European bourses are heading lower in early trade on Monday as investors pause for breath after a phenomenal rally across the month of November. Some European benchmark indices have surged over 20% higher. The FTSE, which has reversed earlier losses

Vaccine optimism has driven risk appetite and stock markets higher across November. Over the past month Pfizer, Moderna and AstraZeneca have all revealed upbeat results from their clinical trials. A vaccine is the quickest and surest way for global growth to return to pre-pandemic levels.

News that the UK regulators could approve the Pfizer vaccine in the coming days is keeping optimism surrounding UK stocks buoyant. The FTSE is outperforming its European peers, pushing into positive territory.

JD Sports is a clear winner, topping the as investors cheer the athleisure retailer stepping back from talks with Debenhams. JD Sports jumps 6.7%, even as trouble on the high street brews.

Oil drops 1%, oil majors decline

Oil stocks are the biggest drag on the FTSE with the likes of BP and Royal Dutch Shell – over 2%, tracing the commodity lower. Oil has dropped almost 1% after an informal OPEC meeting on Sunday revealed that divisions remains over whether to extend production cuts beyond January. The group will meet today to hammer out plans for output in the new year, failure for the group to agree a new deal means that the originally planned output increase of 2 million more barrels a day will come into effect.

Oil stocks are the biggest drag on the FTSE with the likes of BP and Royal Dutch Shell – over 2%, tracing the commodity lower. Oil has dropped almost 1% after an informal OPEC meeting on Sunday revealed that divisions remains over whether to extend production cuts beyond January. The group will meet today to hammer out plans for output in the new year, failure for the group to agree a new deal means that the originally planned output increase of 2 million more barrels a day will come into effect.

Gold has lost its shine

As risk sentiment rose across the previous week a demand for stocks rose, safe haven Gold fell out of favour, closing below its 200 day moving average for the first time since January in an ominous sign. Precious metal miner Fresnillo is under pressure down 3.4% in the first hour of trading.

As risk sentiment rose across the previous week a demand for stocks rose, safe haven Gold fell out of favour, closing below its 200 day moving average for the first time since January in an ominous sign. Precious metal miner Fresnillo is under pressure down 3.4% in the first hour of trading.

Coming up

Looking ahead, UK mortgage approvals will keep house builders in focus. Approvals have been particularly strong across recent months as prospective buyers look to take advantage of the government’s stamp duty holiday scheme, which is set to run until March.

German inflation data is also due later. Expectations are for inflation to remain subdued in disinflation as the Eurozone’s largest economy extends its lockdown until 20th December.

Looking ahead, UK mortgage approvals will keep house builders in focus. Approvals have been particularly strong across recent months as prospective buyers look to take advantage of the government’s stamp duty holiday scheme, which is set to run until March.

German inflation data is also due later. Expectations are for inflation to remain subdued in disinflation as the Eurozone’s largest economy extends its lockdown until 20th December.

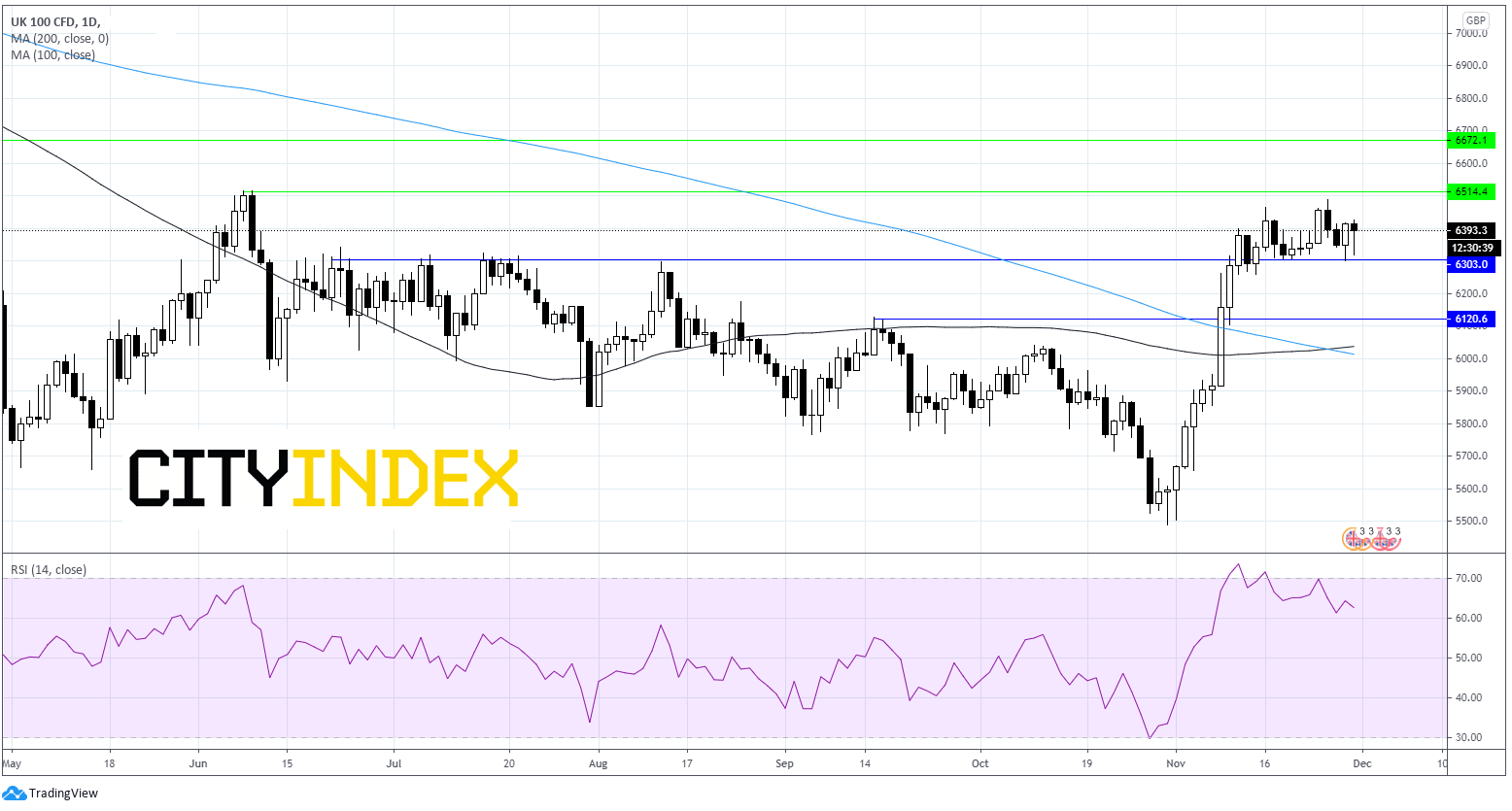

FTSE Chart

The FTSE continues to consolidate in the horizontal channel 6300 – 6515. The index rebounded off the lower band of the channel at the end of last week and is heading back towards the upper band at 6515. A break above this level could see the FTSE advance to 6670 a level last seen in March. On the flip side immediate a break through 6300 could open the door to horizontal support at 6120 prior to 200 day moving average and psychological support at 6000.

Latest market news

Today 04:47 AM

Yesterday 11:23 PM

Yesterday 10:19 PM

Yesterday 08:00 PM

Yesterday 04:54 PM

Latest Indices articles

Yesterday 08:00 PM

Yesterday 04:54 PM

April 15, 2024 06:08 AM

April 14, 2024 04:00 AM