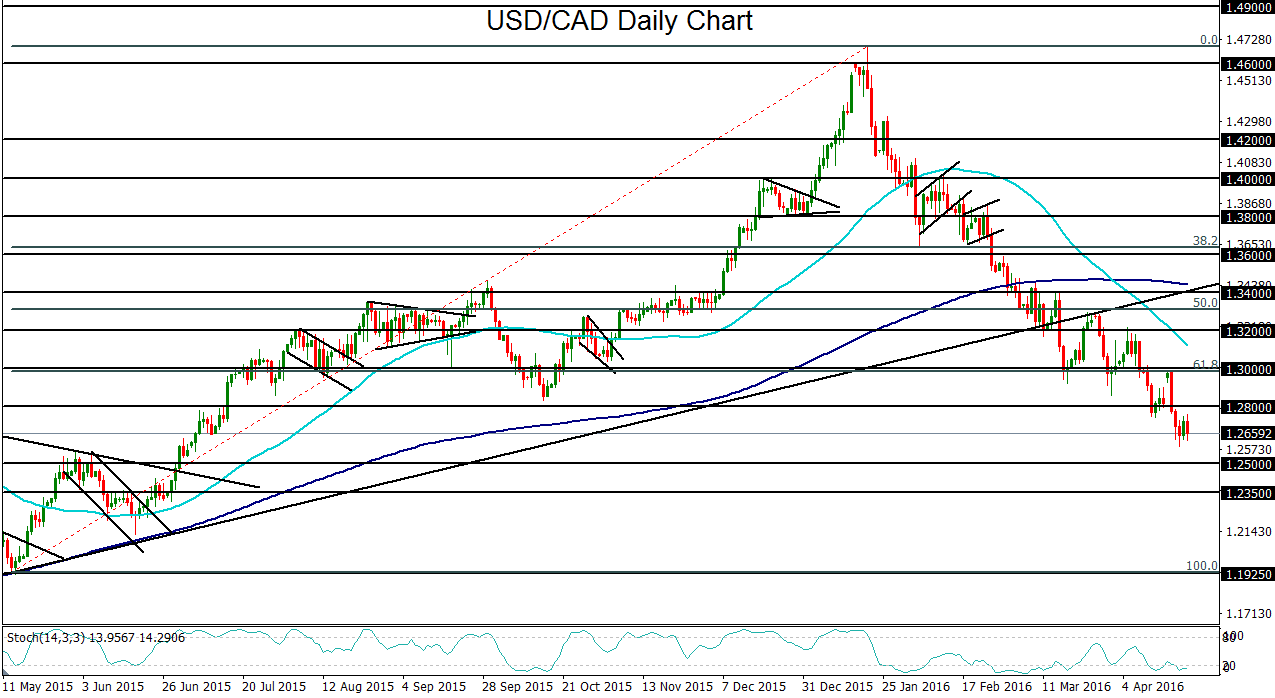

USD/CAD

USD/CAD turned down sharply from the key 1.3000 psychological resistance level this past week as crude oil prices rebounded, apparently shrugging off the opening plunge after last weekend’s failed oil deal meeting in Doha, Qatar. Initially, crude oil prices had gapped down significantly after news of the failure to strike a deal among major OPEC and non-OPEC countries was made public. Last Monday, however, saw oil prices close the gap as the benchmarks, WTI and Brent, both recovered much of their losses.

Prior to and following the oil meeting, the Canadian dollar closely mirrored price action on crude oil, as is typically the case due to Canada’s traditional economic reliance on oil-related exports. In the immediate run-up to the Qatar meeting and on news of the meeting’s results, the Canadian dollar fell sharply, boosting the USD/CAD currency pair back up to the key 1.3000 psychological level. On last Monday’s strong recovery in crude oil, however, the Canadian dollar closely followed suit, pressuring USD/CAD back down below the major 1.2800 support level.

The currency pair then followed through to the downside this past week to hit a new 9-month low below 1.2600. That low has been the latest culmination of a strong downtrend that has been in place since January’s long-term highs near 1.4700. This downtrend has largely resulted from the combination of a weakening US dollar and a strengthening Canadian dollar boosted by recovering crude oil prices within the past three months. During the course of the downtrend, USD/CAD has broken down below multiple key support factors, including the 1.4000 and noted 1.3000 psychological levels, as well as a major uptrend line that extends back to the lows of July 2014. Additionally, the 50-day moving average has crossed below the 200-day moving average in the past several weeks, forming a technical “death cross” and suggesting strong bearish momentum. On Friday, CPI inflation data and retail sales numbers both exceeded expectations, giving a further boost to the Canadian dollar. With any continued downside momentum below the 1.2800 level, the next major USD/CAD target to the downside is at the 1.2500 support level, which would confirm a continuation of the current three-month bearish trend.

{kind=link}

{kind=link}

{kind=link}