FTSE drops as oil breaks 30 but will there be more drama later

There was finally some hope of a rebound for the slumping equities as the global stock indices surged higher from deeply oversold levels yesterday. The […]

There was finally some hope of a rebound for the slumping equities as the global stock indices surged higher from deeply oversold levels yesterday. The […]

There was finally some hope of a rebound for the slumping equities as the global stock indices surged higher from deeply oversold levels yesterday. The markets rallied as oil bounced again off the psychologically-important $30 handle. But those hopes were dashed in overnight trading as Chinese shares led a decline in global markets that has so far lasted in the first half of today’s session. So it may be a different day, but it is still the same story: down goes oil, down goes (almost) everything.

US index futures point to a sharp drop at the open, but will Wall Street traders once again rescue the day? In part, this will depend on the possibility for a rebound in oil prices and also earnings. Among the major US companies reporting their results today are BlackRock, Citigroup, US Bancorp and Wells Fargo. Undoubtedly, earnings from Citi will be the key one to watch.

In Europe, the UK’s FTSE 100 is among the top losers. Understandably, it is the resources sector that is leading the falls, with miner Anglo American being down more than 10%. Another top faller today is BHP Billiton, with its shares being almost 7% lower at the time of this writing after it said it would write down the value its US shale assets by $7.2 billion.

Crude’s drop below $30 is yet another blow for the commodity currencies and energy stocks, and it just goes to show what speculators are feeling at the moment about the prospects of fresh supplies hitting an already-saturated market from Iran. Those who had hoped to see a more significant rebound from $30 will have been disappointed and so the withdrawal of bids from this group of speculators is further clearing the path of least resistance which at the moment is clearly to the downside. Indeed, if crude holds below the $30 level on a closing basis then there is not much further significant support until $25 now. That being said however, the day has just started and we may see some short-covering later on ahead of the week and possibly around the time Baker Hughes releases the weekly rig counts data later this afternoon. If for whatever reason oil closes the day decisively back above $30, then that would be a bullish technical scenario. And not just for oil.

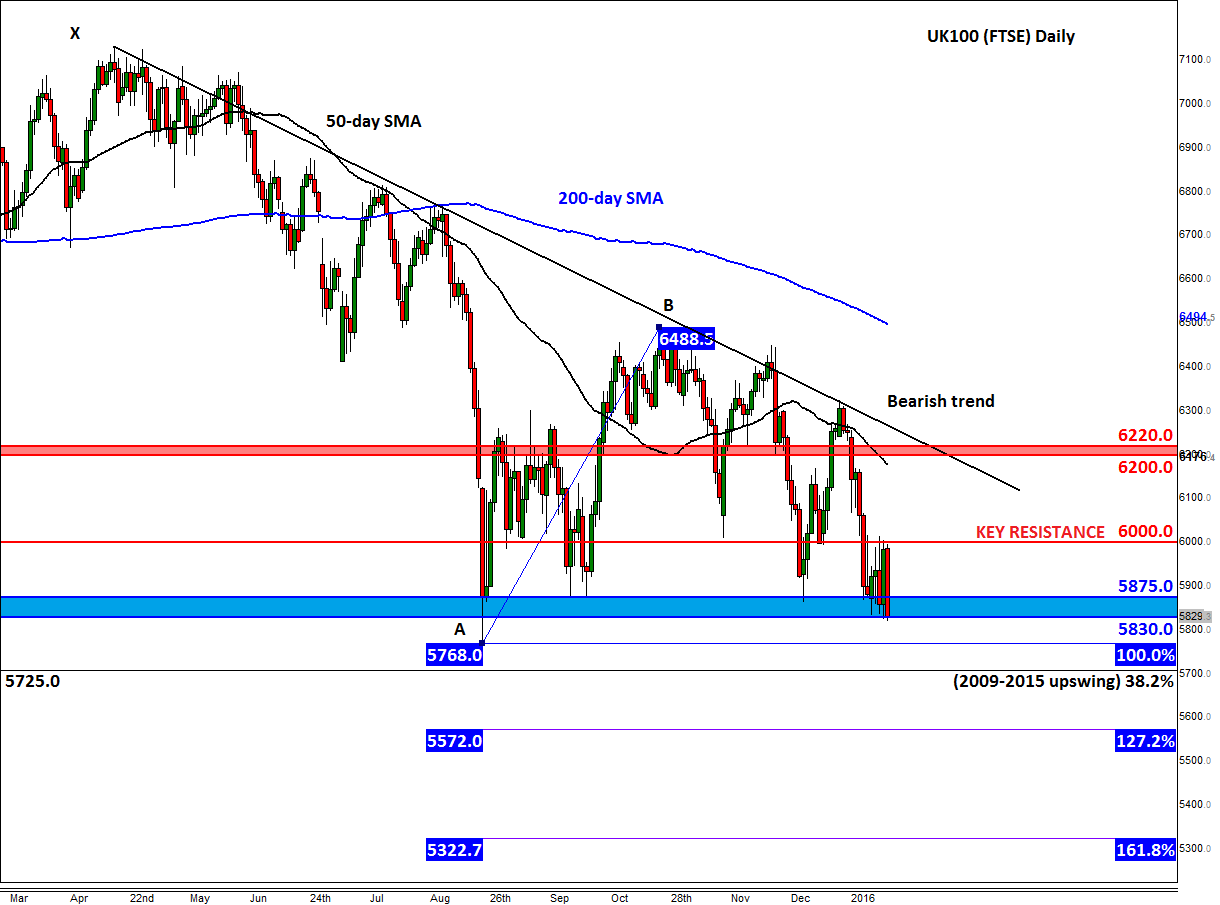

The FTSE is testing a key technical area of its own around 5830-5875 (ahead shaded in blue on the chart). Here, it has found repeated support in the past, but the lack of any significant bounce this time suggests a break down might be forthcoming. The next bearish targets are at 5765/70, the August 2015 low, followed by the Fibonacci extension levels at 5570/5 (127.2%) and 5320/5 (161.8%). The 38.2% Fibonacci retracement level of the entire 2009-2015 upswing comes in at 5725. This could an important level to watch, should we get there.

Meanwhile, as yesterday’s rally again failed at the important 6000 level, speculators should watch this level closely for a break above it would be a bullish outcome. If seen, the FTSE may then rally all the way back to the bearish trend line and the next key resistance area between 6200 and 6220.