FTSE Stocks end losing run as focus shifts to Fed

European stock markets and US index futures are sharply higher today, extending the gains from Monday afternoon’s bounce which saw Wall Street end the recent […]

European stock markets and US index futures are sharply higher today, extending the gains from Monday afternoon’s bounce which saw Wall Street end the recent […]

European stock markets and US index futures are sharply higher today, extending the gains from Monday afternoon’s bounce which saw Wall Street end the recent streak of losses. Here, the FTSE is breaking an eight-day losing run, thanks in part to rising share prices of supermarkets and as miners and energy stocks recover along with crude prices. Supermarkets are finding support in anticipation of bumper sales leading up to Christmas and on news that Sainsbury’s market share has increased. Crude prices are up for a second day, possibly because of short-covering after both oil contracts fell near their December 2008 lows on Monday. Thus, there is the danger that another round of selling could be on the way for crude once the buying pressure fades, because fundamentally nothing has changed. But for now, traders may correspondingly be trimming their bearish bets on oil companies, which could be helping to put additional upward pressure on the major indices like the FTSE. December is usually a positive month for the stock markets anyway, possibly because of the effect of ‘window dressing’ as money managers buy stocks that have been trending strongly in order to show off to their clients that they are holding the ‘correct’ type of stocks. Although this particular December is looking anything but strong, we are only at mid-way point. So, there is still plenty of time for the so-far elusive Santa Clause rally to start.

So far this week however, investors have largely been sitting on their hands, possibly because of the imminent rate decision from the US Federal Reserve on Wednesday. The market is widely expecting a small rate increase, accompanied by assurance that further rate rises will only take place if the incoming data shows the world’s largest economy is on a sustainable path of growth and that inflation is moving towards the Fed’s 2% target. But if the Fed surprises then the stock and other financial markets could move sharply. If it decides to keep its policy unchanged, which is unlikely in our view because its credibility in on the line, then stocks may initially rally on relief that interest rates will remain low for longer. On the other hand, if the Fed delivers a particularly hawkish message with a bigger-than-expected rate rise then that would probably not be good news for US and global stocks. Anything in-between is likely to be neutral to slightly positive for the markets.

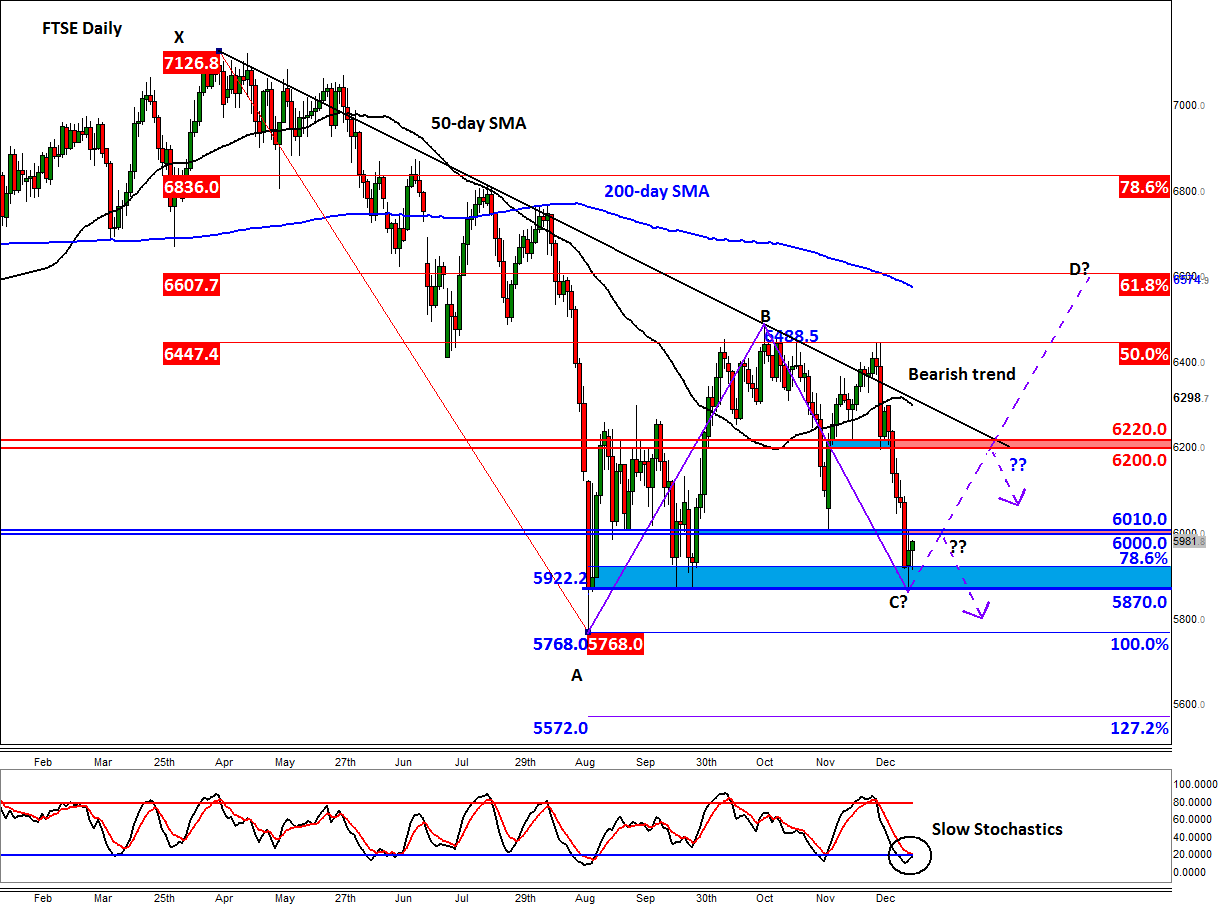

Technical outlook: FTSE

On Monday the FTSE dipped to the key support zone in the range between 5870 and 5920. This area had previously been support and corresponds with the 78.6% Fibonacci retracement against the bounce from August. At this stage however it is not clear if a base has been formed, given that the index was looking oversold anyway and short-side traders were likely to book some profit ahead of this week’s key fundamental event (i.e. Federal Reserve rate decision). The index still needs to clear key short-term resistance around the 6000-10 range if we are to see a more pronounced rally later this afternoon or tomorrow. Failure to do so would mean a small oversold bounce, potentially leading to another significant drop. But if does clear this resistance range, then there is little further short-term resistance until the 6200/20 range. This is also roughly where a bearish trend line that has been in place since April comes in to play. Thus a potential break above this key area could lead to an eventual rally, which could see the index climb all the way to the 200-day moving average at 6575 or the long-term 61.8% Fibonacci level at 6605/10.