Europe is pointing to a mixed open after a similar story on Wall Street where stocks stalled after reaching a fresh all-time high. Disappointing vaccine news combined with US stimulus optimism, Brexit nerves and strong German Factory orders are painting a mixed picture ahead of today’s non farm payroll report.

News that Pfizer has cut its rollout target for the covid vaccine by half, owing to supply chain obstacles has knocked risk sentiment. Vaccine optimism put the markets on a stellar run across November as investors priced in the end of the pandemic and a return to pre-pandemic growth, regardless of the dire few months expected before the vaccine becomes widely available. Then news from Pfizer means that it could now take longer to reach the end of the tunnel, but with other vaccines also coming, this is more of a set back rather than risk reset news.

However, optimism surrounding a large US economic stimulus package is helping lift US futures after the close. A $908 billion rescue package in the worlds largest economy now appears within reach, offering support to the global risk sentiment picture, off-setting some vaccine disappointment.

FTSE looks to outperform

The FTSE is seen opening on higher ground, outperforming its European peers whilst the Pound was holding 1.3450 as Brexit remained in focus. Headlines continue to be mixed, with the latest suggesting that today’s soft deadline will be passed. Even so, with the Pound at 12-month highs investors remain optimistic that a deal will be achieved.

The FTSE is seen opening on higher ground, outperforming its European peers whilst the Pound was holding 1.3450 as Brexit remained in focus. Headlines continue to be mixed, with the latest suggesting that today’s soft deadline will be passed. Even so, with the Pound at 12-month highs investors remain optimistic that a deal will be achieved.

Oil gains as OPEC agrees

Oil majors will be in focus as oil prices are rising after OPEC+ group agreed to a smaller than feared cut to output come January. The agreed cut of 500,000 barrels per day will put production cuts at 7.2 million bdp, down from the current 7.7 million. The group failed to agree on policy strategy beyond that. At the time of writing Brent trades up 2% at an 8 month high of $45.

Oil majors will be in focus as oil prices are rising after OPEC+ group agreed to a smaller than feared cut to output come January. The agreed cut of 500,000 barrels per day will put production cuts at 7.2 million bdp, down from the current 7.7 million. The group failed to agree on policy strategy beyond that. At the time of writing Brent trades up 2% at an 8 month high of $45.

US non-farm payrolls

Looking ahead US non-farm payroll will be in focus. Expectations are for a more modest gain in non farm payrolls in November following on from a sharp increase in jobs added in November.

500,000 new jobs are expected to have been created in November after 638,000 in the previous month. The unemployment rate is expected to edge down to 6.8% from 6.9%.

Leading indicators this month have been disappointing, with the ADP payroll coming in steeply lower and ISM manufacturing PMI Employment subcomponent also weakening, although the ISM services PMI employment component edged higher.

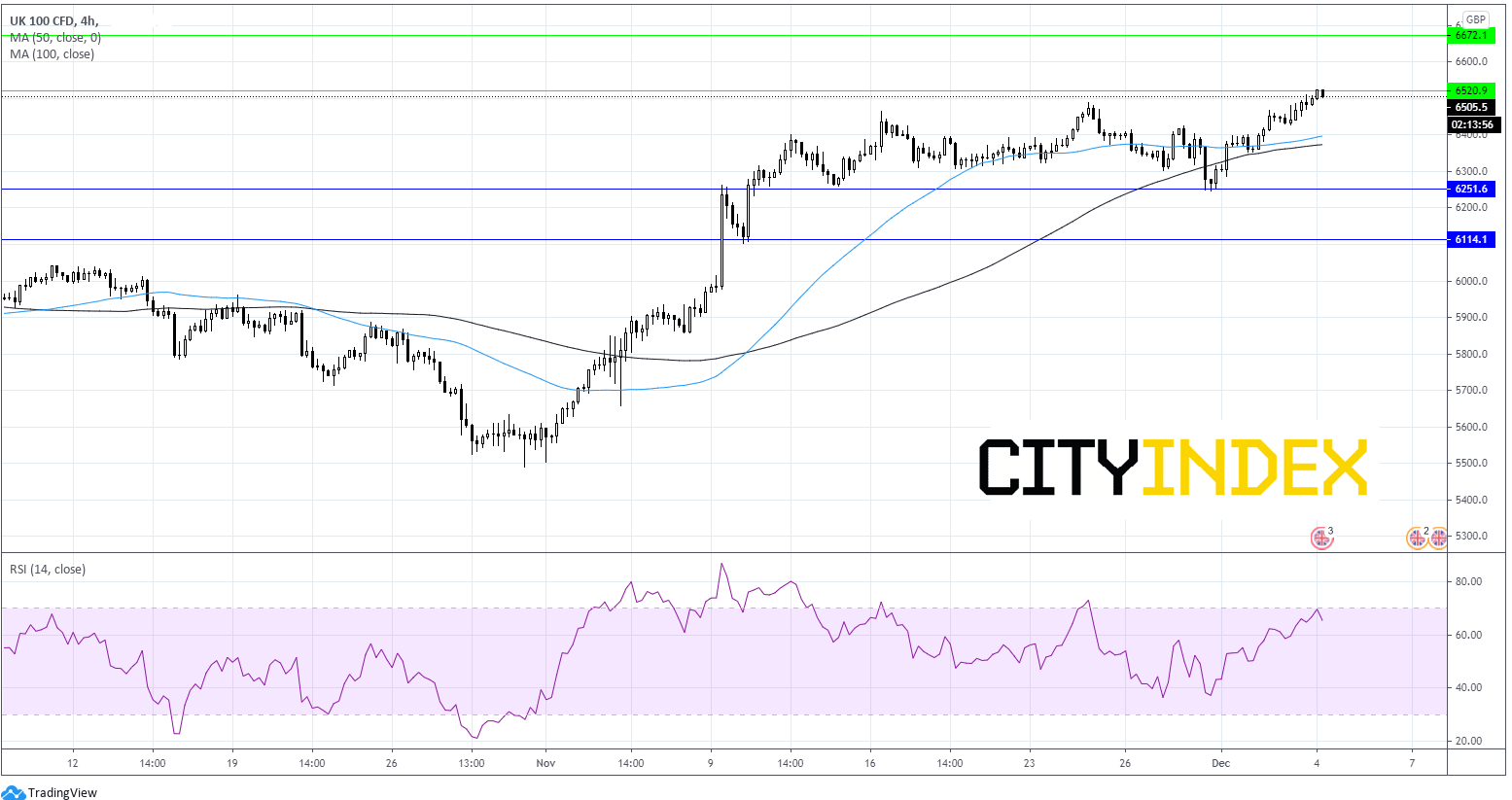

FTSE Chart

The FTSE is extending gains at a 9 month high of 6525, testing the upper band of the channel that it has traded in across November. A break through here could open the door to resistance at 6670. On the flip side, failure to break resistance could see the price head back towards 6400 50 & 100 sma on 4 hour chart.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM