FTSE shows signs of strength despite not so Super Thursday

Rio Tinto, BHP Billiton, Antofagasta lined-up at the bottom of the FTSE 100 index on Thursday after many had been the top gainers a day […]

Rio Tinto, BHP Billiton, Antofagasta lined-up at the bottom of the FTSE 100 index on Thursday after many had been the top gainers a day […]

Rio Tinto, BHP Billiton, Antofagasta lined-up at the bottom of the FTSE 100 index on Thursday after many had been the top gainers a day ago, before the Bank of England grabbed the day’s agenda, with moderately unexpected results.

The benchmark index was led by more defensive names on Thursday with Old Mutual at the top with a 5% gain, for most of the session, after the South Africa-focused life insurer reported a 20% rise in H1 operating profit.

The stock was having its best day for two months and its biggest jump in a day since December 2014.

OM’s peer Aviva also reported stronger half-year operating profit, helped largely by general and life insurance.

Insurance sector peers Legal & General, Prudential and Standard Life, also rose in the wake of their rivals’ earnings.

The FTSE 350 insurance sector index was 1.5% higher.

However the contribution from the broad ‘Financials’ segment to the entire FTSE index was little over 1.5 points, as all of the banks in the list dragged.

Banks were the stocks that showed the biggest negative reaction to a barrage of releases and a press conference by the Bank of England, that was somehow dubbed ‘Super Thursday’.

In the end, whilst these events drew much market attention, they revealed few divergences from the baseline of the BoE’s monetary policy.

The updates were most notable for producing one new dissenter on the BoE’s monetary policy committee, whilst most economists polled by financial data providers like Thomson Reuters had been expecting two.

Additionally, the central bank provided a more nuanced forecast of its view of inflation, moderately marking down its expectation of when there would be a pick-up in the key consumer price index reading, which now sits at zero.

Aberdeen Asset Management and Standard Chartered were the weakest financial stocks on the day down 2.8% and 3.3% respectively.

Shares of the latter had risen strongly for much of the day before after StanChart reported a deep fall in half-year profits, but held off from immediately raising capital as some investors had feared, whilst its earnings were largely in-line.

Aberdeen continues to experience outflows from emerging-market funds on worries related to a potential looming interest rate rise in the States, which could harm emerging market currencies.

The prospect of continued low interest rates also boosted rate-sensitive sectors like housebuilders and property-related stocks.

Housebuilder Taylor Wimpey rose 3.1%, making it one of the best-performers on the FTSE 100 and taking it to a new eight-year high.

Barratt Developments rose 2.3%, also hitting its highest level since 2007.

Persimmon rose 2% to a record high.

Whilst a modulation in prospects for a rise in UK interest rates could rekindle hopes for the benefits of lower borrowing c0sts, heavier-weighted mining stocks were a bigger influence on the market on Thursday, and they have reverted to drag mode.

It’s a correction reflex as many of these stocks had been top FTSE gainers a day ago.

Anglo American, BHP Billiton, Glencore, and Antofagasta traded between 3.5% and 5% lower.

Whilst investors have begun to accept that stock price downside of these and other miners is not inviolably tied to the price of the commodities they produce, their shares will inevitably maintain the highest delta to metals prices.

This is especially so as there’s no sign to an end of weak demand for industrial metals by their biggest consumer, China.

As evidence of economic slowdown there continues to mount, prices for metals like iron ore and copper are likely to keep falling for the foreseeable future.

Additionally, supply in some key commodities is still rising, increasing the risk that dividends at firms below the size of Glencore, BHP and Rio, will come under pressure.

This has not been seen at the largest FTSE miners, like Rio, which on Thursday reported an in-line 43% drop in half-year earnings.

Rio lifted its interim dividend by 12% to $1.075 per share, keeping to board policy.

But whilst share prices of the Big 3 may now have largely priced-in investors’ worst fears (all are around 20% lower since May) it’s clear their stocks are permanently sensitised to metal prices, economies like China and those of other industrializing nations.

Therefore it looks the resources sector in general, including ‘Supermajor’ oil multinationals like BP—which was 3.5% lower—could contain the FTSE 100’s progress for the remainder of the month at least.

The drop off in volume and volatility from the summer holiday season will also play a part.

However, further out, the arguments for the FTSE to revert to historic strength it showed earlier in 2015 are mounting.

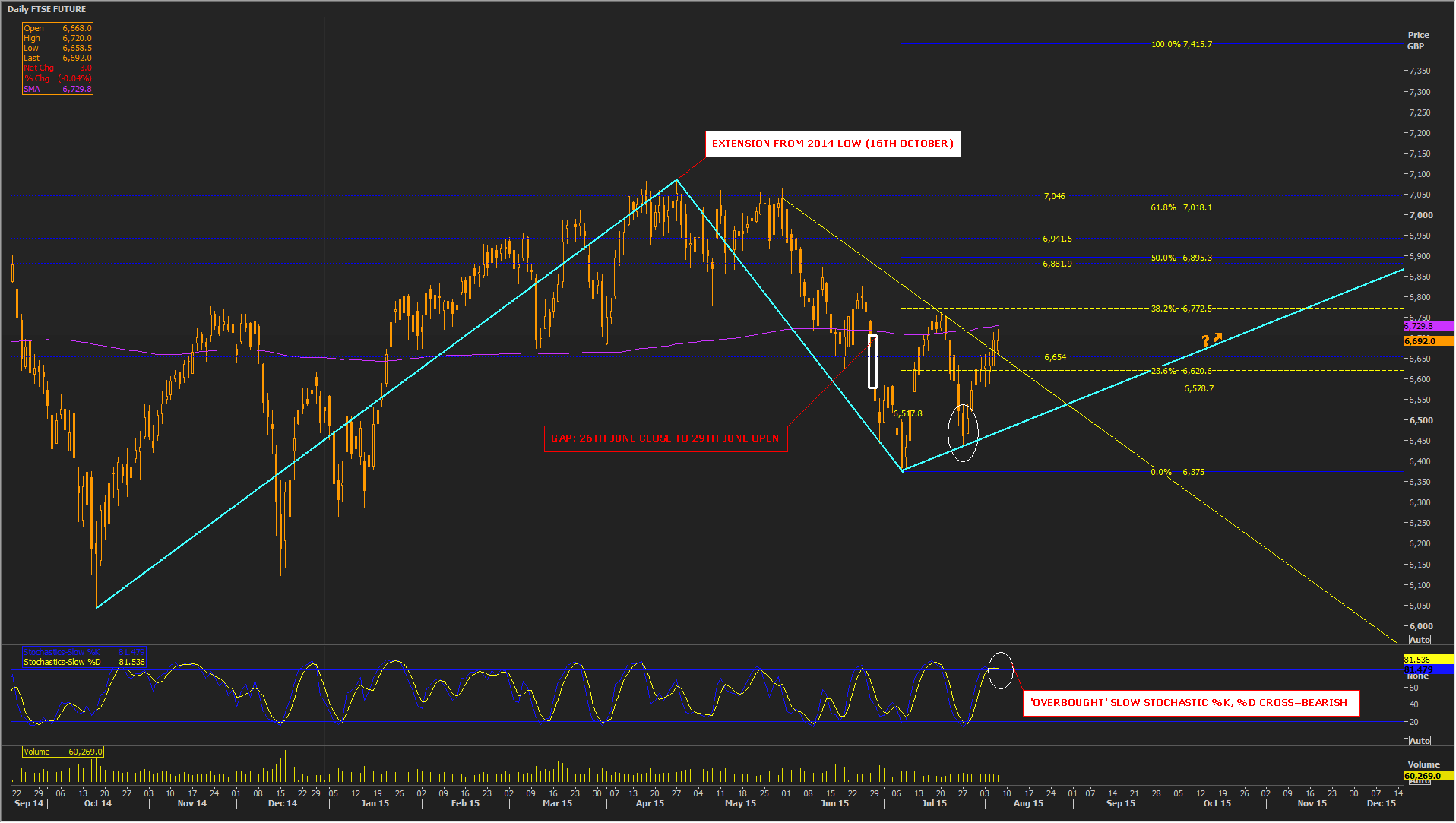

Looking at the main derivative of the benchmark that is tradable, InterContinental Exchange’s FTSE Future contract, it has now advanced for eight straight sessions after establishing a moderate uptrend by a lower low at the end of July than at the beginning of the month.

A synthetic ‘continuation’ version of the main contracts in this series puts the FTSE Future through a mild 23% projection off the July low, which itself was the base of a continuation from the 2014 low hit in October.

FTSE Future is now just 30 points away from its crucial 200-day moving average at 6729, and 20 points away from the 38.2% Fibonacci (6772) projection from July’s low.

Whilst current momentum does not favour a sustained rise above these important thresholds in the immediate term, the trajectory of the FTSE Future’s advance is likelier than not to propel it past these barriers in the next few months.

Additionally, the FTSE Future has maintained its poise, so far, above a descending line from the end of May, and resistance-turned-support around 6654.

On a more bearish perspective, should the contract’s forthcoming consolidation of its recent gains stray below the levels mentioned and lower support at 6578-6520, the risk of a breach of its recently established rising trend will increase.

That in turn will provide evidence for the longer-term bear case embodied by the FTSE’s struggling mining giants.

The benchmark index itself (not pictured) also tested the 200-day moving average on Thursday.

Successful meeting and breaching of either the FTSE’s or the FTSE Future’s 200-day MA would, naturally, provide virtuous feedback for both.