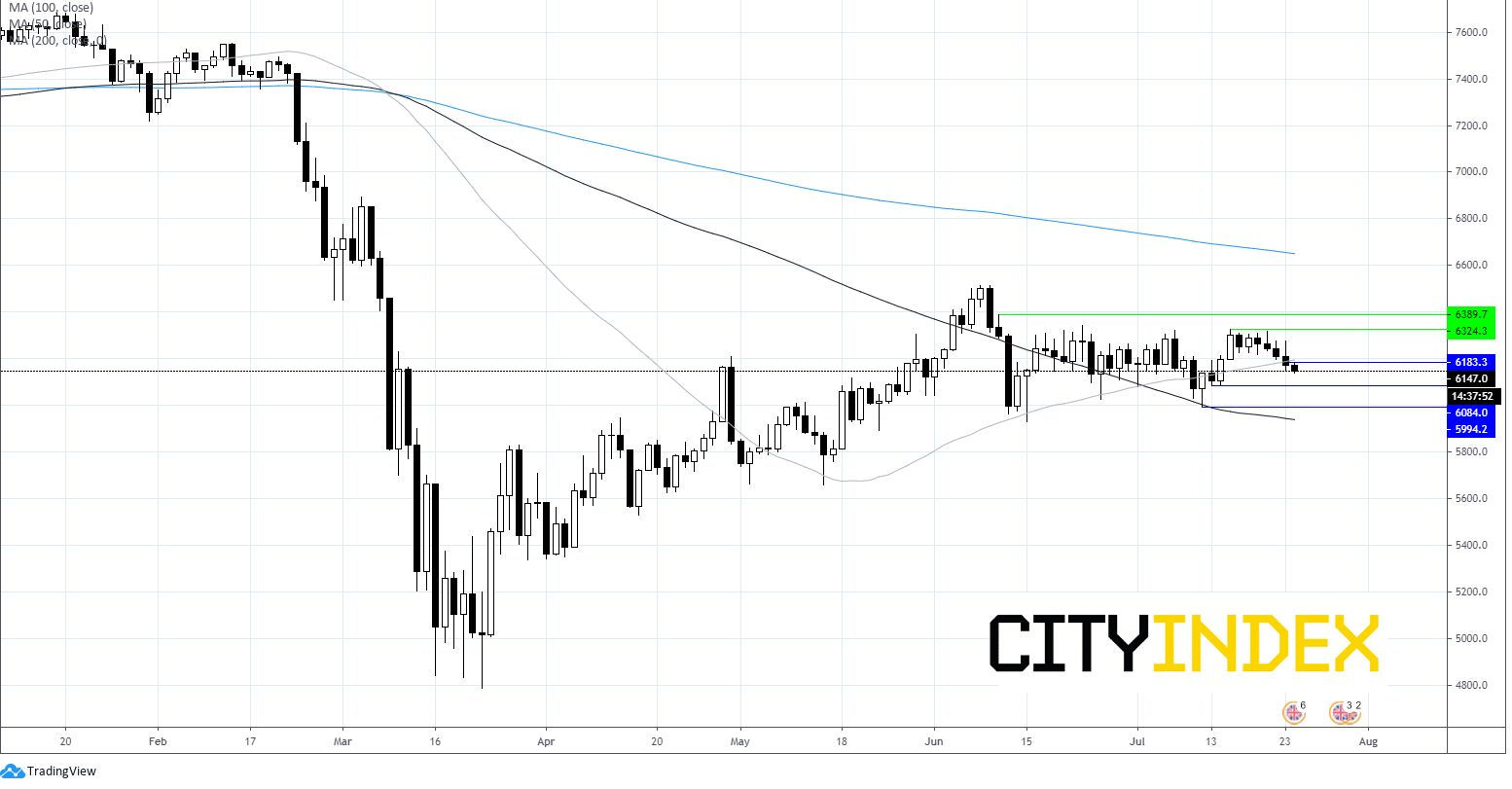

Concerns over the economic recovery in the US and raising US – Sino tensions are dragging on investor sentiment at the end of the week. European bourses are heading for a weaker start on the open despite UK retail sales soaring.

The week was on the whole upbeat following the EU recovery fund agreement; a stimulus package which sent a strong message as the EU reached an important milestone funding expenditure through capital market borrowing. The package will also go some way to cushioning the blow from the coronavirus crisis. Needless to say, the Euro has been the star performer this week, surging to a 21-month high versus the US Dollar.

US labour market recovery stalls

Concerns over the economic recovery in the US are weighing on risk sentiment. Data yesterday showed that the US labour market recovery was stalling as the US struggles to get control of the coronavirus outbreak. The number people signing up for unemployment benefits saw a weekly increase to 1.4 million, up from 1.3 million. The weekly increase comes as parts of California and the sunbelt re-impose lockdown measures in an attempt to slow the spread of the virus.

Concerns over the economic recovery in the US are weighing on risk sentiment. Data yesterday showed that the US labour market recovery was stalling as the US struggles to get control of the coronavirus outbreak. The number people signing up for unemployment benefits saw a weekly increase to 1.4 million, up from 1.3 million. The weekly increase comes as parts of California and the sunbelt re-impose lockdown measures in an attempt to slow the spread of the virus.

The data comes as Republicans and Democrats on Capitol Hill fail to reach and agreement on further stimulus ahead of the expiry of desperately needed unemployment benefits.

Adding to the risk adverse mood, China ordered the closure of the US consulate in Chengdu, in a tit for tat move following the shutting of the Chinese consulate in Houston. Fears are growing over the stability of the Phase 1 trade deal.

Adding to the risk adverse mood, China ordered the closure of the US consulate in Chengdu, in a tit for tat move following the shutting of the Chinese consulate in Houston. Fears are growing over the stability of the Phase 1 trade deal.

UK retail sales

UK retail sales surged in June, smashing expectations. Sales jumped 13.9% mom, adding to May’s 12% surge. This was well ahead of expectations for an 8% increase. The data shows that as lockdown measures eased and non-essential shops opened in the middle of the month, consumers were ready to spend. This is a very encouraging reading and boosts optimism surrounding a V-shaped recovery. However, as the government withdraws its support from the labour market, retail sales could quickly fall away. The Pound has lifted off session low and moved into positive territory at $1.2745.

UK retail sales surged in June, smashing expectations. Sales jumped 13.9% mom, adding to May’s 12% surge. This was well ahead of expectations for an 8% increase. The data shows that as lockdown measures eased and non-essential shops opened in the middle of the month, consumers were ready to spend. This is a very encouraging reading and boosts optimism surrounding a V-shaped recovery. However, as the government withdraws its support from the labour market, retail sales could quickly fall away. The Pound has lifted off session low and moved into positive territory at $1.2745.

PMI’s up next

Looking ahead PMI data will be in focus across the regions. The UK data is expected to be upbeat showing that activity in both the dominant service sector and the manufacturing sector expanded in July. If strong enough the numbers could boost optimism further surrounding a V-shaped recovery. Eurozone and US PMI data is expected to be similarly upbeat.

Latest market news

Yesterday 08:33 AM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM