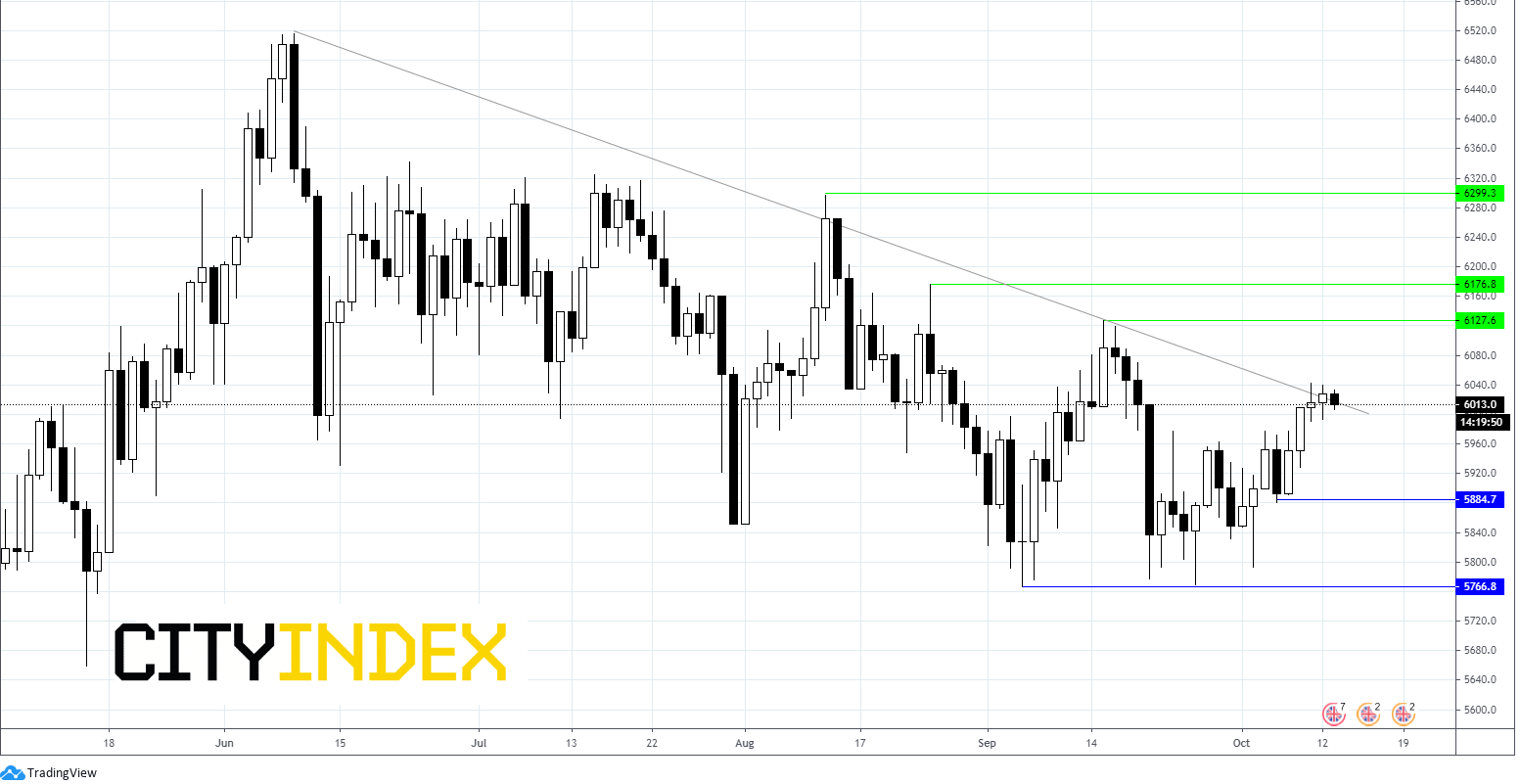

The FTSE is heading higher on the open following a solid performance on Wall Street. US indices surged ending close to all time highs as fears over a contested US Presidential election ease and large tech surged. Upbeat Chinese trade data and mixed UK jobs numbers are playing into the mix.

China remains on road to recovery

Upbeat Chinese trade data in the Asian session is helping investors look past the lack of US Congressional agreement over fiscal stimulus. Chinese exports surged 9.9% rising for a fourth straight month in September, whilst imports jumped 13.2% as economies across the globe reopened. Analysts had expected exports to rise 10% and imports to edge just 0.4% higher. China remains clearly on the rad to recover, as it capitalises on economies reopening across the globe.

UK jobs data provides little clarity

UK jobs data threw out mixed signals. Unemployment ticked higher to 4.5% in the three months to August whilst July’s reading was upwardly revised to 4.3%. However, the timelier claimant count increased by a significantly less than forecast 28K vs 78.8K expected. The claimant count is very surprising. We would have expected this to start to show those coming off the furlough scheme as company contribution increases. The broad expectation is still that the UK will see a sharp increase in the number of people unemployed by the end of the year, particularly as the chancellors Job Support Scheme is significantly less generous than the Jobs retention scheme and given that large parts of the UK are likely to see tighter lockdown restrictions in the coming weeks.

Johnson & Johnson halts vaccine trial

News that Johnson & Johnson have paused its covid trial due to an unexplained illness in a participant is keeping risk sentiment in check. An independent safety monitoring board will review and evaluate the data. These pauses are considered normal in large scale vaccine trials. It would have to be a serious event to halt trials, hopes are that this will blow over quickly as it did with AstraZeneca. Johnson & Johnson, which is due to report later today, has been a front runner in the development of a vaccine candidate to fight covid. Given that a vaccine is the surest way to return to pre-covid levels of growth, the markets are particularly sensitive to vaccine developments and news.

A win for Biden is a win for stimulus?

With Joe Biden now 10 points ahead in the polls uncertainty surrounding the election has waned and expected volatility in the equity markets for November and December has fallen significantly. Markets hate uncertainty, anything that can remove a layer of uncertainty is considered risk positive.

The risk on trade continues into Europe, although with less umph, riskier stocks are in demand. Investors are optimistic that a large US fiscal stimulus package is on its way after the election. A win by Joe Biden is expected to be particularly lucrative, Democrats have shown that they support a large scale covid relief package. Markets have made their peace with the idea that stimulus might not be before the elections, but it will be worth waiting for.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest FTSE 100 articles

March 11, 2024 04:30 PM

March 5, 2024 12:00 PM

February 12, 2024 10:30 AM

January 15, 2024 12:30 PM