FTSE stable as investor focus shifts from China to US

The FTSE managed to bounce back this morning alongside the wider European stock markets after renewed concerns about China, the world’s second largest economy, had […]

The FTSE managed to bounce back this morning alongside the wider European stock markets after renewed concerns about China, the world’s second largest economy, had […]

The FTSE managed to bounce back this morning alongside the wider European stock markets after renewed concerns about China, the world’s second largest economy, had weighed heavily on the stocks markets on Tuesday. Traders took profit on their short positions that had been opened the previous day and bargain hunters picked up mining stocks while Ashtead Group, which hires out industrial equipment, gained in excess of 5 per cent thanks to a record profit in the three months to July. But by midday in London, the major indices had relinquished their earlier gains and US index futures were pointing to only small rise at the open on Wall Street. As the Chinese markets will be closed for the remainder of this week as China commemorates the 70th anniversary of the end of World War II, investors will sharpen their focus on the health of the world’s largest economy, the US. We will have some very important employment and services data out this week which should provide us a good clue in terms of when to expect a rate hike from the Federal Reserve. As a small rate increase looks inevitable at some point later this year anyway, the stock market bulls will want to see some good macroeconomic numbers from the US economy, which have been lacking of late. If seen, this could revive recovery hopes and should boost the sentiment. Conversely, if the data fails to cheer then stocks could extend their declines even if it means rates will be held at record low levels for even longer than has been expected.

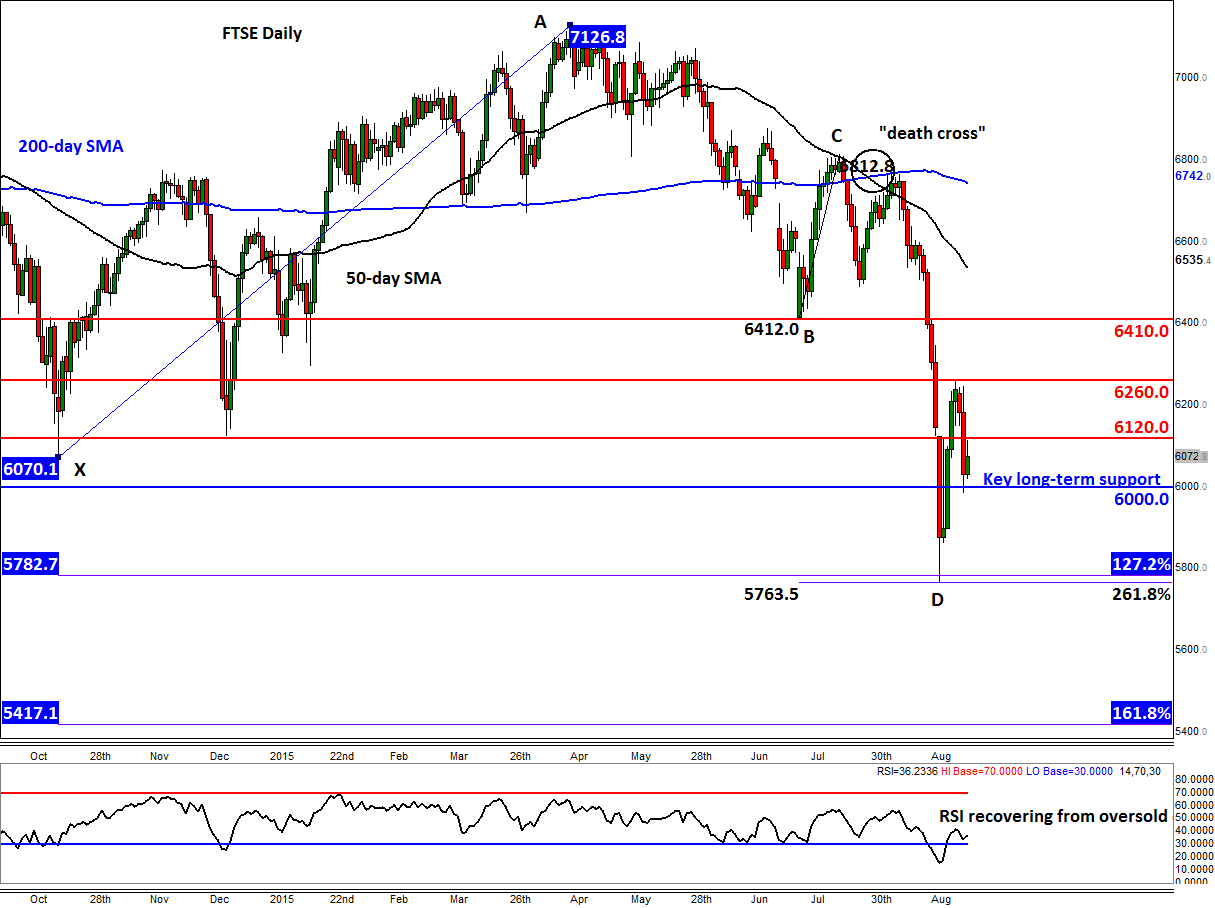

After a vicious sell-off that started from around 6600 in mid-August, the index dropped 800 points in subsequent days before finding strong support at 5765/85 (point D). This area corresponds with the Fibonacci extension levels of the previous couple of price swings (i.e. the 127.2% extension of XA and 261.8% extension of BC). Given that this area represents an exhaustion point and the manner in which the index had dropped, the resulting rally looks to have been mainly due to short covering rather than fresh buying. If this view is correct then the shorts may have established fresh positions following the kick-back rally that began early last week and that more of the existing longs probably exited their trades. In other words, we could see another sharp sell-off if the bears win back control and take out the key 6000 level again.

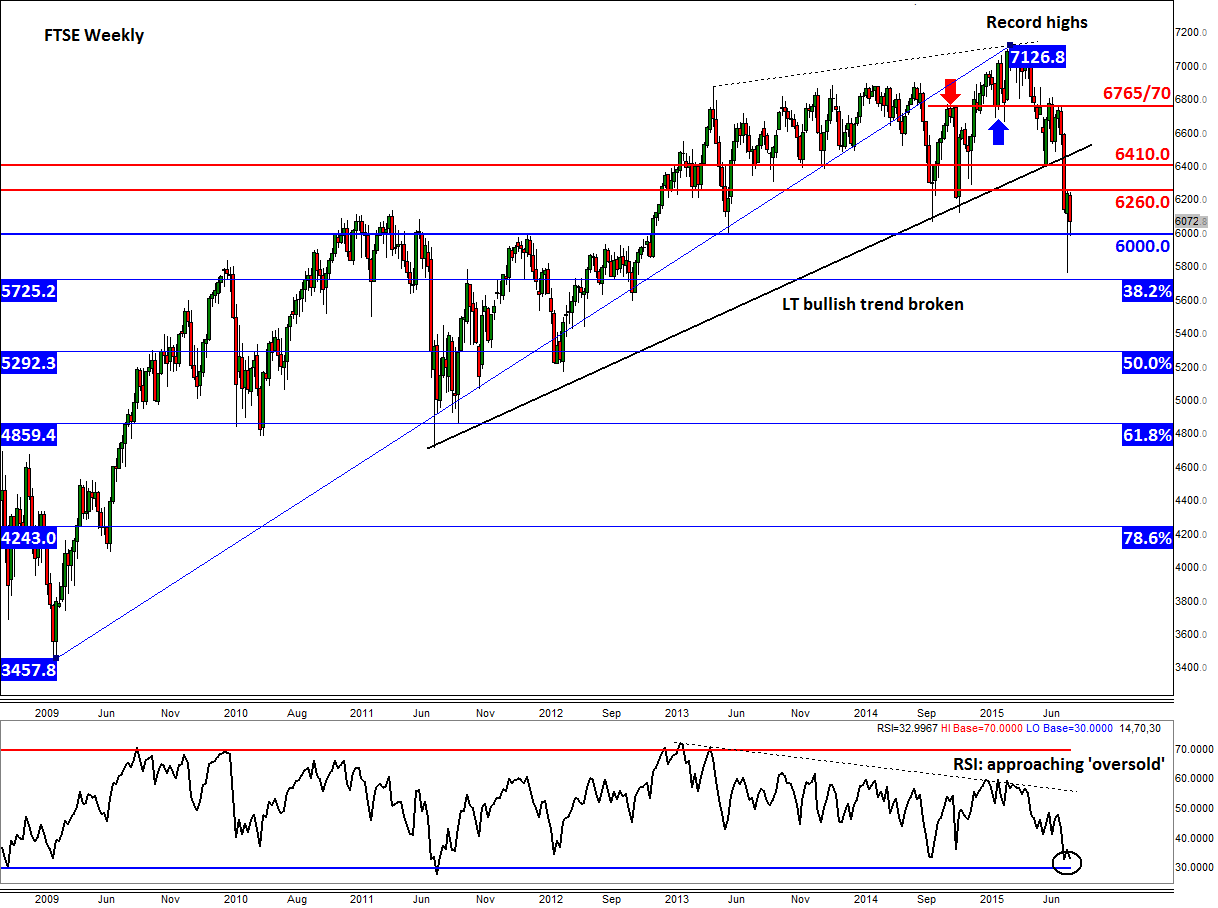

Indeed, the near-term direction of the FTSE may depend on what it does around this key long-term support at 6000. As can be seen from the daily and weekly charts, below, the index slipped through this handle on Monday of last week, before recovering strongly to finish the week higher.

A decisive break below the 6000 level could see the FTSE at least revisit last week’s low around 5670. If it also breaks below this level then it could possibly drop to its long-term 38.2% Fibonacci retracement level at 5725 (see weekly chart) or even the 161.8% extension of the corrective up move from the October low (i.e. XA swing on the daily chart) at just below 5420, before deciding on its next move.

Meanwhile the bulls will want to see a decisive break above last week’s high of 6260 in order to confirm the potential reversal pattern that we saw on the weekly chart – a bullish hammer candle – last week. If it does break above 6260 then the next target for the bulls could be the previous support at 6410 or the back side of the broken trend line around 6500.